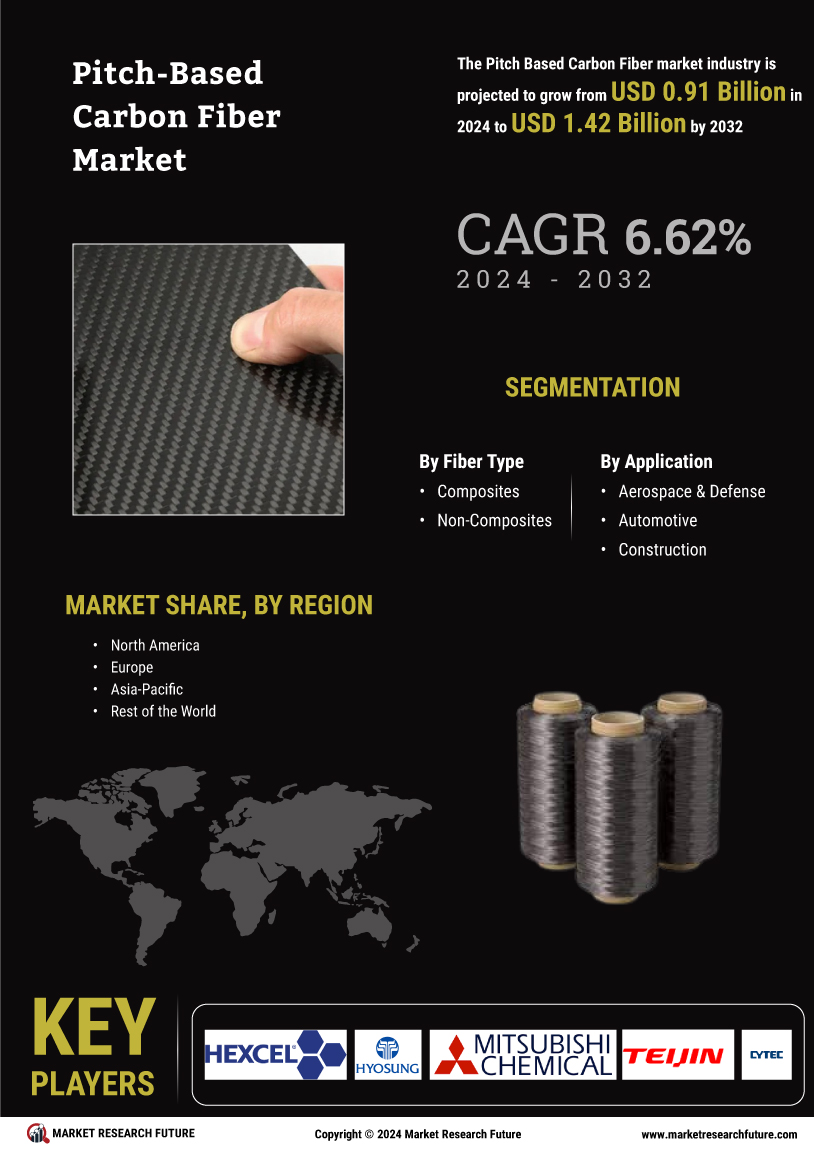

Pitch Based Carbon Fiber Market Segmentation

Pitch Based Carbon Fiber Market By Type (USD Billion, 2025-2035)

- Composites

- Non-Composites

Pitch Based Carbon Fiber Market By Application (USD Billion, 2025-2035)

- Aerospace & Defense

- Automotive

- Construction

- Wind Energy

- Sports & Leisure

- Others