Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Classification System | ICD, HCPCS, CPT, Others | International Classification of Diseases (ICD) | Medical Coding Market Common Procedure Code System (HCPCS) |

| Component | Outsourced Coding Services, In-House Coding Solutions | Outsourced Coding Services | In-House Coding Solutions |

| Delivery Mode | Web & Cloud-Based, On-Premise | Web & Cloud-Based | Web & Cloud-Based |

| End User | Hospitals, Physician Practices, Insurance Payers, Ambulatory Surgery Centers | Hospitals | Insurance Payers |

| Specialty Type | Radiology, Oncology, Cardiology, Orthopedics, Others | Radiology | Oncology |

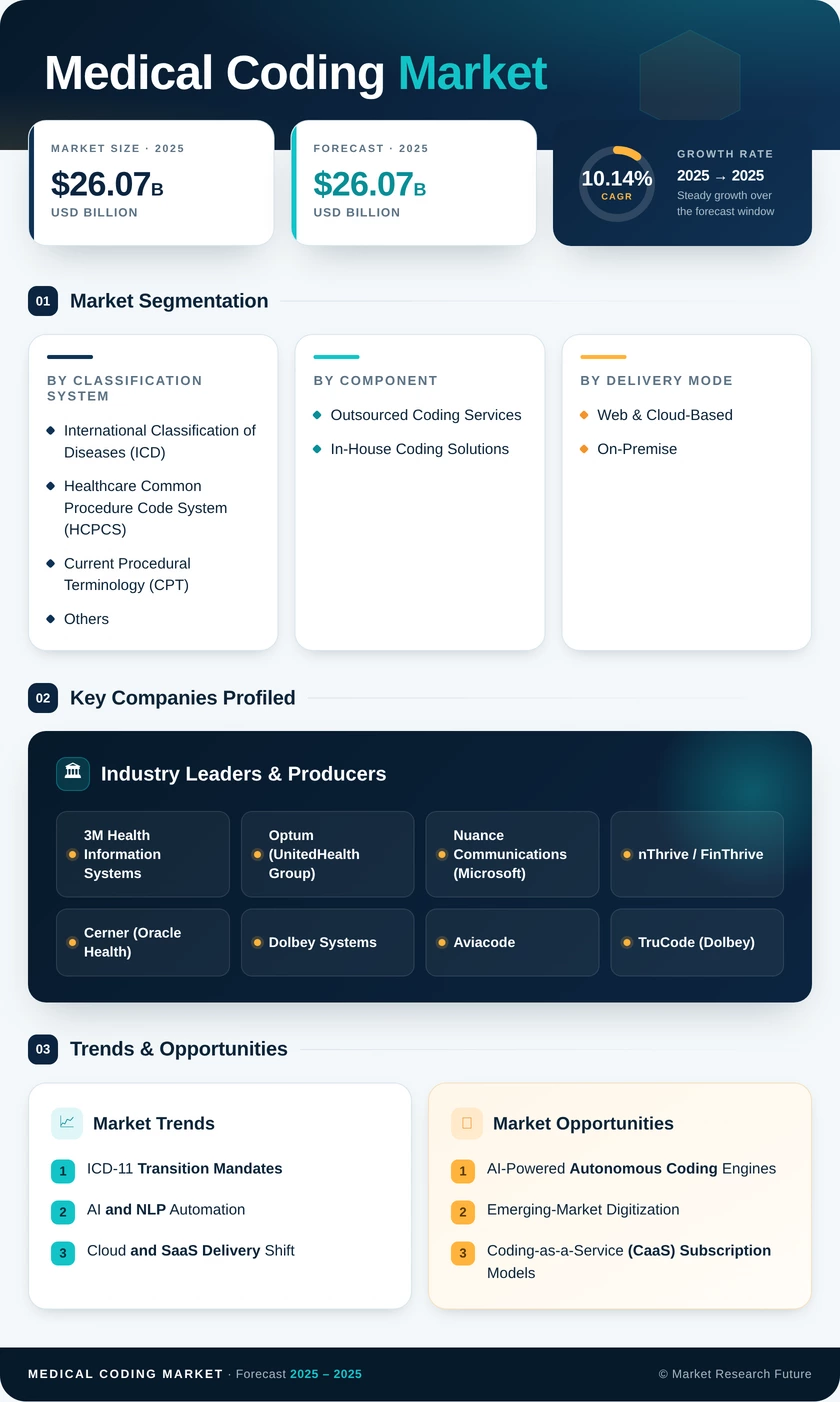

Market Segmentation Overview

By Classification System

| Sub-Segment | Key Trend |

| International Classification of Diseases (ICD) | ICD-11 transition driving upgrade investments globally; 71.2% share in 2025 |

| Medical Coding Market Common Procedure Code System (HCPCS) | Outpatient and ambulatory procedure growth is accelerating HCPCS adoption |

| Current Procedural Terminology (CPT) | Physician professional fee coding remains a core revenue-cycle function |

| Others | National and specialty classification systems for niche clinical domains |

The ICD classification system remains the backbone of the Medical Coding Market, underpinned by universal regulatory mandates for morbidity reporting. The ongoing ICD-11 transition is creating a multi-year investment cycle as health systems upgrade their diagnosis coding systems and retrain clinical documentation coding staff to accommodate post-coordination and extension-code logic.

By Component

| Sub-Segment | Key Trend |

| Outsourced Coding Services | Workforce shortages and cost efficiency are driving outsourcing demand |

| In-House Coding Solutions | AI-powered platforms enabling large health systems to internalize coding. |

Outsourced coding services dominate the component landscape as the persistent 30%+ coder shortfall compels providers to engage third-party CPT clinical code assignment specialists. In-house solutions are gaining traction among large integrated delivery networks that invest in proprietary AI engines for healthcare billing codes automation.

By Delivery Mode

| Sub-Segment | Key Trend |

| Web & Cloud-Based | Remote coding enablement; real-time regulatory update deployment |

| On-Premise | Legacy installations in data-sensitive environments; declining share |

Cloud platforms account for the majority of new deployments, enabling scalable, subscription-based access to ICD-10 procedure coding tools. On-premise solutions persist primarily in organizations with strict data sovereignty or regulatory constraints.

By End User

| Sub-Segment | Key Trend |

| Hospitals | Highest encounter complexity; DRG and case-mix coding requirements |

| Physician Practices | E/M coding and professional fee documentation |

| Insurance Payers | Pre-payment claims editing and fraud-detection analytics |

| Ambulatory Surgery Centers | Rapid outpatient volume growth is driving procedure-code adoption. |

Hospitals lead the end-user landscape due to the complexity and volume of inpatient diagnosis coding systems requirements. Insurance payers are the fastest-growing segment as they deploy advanced healthcare billing codes validation algorithms to reduce claims leakage.

By Specialty Type

| Sub-Segment | Key Trend |

| Radiology | High imaging volumes requiring precise CPT modality codes |

| Oncology | Complex multi-drug and immunotherapy regimen coding |

| Cardiology | Interventional and diagnostic procedure coding depth |

| Orthopedics | Surgical implant and device coding complexity |

| Others | Multi-specialty ambulatory and primary-care coding |

Radiology maintains the largest specialty share due to sheer imaging encounter volume and the CPT clinical code assignment intensity of modality-specific billing. Oncology is the fastest-growing specialty, as clinical documentation coding for immunotherapy, targeted therapy, and clinical-trial encounters requires increasingly granular diagnosis coding systems expertise.