Coalescing Agents Market Summary

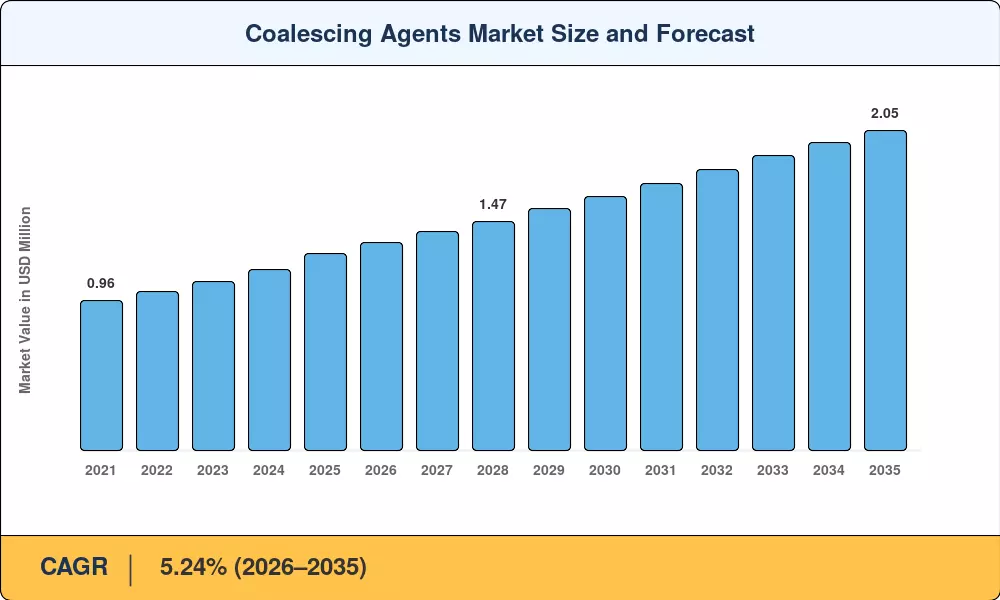

The Coalescing Agents Market reached an estimated USD 1.26 billion in 2025, with the forecast period beginning at USD 1.33 billion in 2026 and climbing to USD 2.05 billion by 2035 at a compound annual growth rate of 5.24%. Stricter volatile-organic-compound (VOC) regulations across North America and Europe — including the U.S. EPA's updated aerosol coating limits effective 2026 and the EU Paints Directive revision — are pushing coating formulators to adopt advanced waterborne coating additives at an accelerated pace [1]. Capital commitments exceeding USD 4.8 billion in new latex and acrylic dispersion capacity announced between 2023 and 2025 signal robust demand for film forming agents and related paint performance chemicals over the coming decade [2].

A structural shift is underway in how architectural and industrial coatings are formulated. Legacy solvent-borne systems that relied on high-VOC coalescent blends are giving way to low VOC coating additives engineered from ester- and diol-based chemistries. The European Coatings Association estimates that waterborne formulations now account for over 62% of new architectural paint launches in the EU, up from 48% in 2019 [3]. This transition compels producers of coating formulation chemicals to invest in next-generation hydrophilic and hydrophobic coalescents that deliver comparable film integrity at lower minimum film-forming temperatures.

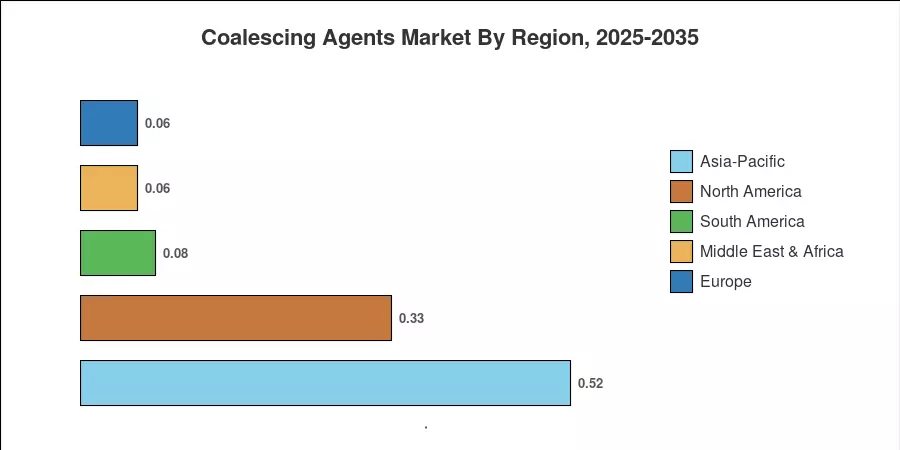

Asia-Pacific commands the largest share of the Coalescing Agents Market at roughly 41% of 2025 revenue, driven by China and India's expanding construction sectors and favorable feedstock economics. The region also posts the fastest CAGR of 5.71% through 2035. North America holds the second-largest position with approximately 26% share, buoyed by stringent EPA mandates that accelerate adoption of specialty coating materials. Europe follows closely, anchored by its mature regulatory framework and demand for sustainable latex paint additives. As green-building certifications proliferate globally, consumption of paint additives and industrial coating chemicals will continue to broaden across emerging economies

Key Report Takeaways

• By Type

- Hydrophobic agents held a dominant 64.3% share of the Coalescing Agents Market in 2025, reflecting their superior compatibility with acrylic and vinyl-acrylic latex systems

- Hydrophilic agents are projected to grow at a 5.93% CAGR through 2035, supported by rising demand in personal care emulsions and waterborne coating additives

• By Chemistry

- Alcohols accounted for USD 0.55 billion within the Coalescing Agents Market in 2025, underpinned by cost-effective glycol-ether intermediates

- Esters are forecast to expand at a 5.75% CAGR to 2035, gaining ground as preferred low VOC coating additives in architectural formulations

• By Application

- Paints and coatings commanded 49.1% of 2025 demand, reinforcing the sector's role as the backbone of the Coalescing Agents Market

- Personal care applications are set to grow at a 6.15% CAGR through 2035, propelled by clean-beauty reformulation trends

• By Region

- Asia-Pacific captured roughly 41% of global revenue in 2025 and leads the Coalescing Agents Market with a 5.71% CAGR through 2035

- North America contributed approximately USD 0.33 billion in 2025, supported by regulatory catalysts for paint performance chemicals

Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model integrates bottom-up production volume data from 38 countries, trade-flow analysis of key glycol-ether and ester intermediates, and top-down validation against coatings industry output figures published by IPPIC, the American Coatings Association, and regional equivalents. Historical figures are reconciled with customs data; forecast values apply a blended CAGR anchored to construction spending indices, automotive OEM output, and regulatory adoption curves for low VOC coating additives.