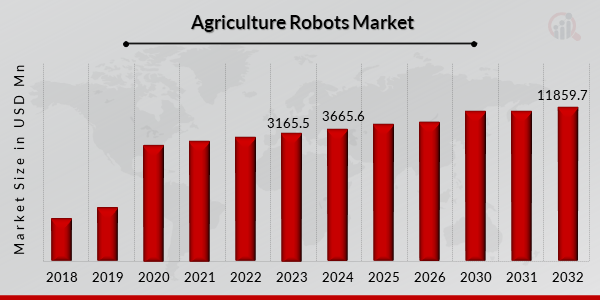

What is the current valuation of the Agriculture Robots Market as of 2024?

The Agriculture Robots Market was valued at approximately 3665.6 USD Million in 2024.

What is the projected market size for the Agriculture Robots Market in 2035?

The market is expected to reach a valuation of around 18426.18 USD Million by 2035.

What is the expected CAGR for the Agriculture Robots Market during the forecast period 2025 - 2035?

The Agriculture Robots Market is anticipated to grow at a CAGR of 15.81% from 2025 to 2035.

Which application segment had the highest valuation in 2024?

In 2024, the Harvesting application segment led with a valuation of 920.0 USD Million.

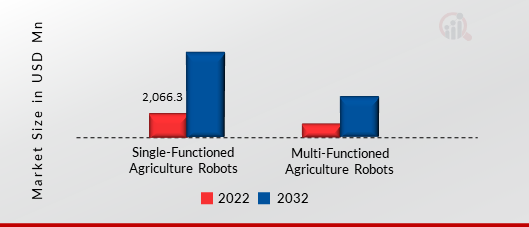

What are the key types of agriculture robots currently dominating the market?

The market is currently dominated by types such as Robotic Harvesters, which had a valuation of 900.0 USD Million in 2024.

How do the valuations of autonomous tractors compare to drones in 2024?

In 2024, autonomous tractors were valued at 800.0 USD Million, while drones had a valuation of 600.0 USD Million.

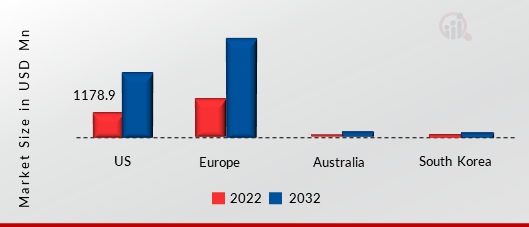

What end-use segment accounted for the largest share in the Agriculture Robots Market in 2024?

Farms represented the largest end-use segment, with a valuation of 1099.68 USD Million in 2024.

Which company is recognized as a key player in the Agriculture Robots Market?

John Deere is recognized as a key player in the Agriculture Robots Market, contributing significantly to its growth.

What is the valuation of the weed control application segment in 2024?

The weed control application segment was valued at 845.6 USD Million in 2024.

How does the market for planting robots compare to that of weeding robots in 2024?

In 2024, planting robots were valued at 765.6 USD Million, while weeding robots had a valuation of 600.0 USD Million.