Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Connectivity | USB, NFC, Bluetooth, Others | USB (42.3% share, 2025) | NFC (24.2% CAGR) |

| By Wallet Type | Cold Wallet, Hot Wallet | Cold Wallet (59.2% share, 2025) | Hot Wallet (21.6% CAGR) |

| By End User | Individual/Retail, Institutional/Enterprise | Individual/Retail (67.1% share, 2025) | Institutional/Enterprise (25.3% CAGR) |

| By Distribution Channel | Online, Offline | Online (55.8% share, 2025) | Offline (24.9% CAGR) |

| By Region | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (36.0% share, 2025) | Asia-Pacific (26.1% CAGR) |

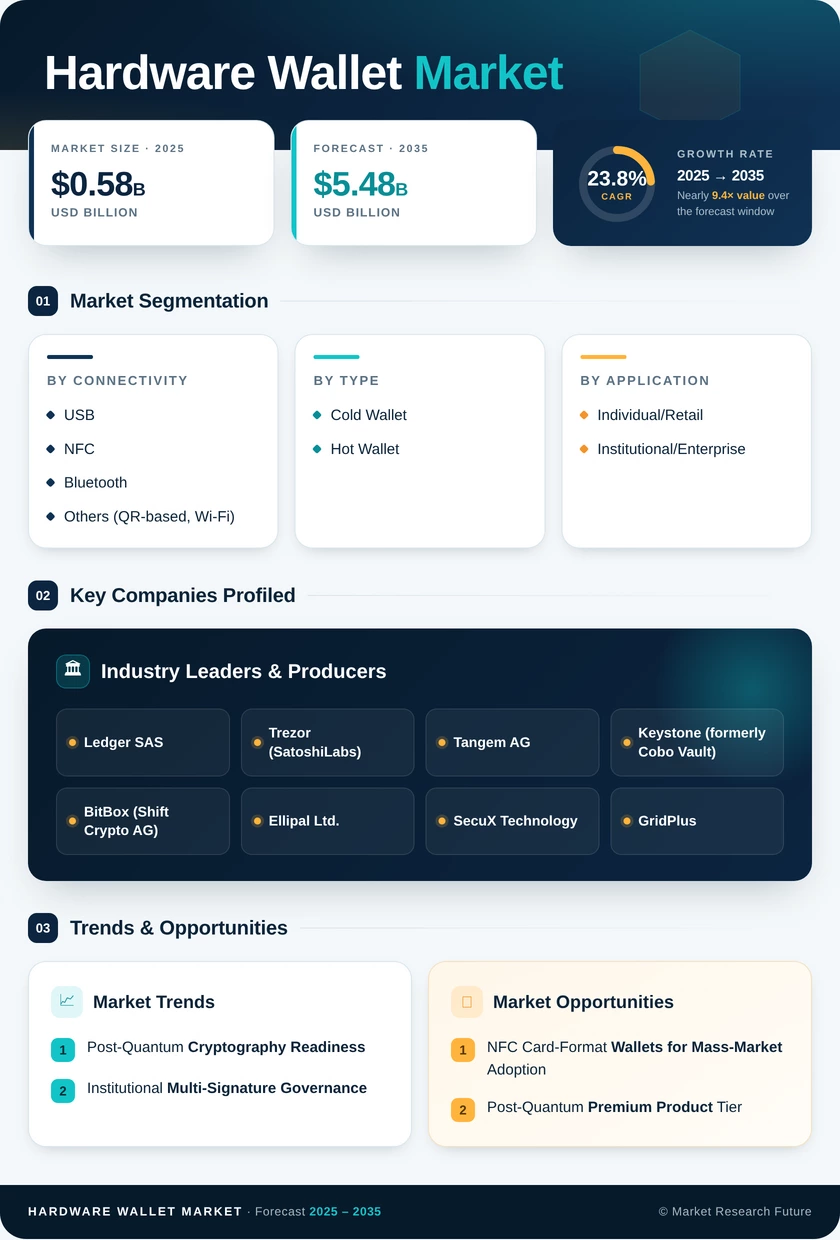

Market Segmentation Overview

By Connectivity

| Sub-Segment | Key Trend |

| USB | Remains the enterprise standard for air-gapped custody workflows; growth decelerating as wireless alternatives mature |

| NFC | Credit-card form factor driving mass-market adoption; smartphone tap-to-sign simplifies onboarding |

| Bluetooth | Mobile-first retail buyers prefer wireless pairing; Ledger Nano X leads this segment |

| Others (QR-based, Wi-Fi) | Niche institutional and IoT custody use cases; Keystone leads air-gapped QR-code signing |

USB connectivity continues to anchor enterprise procurement in the Hardware Wallet Market, but NFC card wallets are rapidly reshaping the retail landscape by eliminating cable-based friction and reducing device costs to sub-USD 40 price points.

By Wallet Type

| Sub-Segment | Key Trend |

| Cold Wallet | Regulatory mandates (MiCA, OCC) position cold storage as the compliance baseline for custody providers |

| Hot Wallet | DeFi power users and yield-farming protocols drive demand for hardware-secured hot wallet signing |

Cold wallets remain the structural backbone of the Hardware Wallet Market as global regulators codify offline key storage as a minimum custodial standard. Hot wallet hardware serves a smaller but fast-growing niche of DeFi-active users.

By End User

| Sub-Segment | Key Trend |

| Individual/Retail | Self-custody pivot post-exchange failures; NFC cards and sub-USD 50 devices expanding addressable base |

| Institutional/Enterprise | Multi-signature governance, custody-as-a-service bundling, and EAL 5+ certification requirements |

Retail users dominate unit volumes, while institutional buyers drive premium ASPs through multi-device quorum deployments and compliance-grade procurement cycles.

By Distribution Channel

| Sub-Segment | Key Trend |

| Online | Direct-to-consumer e-commerce dominates; supply-chain integrity and authenticity verification are key differentiators |

| Offline | Electronics retailers expanding crypto hardware shelf space; carrier-bundled NFC card wallets emerging |

Online channels remain dominant to mitigate counterfeit risks, but offline retail is the fastest-growing distribution mode as mainstream electronics chains onboard hardware wallet SKUs.

By Region

| Sub-Segment | Key Trend |

| North America | OCC/FDIC guidance, venture-funded startup ecosystem, institutional custody concentration |

| Europe | MiCA compliance deadlines, Ledger's France-based supply chain, EAL certification demand |

| Asia-Pacific | Regulatory sandboxes, exchange-bundled device sales, massive untapped retail crypto user base |

| South America | Macroeconomic instability driving stablecoin self-custody; Brazil leads regional adoption |

| Middle East & Africa | VARA licensing, sovereign wealth fund crypto pilots, CBDC custody infrastructure development |

North America leads the Hardware Wallet Market by revenue share, but Asia-Pacific's combination of regulatory momentum and a 93-million-strong retail crypto base in India alone makes it the fastest-growing region through 2035.