Law Enforcement Software Market Summary

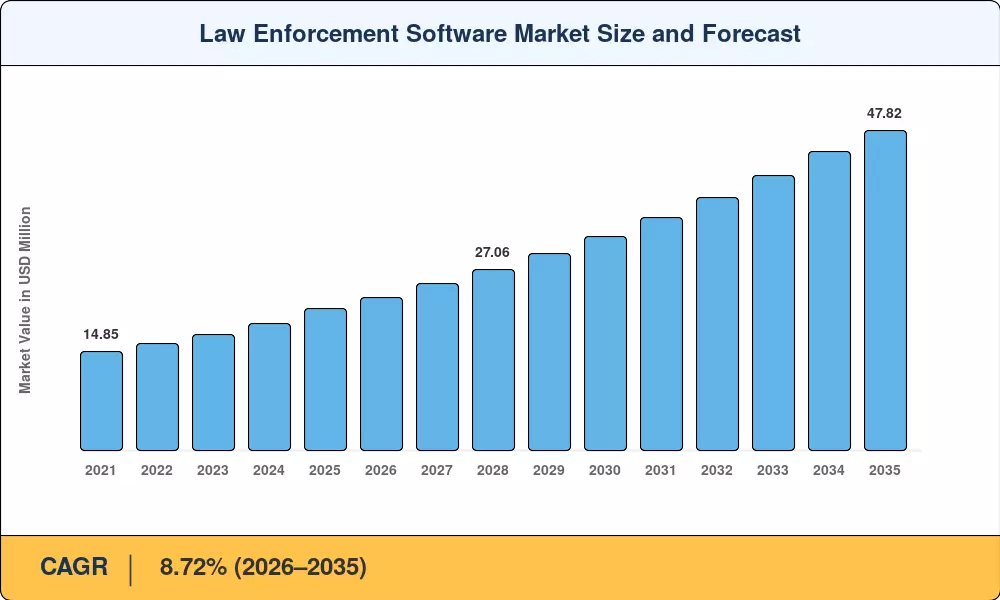

The Law Enforcement Software Market stood at an estimated USD 21.17 Billion in 2025, with the forecast period opening at USD 22.89 Billion in 2026 and climbing to USD 47.82 Billion by 2035 at an 8.72% CAGR. Persistent staffing shortages across police departments — the Police Executive Research Forum recorded a 65% increase in resignation rates since 2020 — have made automation of dispatch, records, and digital evidence management a budget priority rather than a discretionary upgrade [2]. Federal catalysts such as the Edward Byrne Memorial Justice Assistance Grant, which earmarked roughly USD 450 million for public safety technology improvements in 2025, are compressing procurement cycles and opening the law enforcement analytics pipeline for mid-sized agencies that previously relied on paper-based workflows [1].

Legacy client-server architectures built in the early 2000s are giving way to cloud-native platforms that unify crime investigation software, computer-aided dispatch, and body-worn-camera ingestion into a single evidence chain. The U.S. Department of Justice allocated over USD 280 million in 2024 toward CJIS-compliant cloud migration grants, signaling that on-premise holdouts face growing regulatory and interoperability pressure to modernize [3]. This shift is accelerating demand for police records management suites capable of real-time data sharing across jurisdictions.

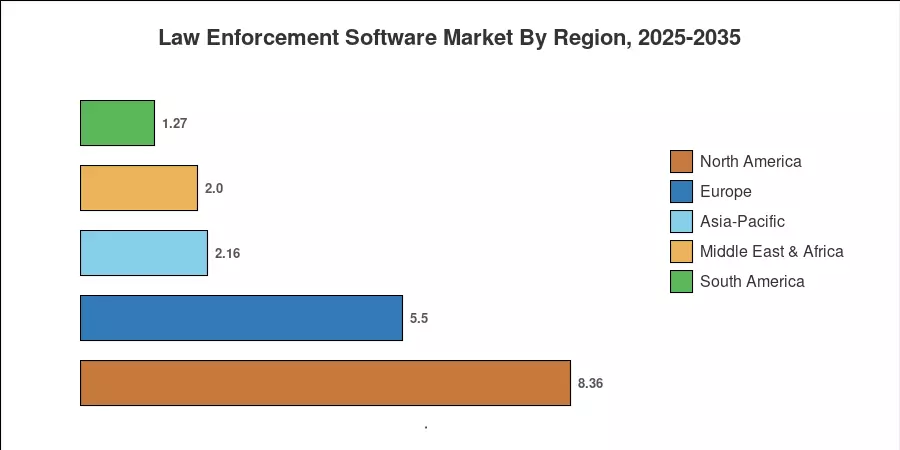

North America commands approximately 39.5% of the Law Enforcement Software Market, anchored by the United States' massive installed base and federal grant infrastructure Asia-Pacific is the fastest-growing region, projected at a 10.18% CAGR through 2035, driven by India's Safe City Programme and China's Xueliang (Sharp Eyes) surveillance expansion [4]. Europe holds the second-largest share at roughly 26%, where EU data-sovereignty mandates are reshaping vendor hosting strategies. The next decade will reward public safety software tools providers that balance analytics depth with strict compliance frameworks.

Key Report Takeaways

• By Solution

- Computer-aided dispatch platforms captured a leading 26.2% revenue share of the Law Enforcement Software Market in 2025, reflecting the mission-critical nature of real-time call routing and officer allocation

- Predictive and crime analytics solutions are on track for a 10.22% CAGR through 2035, as agencies invest in law enforcement analytics to pre-empt crime hotspots

- Digital evidence management platforms reached USD 3.78 Billion in 2025, fueled by body-camera mandates and rising video data volumes

• By Deployment & Component

- On-premise deployment held 62.4% of the Law Enforcement Software Market in 2025, though cloud adoption is accelerating rapidly

- Cloud deployment is pacing an 11.07% CAGR to 2035 as CJIS Security Policy updates enable FedRAMP-authorized hosting

- Software accounted for 75.3% of component revenue, while managed services are growing at a 9.85% CAGR

• By End User & Geography

- Municipal and local agencies represented 49.1% of demand in the Law Enforcement Software Market, reflecting the sheer number of sub-federal departments

- Federal and national police agencies are the fastest-growing end-user cohort at a 10.82% CAGR

- Asia-Pacific's 10.18% CAGR outpaces all other regions, with North America maintaining the largest absolute revenue base

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines bottom-up vendor revenue modeling with top-down macroeconomic benchmarking. Historical data (2021–2024) draws on agency procurement disclosures, vendor annual filings, and freedom-of-information requests. Forecast values (2026–2035) apply a calibrated CAGR anchored to grant funding trajectories, cloud migration timelines, and demographic policing demand curves.