Silicone Elastomers Size

Market Size Snapshot

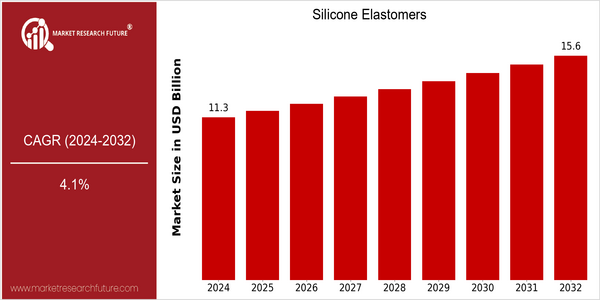

| Year | Value |

|---|---|

| 2024 | USD 11.29 Billion |

| 2032 | USD 15.57 Billion |

| CAGR (2024-2032) | 4.1 % |

Note – Market size depicts the revenue generated over the financial year

The market for silastic elastomers is growing steadily, with the current market size of $ 11.29 billion in 2024, projected to reach $ 15.57 billion by 2032. The CAGR for this period is 4.1%. The growth of the market is mainly driven by the increasing demand for silastic elastomers in various industries, such as the automobile, medical and electrical industries. In recent years, as industries have tended to focus on obtaining materials with excellent properties such as heat resistance, elasticity and wear resistance, silastic elastomers have become more and more popular in seals, gaskets, medical devices and other fields. , and the market is expected to grow. Technological innovation and formulation development will also promote market growth. Companies are investing in R & D to improve the properties of silastic elastomers and make them more flexible and more suitable for various applications. Strategic initiatives such as establishing strategic alliances and launching new products have been launched by leading companies such as Dow, Wacker Chemie AG and Momentive Performance Materials to enhance their market position. For example, the recent establishment of a joint venture to develop sustainable silicone materials reflects the industry's innovation and commitment to the environment.

Regional Market Size

Regional Deep Dive

The Silicone Elastomer Market is characterized by its wide range of applications in several industries including automotive, healthcare, and consumer goods. In North America, the market is driven by technological advancements and a strong manufacturing base, while Europe is driven by concerns related to sustainable development and regulatory compliance. In the Asia-Pacific region, the growing industrialization and urbanization have led to an increased demand for these products. The Middle East and Africa are gradually adopting these products owing to the development of their infrastructural base, while Latin America is focusing on enhancing its manufacturing base to meet the growing demand for these products. Each region offers unique opportunities for market growth, based on its economic conditions, regulatory frameworks, and cultural factors.

Europe

- A growing trend in Europe is towards the use of bio-based silicone elastomers, a trend that is driven by the Green Deal and the sustainable development initiatives of the European Union. Momentive and Elkem are leading the way in the development of eco-friendly silicone products that meet the increasing demand for sustainable materials.

- In the European market, the stricter safety regulations, such as REACH, also affect the manufacturers. This has resulted in an increase in the number of innovation and product development costs to meet the regulatory requirements.

Asia Pacific

- The Asia-Pacific region is experiencing a rapid growth in the silicon elastomer market, especially in China and India, where the process of industrialization and urbanization is accelerating. To meet this growing demand, the major manufacturers, such as Shin-Etsu and KCC, are expanding their production capacity.

- High-tech products and manufacturing processes, such as the development of high-performance silicone elastomers for medical applications, are gaining ground. The increasing use of advanced materials in the health care industry will further spur the growth of the market.

Latin America

- Latin America is concentrating on increasing its manufacturing capacity to meet the growing local demand for elastomers, especially in the automobile and consumer goods industries. Siltech and Dow have set up local production facilities to supply this market.

- The use of silicone rubber in the medical field is also a sign of the growing importance of medical devices and the growing importance of medical care. This is expected to drive growth in the coming years.

North America

- The North American market is experiencing a strong growth in the demand for silicone elastomers in the automobile industry, due to the growing trend towards electric vehicles and the need for light materials that can increase energy efficiency. As a result, companies like Dow and Wacker are investing heavily in research and development in order to develop new silicone solutions tailored to the requirements of the electric vehicle market.

- The Californian regulations enacted in the course of the last few years, directed toward the reduction of exhausts and the encouragement of sustainable materials, are putting the manufacturers of the rubber industry under pressure to adopt silicone rubbers that meet the strictest standards of the new regulations. This will undoubtedly stimulate the growth of the market as the companies align their products with these regulations.

Middle East And Africa

- In the Middle East and Africa, the market for silicone rubbers is influenced by the considerable investments in the construction and transport industries. The companies BASF and Huntsman are active in the region and are thus contributing to the growth of the market.

- The region's particular climate also influences the demand for elastomers, especially in applications requiring high thermal stability and resistance to harsh environments. In the future, it is expected that innovation and development of products to meet local needs will be encouraged.

Did You Know?

“Silicone elastomers are known for their exceptional thermal stability, withstanding temperatures ranging from -60°C to 200°C, making them ideal for a wide range of applications.” — Silicone Elastomers Market Research Report, 2023

Segmental Market Size

The market for elastomers is a key component of the silicone market, which is currently growing steadily, driven by the rising demand from various industries. The demand for high-quality materials in the automotive and medical industries, as well as the stricter requirements for the use of non-toxic and environmentally friendly materials, are the main drivers of the elastomers market. Furthermore, the development of production technology increases the material properties of elastomers, thus making them more attractive for producers. At present, the use of elastomers is already in a mature stage, with Dow and Wacker being the market leaders in terms of innovation and application. Elastomers are used in medical devices, car seals, and in the electronics industry in applications where flexibility and resilience are important. Moreover, macro-economic trends, such as sustainable development and the trend towards the use of lightweight materials in cars, are also promoting the growth of the elastomers market. In addition, 3D printing and injection molding technology are also influencing the development of elastomers, which allows for the more efficient and flexible production of products.

Future Outlook

From 2024 to 2032, the silicone elastomer market is expected to grow from $11.29 billion to $15.57 billion, with a compound annual growth rate (CAGR) of 4.1%. This growth is mainly driven by the increasing use of silicon elastomers in many industries, such as the automobile, health, electrical appliances, and building materials. The demand for silicon elastomers is expected to rise sharply. By 2032, the penetration rate of silicon elastomers in the automobile and medical fields will reach about 30 and 25 percent respectively. Also, some key technological developments, such as the development of high-temperature resistant silicon elastomers and medical silicon elastomers with high biocompatibility, will drive market growth. In addition, as the government tightens its regulations on the environment, the demand for silicon elastomers, which are known to be durable and recyclability, will also increase. Also, with the development of smart manufacturing and the increasing demand for sustainable development, the trend of the market is expected to change. As a result, the silicon elastomer industry is facing a strong innovation and competition environment, and needs to position itself to meet the needs of end users.

Leave a Comment