Market Summary

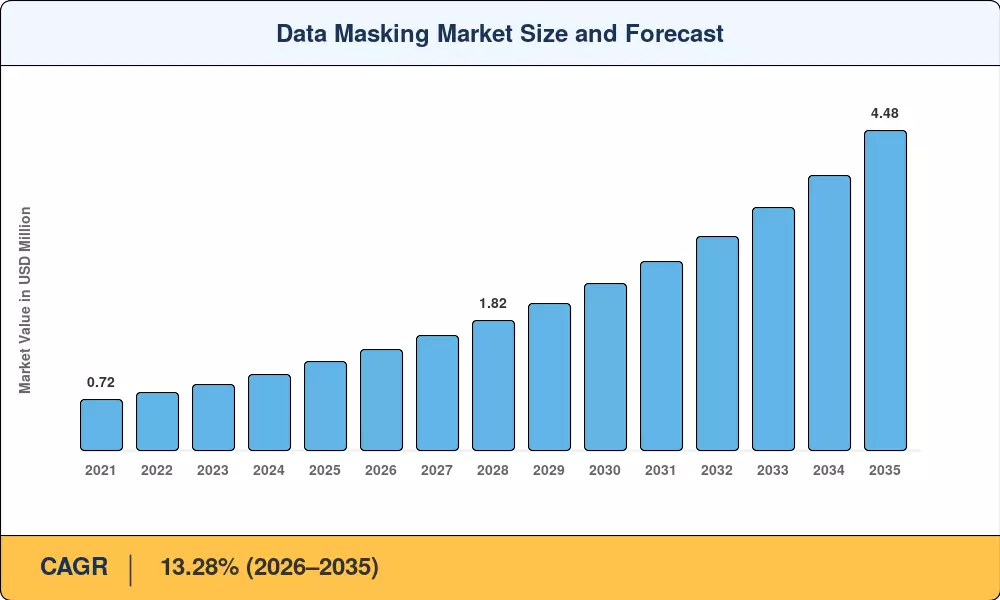

The Data Masking Market reached a valuation of USD 1.24 billion in 2025 and is projected to grow from USD 1.42 billion in 2026 to USD 4.48 billion by 2035, registering a CAGR of 13.28% during the forecast period (2026–2035). Tightening data privacy mandates — including the EU's Digital Operational Resilience Act (DORA) and California's updated CCPA enforcement provisions — are compelling enterprises to formalize sensitive data obfuscation techniques across production and non-production environments [2]. Simultaneously, a 72% year-over-year surge in ransomware targeting database assets through 2024 has accelerated procurement of tokenization for PII data protection and static and dynamic data masking for test environments [3].

A pronounced technology shift is underway as organizations retire legacy, script-based anonymization routines in favor of AI-augmented masking platforms capable of automated sensitive-field discovery and format-preserving transformations. Gartner estimates that enterprise spending on data anonymization for GDPR compliance tooling surpassed USD 2.1 billion globally in 2024, reflecting a decisive pivot toward integrated masking suites that serve DevOps pipelines and analytics workloads simultaneously. Database masking for non-production environments is now a baseline expectation for CI/CD workflows, replacing ad-hoc data subsetting practices that introduced compliance risk.

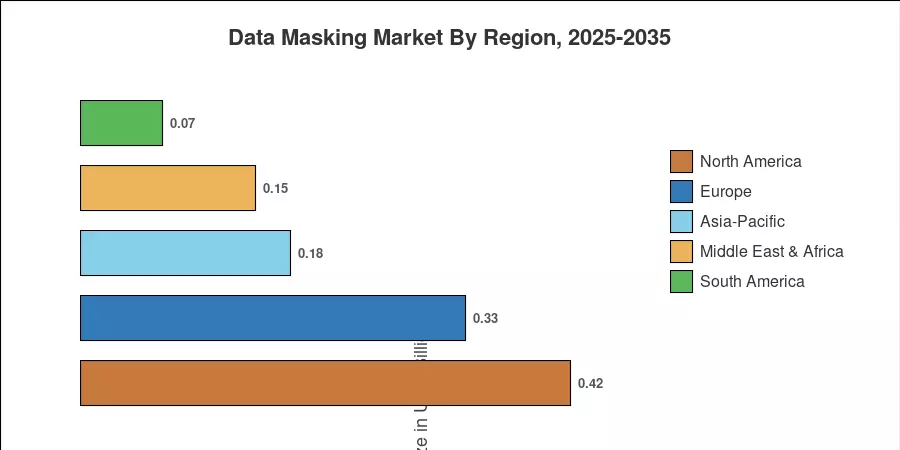

North America held approximately 34% of the Data Masking Market share in 2025, anchored by stringent HIPAA and SOX enforcement and a mature cloud-services ecosystem. Asia-Pacific is the fastest-growing region at a projected CAGR of 14.22% through 2035, propelled by India's Digital Personal Data Protection Act (2023) and China's expanding cross-border data transfer regulations [5]. Europe represents the second-largest regional bloc, where GDPR penalty escalations continue to drive adoption of data anonymization for GDPR compliance solutions across financial services and healthcare verticals. The Data Masking Market is poised for sustained double-digit expansion as hybrid-cloud architectures and real-time analytics push masking deeper into enterprise data stacks.

Key Report Takeaways

• By Type

- Static masking captured 53.21% revenue share of the Data Masking Market in 2025, reflecting its dominance in batch-oriented database masking for non-production environments

- Dynamic masking is set to expand at a 13.68% CAGR through 2035, driven by demand for real-time tokenization for PII data protection in customer-facing applications

• By Deployment Model

- On-premise installations represented 50.87% of the Data Masking Market in 2025, favored by regulated industries requiring data residency control

- Cloud deployments are growing at a 13.91% CAGR through 2035 as SaaS-native masking platforms gain traction

• By Organization Size

- Large enterprises commanded 63.48% of market revenue in 2025, investing heavily in sensitive data obfuscation techniques across distributed data estates

- SMEs register the fastest growth outlook at a 13.82% CAGR through 2035

• By End-User Industry

- BFSI captured USD 0.33 billion in 2025, reflecting rigorous compliance mandates for static and dynamic data masking for test environments

- Healthcare is advancing at a 14.08% CAGR to 2035, fueled by electronic health record (EHR) masking requirements

• By Region

- North America led the Data Masking Market with approximately 34% share in 2025

- Asia-Pacific is set to rise at a 14.22% CAGR through 2035, led by regulatory modernization across India, China, and ASEAN nations

MRFR's market sizing integrates bottom-up vendor revenue analysis, end-user procurement surveys across 22 countries, and top-down macroeconomic modeling benchmarked against IT security spending indices. Historical figures (2021–2024) are calibrated to reported enterprise data protection budgets, while the forecast (2026–2035) applies a compound model adjusted for regulatory cadence, cloud migration velocity, and technology substitution curves[6].