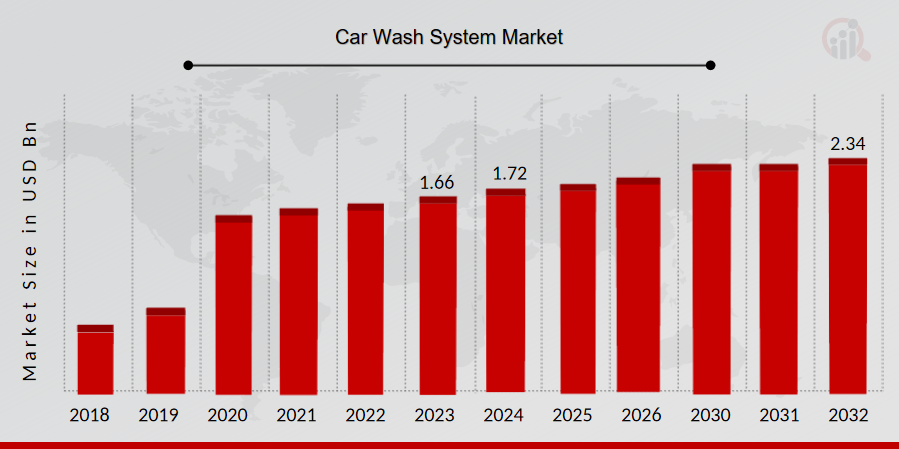

What is the current valuation of the Car Wash System Market?

As of 2024, the Car Wash System Market was valued at 1.73 USD Billion.

What is the projected market valuation for the Car Wash System Market in 2035?

The market is projected to reach a valuation of 2.627 USD Billion by 2035.

What is the expected CAGR for the Car Wash System Market during the forecast period 2025 - 2035?

The expected CAGR for the Car Wash System Market during 2025 - 2035 is 3.87%.

Which segments are included in the Car Wash System Market?

The market segments include Tunnels, Roll-Over/In-Bay, and Self-Service car wash systems.

What were the valuations for the Tunnels segment in 2024?

In 2024, the Tunnels segment was valued at 0.69 USD Billion.

How does the Roll-Over/In-Bay segment perform in terms of valuation?

The Roll-Over/In-Bay segment had a valuation of 0.52 USD Billion in 2024.

What is the valuation of the Self-Service segment as of 2024?

The Self-Service segment was valued at 0.52 USD Billion in 2024.

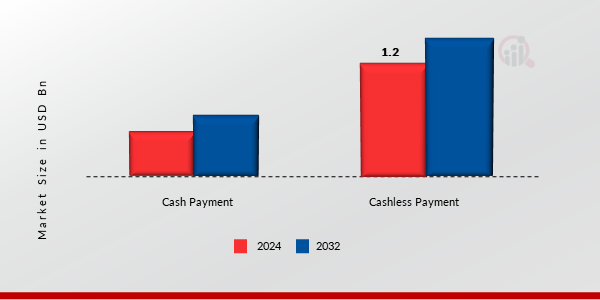

What modes of payment are prevalent in the Car Wash System Market?

The prevalent modes of payment include Cash Payment and Cashless Payment.

What were the valuations for Cashless Payment in 2024?

In 2024, Cashless Payment was valued at 1.23 USD Billion.

Who are the key players in the Car Wash System Market?

Key players include WashTec AG, Istobal S.A., DRB Systems LLC, and others.