Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

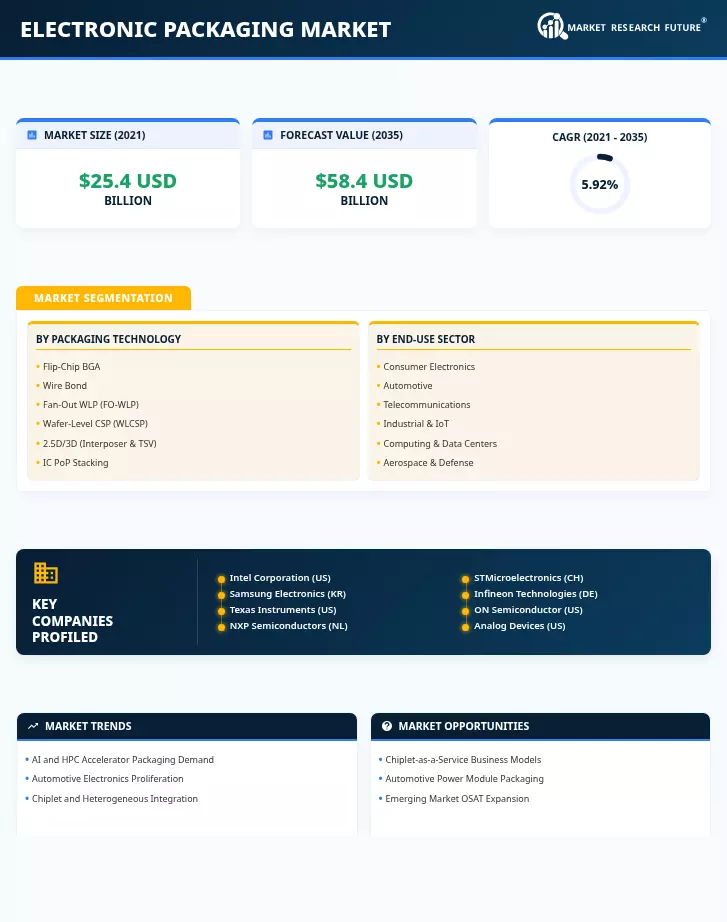

| By Packaging Technology | Flip-Chip BGA; Wire Bond; Fan-Out WLP (FO-WLP); Wafer-Level CSP (WLCSP); 2.5D/3D (Interposer & TSV); IC PoP Stacking | Flip-Chip BGA (31% share) | 2.5D/3D Interposer & TSV (9.1% CAGR) |

| By End-Use Sector | Consumer Electronics; Automotive; Telecommunications; Industrial & IoT; Computing & Data Centers; Aerospace & Defense | Consumer Electronics (34% share) | Automotive (7.5% CAGR) |

Market Segmentation Overview

By Packaging Technology

| Sub-Segment | Key Trend |

| Flip-Chip BGA | Dominant in data center and HPC; substrate innovation (glass core) on horizon |

| Wire Bond | Legacy cost leader; declining share but persistent in MCU, analog, discrete |

| Fan-Out WLP (FO-WLP) | Fastest package-level growth; expanding from mobile into automotive and RF |

| Wafer-Level CSP (WLCSP) | Compact, substrate-less; strong in PMIC, MEMS, and wearable devices |

| 2.5D/3D (Interposer & TSV) | Highest complexity; driven by AI GPU and HBM integration requirements |

| IC PoP Stacking | Stable mobile niche; evolving toward hybrid bonding 3D architectures |

Flip-chip BGA and wire bond collectively account for over half of the Electronic Packaging Market's revenue, reflecting the industry's reliance on mature high-volume technologies. Growth, however, is concentrating in fan-out wafer-level packaging FO-WLP and 2.5D/3D integration, where advanced interconnect density requirements from AI, automotive, and next-generation communications create sustained demand for premium packaging platforms.

By End-Use Sector

| Sub-Segment | Key Trend |

| Consumer Electronics | Volume anchor; complexity per device rising even as unit growth plateaus |

| Automotive | Fastest-growing sector; 800V EV drivetrains and ADAS sensors driving premium packaging |

| Telecommunications | 5G mmWave AiP and fiber optic module packaging underpin stable mid-single-digit growth |

| Industrial & IoT | Edge AI and smart metering expanding wafer-level chip scale packaging WLCSP adoption |

| Computing & Data Centers | AI accelerator and HBM packaging creating the highest ASP tier in the market |

| Aerospace & Defense | Radiation-hardened and hermetic packaging requirements sustain premium pricing |

The Electronic Packaging Market's end-use distribution is shifting from consumer electronics volume dominance toward a more balanced profile, as automotive and data center segments grow at nearly double the market average. This rebalancing elevates average selling prices across the industry and rewards OSATs with advanced multi-chip module MCM advanced packaging and IC package-on-package PoP stacking capabilities.