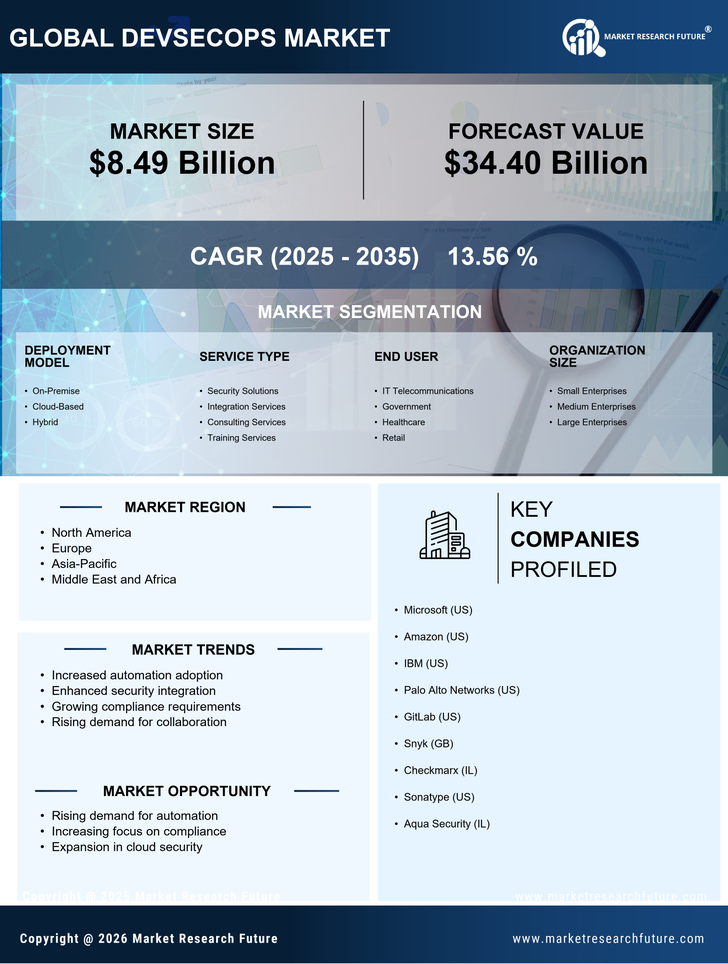

MARKET SEGMENTATION OVERVIEW

The global DevSecOps market is analyzed across four primary segmentation dimensions. Each dimension reflects distinct demand drivers, regulatory treatment, and end-user requirements, enabling granular revenue forecasting and strategic positioning for market participants.

By Offering

| Sub-Segment | Key Trend |

| Solutions | Unified platforms combining SAST, DAST, SCA, and IaC scanning gaining share |

| Services — Professional Services | Implementation consulting and pipeline integration advisory |

| Services — Managed Services | Outsourced AppSec operations for talent-constrained mid-market firms |

Solutions remain the largest sub-segment (~76% share in 2025) as enterprises consolidate point tools into integrated platforms. Managed Services (27.10% CAGR) is the fastest-growing sub-segment as organizations lacking in-house AppSec specialists outsource pipeline security operations to managed providers.

By Deployment Model

| Sub-Segment | Key Trend |

| Cloud | Kubernetes-native stacks driving SaaS-based DevSecOps adoption |

| On-Premise | Defense, intelligence, and banking mandating air-gapped environments |

| Hybrid | Gradual migration strategies bridging on-prem and cloud workloads |

On-premise installations hold majority share (~53% in 2025) driven by data-sovereignty requirements in defense and financial verticals. Cloud deployments (28.50% CAGR) are the fastest-growing model as container security scanning becomes inseparable from cloud-native application stacks.

By End-User Enterprise Size

| Sub-Segment | Key Trend |

| Large Enterprises | Complex multi-cloud environments and stringent compliance mandates |

| Small & Medium Enterprises (SMEs) | SaaS-based affordable tooling with consumption-based pricing models |

Large enterprises command ~62% share in 2025, driven by regulatory compliance obligations and scale. SMEs represent the faster-growing segment (25.80% CAGR) as vendors introduce consumption-based pricing that lowers the barrier to shift-left security adoption.

By End-User Industry

| Sub-Segment | Key Trend |

| IT & Telecom | Most mature CI/CD pipelines; highest code deployment frequency |

| BFSI | DORA, PCI DSS 4.0 compliance driving fastest vertical growth |

| Manufacturing | OT/IT convergence demanding pipeline-embedded firmware security |

| Healthcare | HIPAA modernization and connected medical device security |

| Government & Defense | EO 14028, FedRAMP mandates requiring SBOM attestation |

| Others | Education, retail, energy digital transformation initiatives |

IT & Telecom leads with ~30% revenue share in 2025 due to mature CI/CD ecosystems. BFSI is the fastest-growing vertical (26.90% CAGR), propelled by Europe's DORA and global PCI DSS 4.0 mandates requiring continuous security testing across ICT service providers.

SEGMENTATION QUICK REFERENCE

| Dimension | Sub-Segments | Dominant Segment (2025) | Fastest Growing |

| Offering | Solutions · Professional Services · Managed Services | Solutions (~76%) | Managed Services (27.10%) |

| Deployment Model | Cloud · On-Premise · Hybrid | On-Premise (~53%) | Cloud (28.50%) |

| Enterprise Size | Large Enterprises · SMEs | Large Enterprises (~62%) | SMEs (25.80%) |

| End-User Industry | IT & Telecom · BFSI · Manufacturing · Healthcare · Gov & Defense · Others | IT & Telecom (~30%) | BFSI (26.90%) |