Patient Lifting Equipment Market Summary

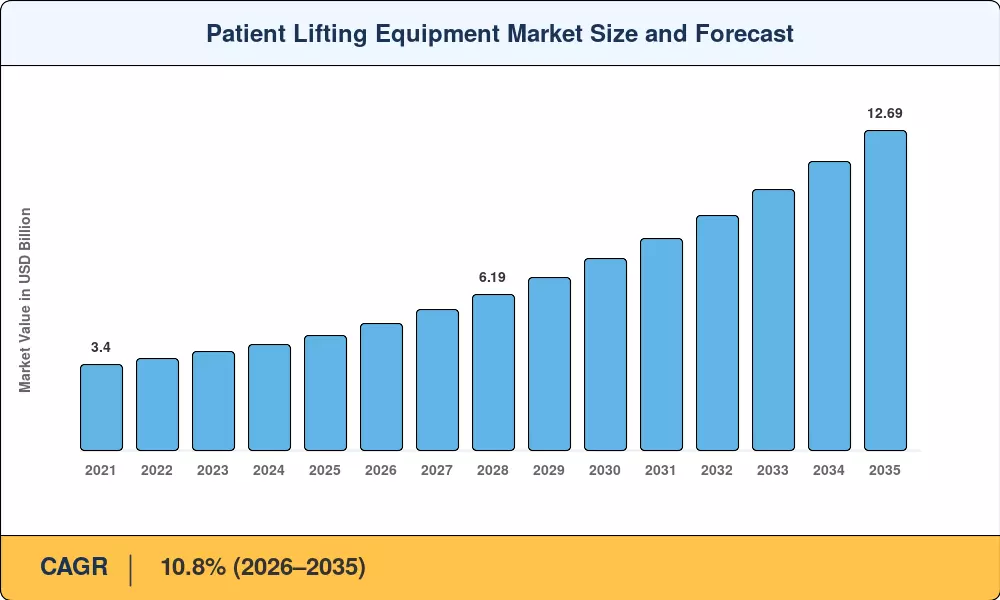

The Global Patient Lifting Equipment Market size was valued at USD 4.58 Billion in 2025, and the market is projected to grow from USD 5.04 Billion in 2026 to USD 12.69 Billion by 2035, registering a CAGR of 10.8% during the forecast period 2026–2035. This acceleration traces directly to government-enforced zero-lift and safe patient handling mandates — the U.S. Occupational Safety and Health Administration (OSHA) alone recorded over 46,000 back injuries among healthcare workers annually, fueling regulatory urgency [1]. Capital allocation into powered transfer systems intensified as acute care providers scaled infection-control-compliant equipment budgets beyond USD 1.2 Billion globally during 2024 [2].

Technology adoption is reshaping the patient lifting equipment market from the facility floor up. Manual hoists and gait belts, once standard across hospital wards and long-term care wings, are giving way to ceiling-mounted rail systems, IoT-enabled smart lifts with integrated load sensors, and battery-powered mobile platforms. The European Union's revised Medical Device Regulation (MDR 2017/745) has accelerated device requalification timelines, pushing manufacturers to embed digital health records interoperability into new lift platforms [3].

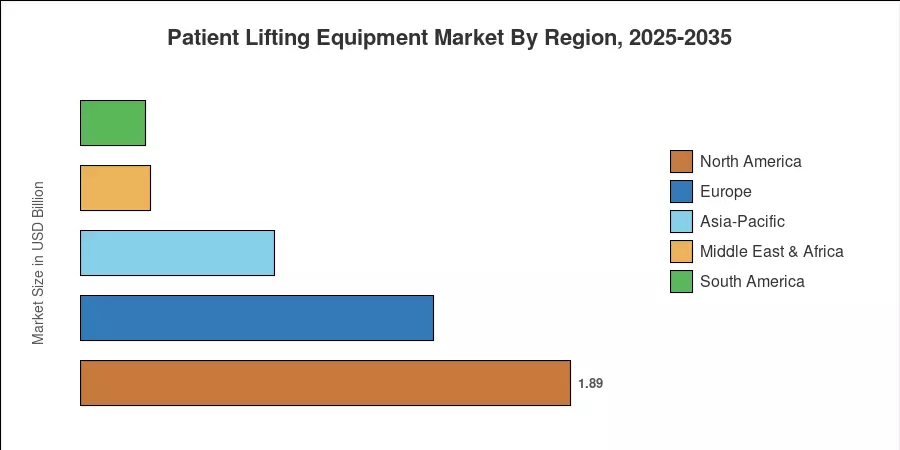

North America commanded a 41.3% share of the patient lifting equipment market in 2025, anchored by reimbursement-favorable Medicare policies and a dense network of rehabilitation facilities. Asia-Pacific registered the fastest regional CAGR at 16.4%, driven by hospital capacity expansions across India, China, and ASEAN nations [4]. Europe held the second-largest share at 29.8%, underpinned by aging demographics and robust occupational safety legislation. The convergence of bariatric care demand, home-care decentralization, and rental-model proliferation positions this market for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Product

- Ceiling lifts captured 35.1% revenue share of the patient lifting equipment market in 2025, reflecting high adoption in new hospital builds and renovation projects.

- Stair and wheelchair platform lifts are projected to advance at a 15.6% CAGR through 2035, driven by residential accessibility retrofitting and aging-in-place trends.

- Floor and mobile lifts accounted for USD 1.14 Billion in 2025 revenue as emergency departments and home-care agencies expanded their portable transfer fleets.

• By Mechanism

- Powered systems held 84.5% of the patient lifting equipment market share in 2025, as battery technology improvements and caregiver injury reduction targets accelerated electrification.

- Manual lifts are forecast to grow at a 6.3% CAGR through 2035, retained primarily in cost-sensitive rural clinics and field-deployed humanitarian settings.

• By End User

- Hospitals accounted for 51.4% share of the patient lifting equipment market in 2025, concentrated in intensive care, surgical recovery, and bariatric wards.

- Home-care settings are advancing at an 18.6% CAGR during 2026–2035, fueled by patient preference for community-based recovery and payer-driven early discharge policies.

• By Region

- North America led the patient lifting equipment market with 41.3% share in 2025.

- Asia-Pacific is set to register the fastest CAGR of 16.4% to 2035, as government hospital construction programs and domestic manufacturing incentives accelerate.

Market Size and Forecast (2021–2035)

Market Research Future's estimates integrate bottom-up revenue modeling across 40+ countries, validated against distributor sell-through data, regulatory filings, and publicly reported manufacturer revenues. Historical values (2021–2024) rely on audited trade data; forecast values (2026–2035) employ scenario-weighted projections.