North America: Fastest growing healthcare system

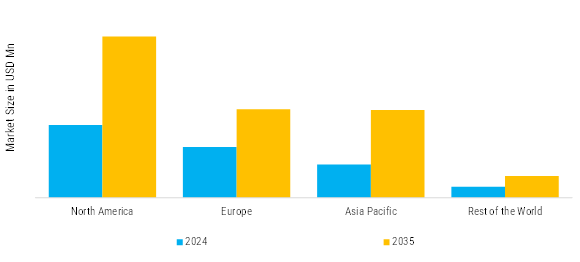

North America leads in the Medical Devices Market Size, accounting for over 40% of the global revenue in 2024. The United States leads with 32% share, driven by advanced healthcare infrastructure and high adoption of innovative technologies, while Canada holds 8% supported by strong public healthcare investments.

The United States holds the leadership position in the region market because of the presence of the major global vendors like Medtronic, Abbott, and Boston Scientific, as well as the developed ecosystem of innovation and clinical research. The market is growing at a high rate due to new investments in R&D and the speedy adoption of digital health technologies, including AI-based diagnostic tools, robotic-assisted surgery, and connected medical devices.

The increasing number of chronic illnesses such as cardiovascular diseases, diabetes and cancer is still generating the need of sophisticated diagnostic and treatment devices. Also, a growing trend toward home healthcare, distance monitoring and wearable medical equipment is transforming the way patients are served. Canada also makes some contribution, as there are favorable government policies regarding medical technology innovation and digitization of healthcare.

The U.S. Food and Drug Administration (FDA) regulatory control guarantees the quality, safety, and reliability of products, which results in a high level of consumer confidence. All in all, the technological leadership, patient awareness, and positive reimbursement structures in the region remain the key factors to its further dominance in the world medical devices market.

Europe: Emerging Medical Devices

Europe Medical Devices Market size was valued at USD 192569.70 million in 2024, making it the second-largest regional market with a 30% share. The aging population, chronic diseases, and high demand of early disease detection and minimal invasive curative measures contribute to the growth of the region. Germany, United Kingdom and France are the significant contributors, which are backed with strong healthcare facilities and extensive government spending on national health.

Germany dominates with 9% due to strong medical technology manufacturing, while the United Kingdom holds 7% driven by increasing digital health adoption.

The EU Medical Device Regulation (MDR) has increased the level of transparency and patient safety in the market, though it has amplified the compliance costs on manufacturers. European companies lead in innovation of imaging systems, orthopedic implants and heart devices.

In addition, the trend of digital transformation in all healthcare systems is promoting the use of artificial intelligence-based diagnostic technologies, wearable health gadgets, and e-health applications. Sustainability and environmentally friendly manufacture processes are also on the agenda of the region, which is in line with the Green Deal policies of the EU.

Asia-Pacific: Development of healthcare system

Asia-Pacific region is also the fastest-growing market with the medical devices due to the growth of healthcare infrastructures, urbanization and growing healthcare awareness. Some of the top contributors include China, Japan, India and South Korea, with the benefits of increased disposable incomes and government policies to streamline healthcare systems. The high number of patients and the increasing incidence of chronic illnesses such as diabetes and cardiovascular diseases in the region are increasing the demand of the inexpensive diagnostic and therapeutic equipment.

China leads with 9% with market value at USD 57,771 Million supported by rapid healthcare expansion, while India accounts for 5% driven by rising healthcare investments and patient population growth.

China and Japan are international manufacturing and innovation centers, and their domestic production is high, and they have substantial investment in AI-based healthcare technologies. In the meantime, the emerging medical device manufacturing ecosystem in India with the assistance of the Make in India program and healthcare policy reform is becoming a source of foreign investment. There is an upsurge in the adoption of portable and home-care medical devices because of affordability and enhanced accessibility.

Moreover, the emergence of online healthcare startups and telemedicine portals is improving the provision of healthcare in the rural and underserved regions. Medical tourism also helps in growing the market in the region, especially in Thailand, Singapore and India. The Asia-Pacific market is likely to be a major source of medical device innovation and volume production on the planet in the next few years as regulatory frameworks continue to mature and the spending on healthcare increases.

Rest of the World: Emerging good medical devices

Rest of the World (RoW) segment - Latin America, Middle East and Africa - are emerging as a good area to grow medical devices. The growth of the market is influenced by the advancement of the healthcare infrastructure, the increase in the level of awareness about the disease and the growth of investment in the modernization of the hospitals. The main markets include Brazil, Mexico, Saudi Arabia, the UAE, and South Africa because of the current healthcare reforms and governmental promotion of the use of medical technologies.

The growing rate of infectious diseases, chronic diseases, and surgery is generating high demand of diagnostic, respiratory, and general surgery equipment. Nevertheless, regulatory systems, lack of uniform reimbursement systems and reliance on imported devices hinder growth in some regions. These barriers notwithstanding, multinational medical device firms are increasing their regional presence by partnering, manufacturing locally and training.

Middle East is especially making aggressive investments in new hospital facilities and electronic health care, Africa and Latin America are enjoying the fruits of international assistance and government-business initiatives in healthcare. The development of medical tourism and the rise in the involvement of the private sector is likely to make the RoW market one of the most important growth horizons of the world medical devices industry in the coming decade.

Leave a Comment