Isocyanate Market Summary

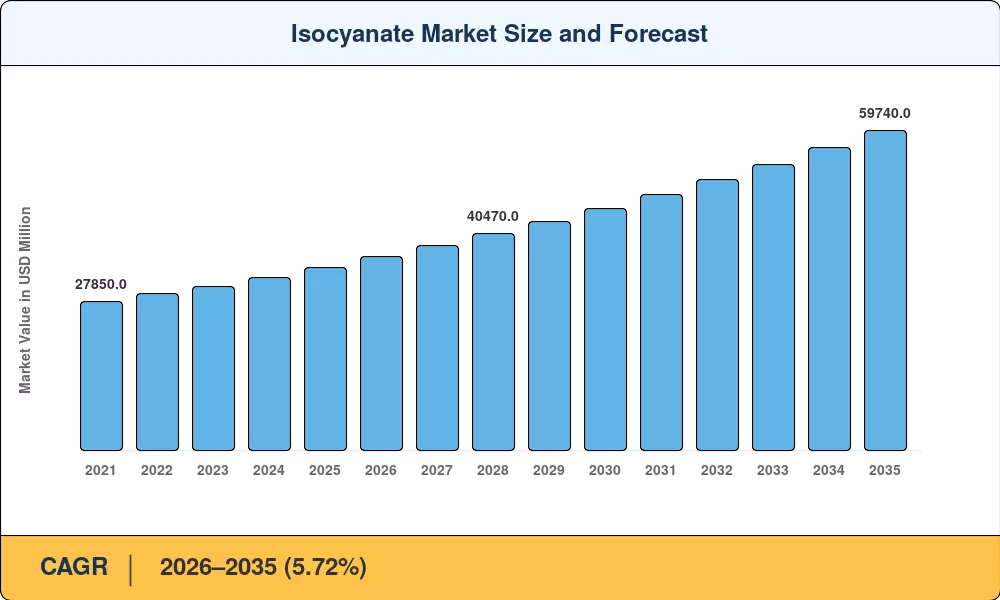

The global Isocyanates Market reached an estimated USD 34,250 million in 2025 and is projected to climb from USD 36,210 million in 2026 to USD 59,740 million by 2035, registering a compound annual growth rate of 5.72% during the forecast period. Two structural catalysts underpin this trajectory: tightening building-energy codes across the EU, China, and the United States that mandate higher-performing insulation, and the global automotive sector's accelerating shift toward lightweight electric-vehicle architectures that rely heavily on polyurethane-based structural components and interior foams [1][2].

The supply side of the isocyanates market is changing due to a subtle but significant technological shift. Gas-phase phosgenation process innovations that drastically reduce solvent consumption and energy footprints are methodically replacing legacy liquid-phase phosgenation assets. This dedication to sustainable manufacturing is demonstrated by Covestro's major infrastructure improvements at its flagship TDI facility in Dormagen, which are matched on the backbone side by Wanhua Chemical's fully integrated benzene-to-MDI operations in Yantai, which provide unmatched feedstock security. Aliphatic options like HDI and IPDI, which are now crucial parts of high-exposure automotive coatings and industrial finishes needing exceptional UV protection, are in great demand due to specialized applications.

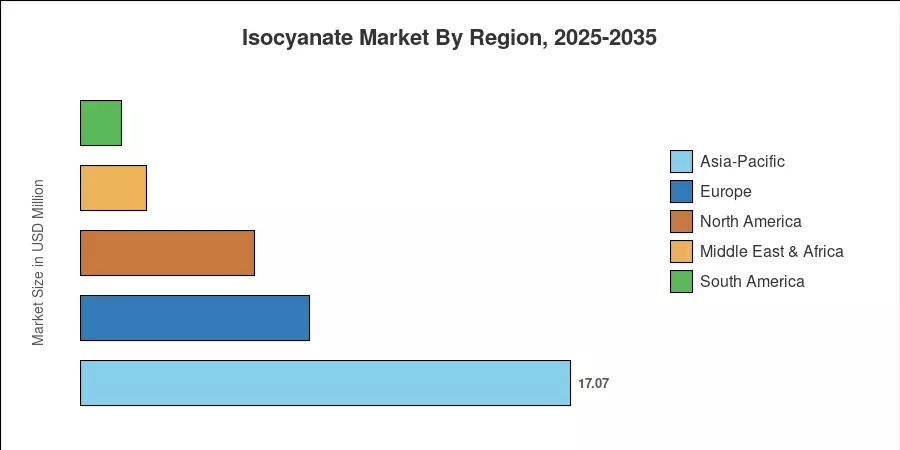

With China's enormous appliance and construction industries at its core, the Asia-Pacific accounts for about 50.2% of world volume. As downstream polyurethane processing capacity grows in Saudi Arabia and the United Arab Emirates, the Middle East and Africa area is expected to record a 6.78% CAGR through 2035, making it the fastest-growing geography in the isocyanates market. Due to strict thermal performance requirements and renovation wave mandates, Europe has the second-largest share at roughly 23.5%. Over the next ten years, there will be a major reconfiguration of the competitive landscape due to new capacity increases throughout Southeast Asia and the Gulf Cooperation Council.

Key Report Takeaways

• By Type

- MDI accounted for 63.2% of the Isocyanates Market in 2025, reflecting its dominant role in rigid insulation and appliance foam.

- Aliphatic isocyanates are forecast to register the fastest type-level CAGR of 7.25% through 2035, driven by automotive and industrial coating reformulations.

• By Application

- Rigid foam represented 34.8% of the total Isocyanates Market volume in 2025, led by construction-sector insulation demand.

- Paints and coatings applications are projected to grow at a 6.98% CAGR through 2035, supported by UV-stable aliphatic formulations.

• By End-User Industry

- Building and construction held a 43.8% share of the Isocyanates Market in 2025.

- The automotive end-user segment is expected to expand at a 7.12% CAGR through 2035 as EV lightweighting programs scale globally.

• By Region

- Asia-Pacific dominated the Isocyanates Market with a 50.2% share in 2025.

- The Middle East & Africa region is forecast to post the highest regional CAGR of 6.78% from 2026 to 2035.

Isocyanates Market Size and Forecast (2021–2035)

Market sizing draws on a combination of trade-flow data from UN Comtrade, producer capacity utilization reports, and downstream polyurethane consumption models cross-validated against national chemical-industry statistics. Historical figures (2021–2024) use confirmed shipment volumes; the 2025 base year blends preliminary trade data with proprietary demand indices. Forecast values (2026–2035) apply a calibrated CAGR of 5.72%, adjusted for planned capacity additions and anticipated regulatory impacts [5].