Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Landing Gear Type | Main Landing Gear, Nose Landing Gear | Main Landing Gear | Nose Landing Gear |

| Aircraft Type | Narrowbody, Widebody, Regional Jet | Narrowbody | Widebody |

| End User | Original Equipment Manufacturer (OEM), Aftermarket | OEM | Aftermarket |

| Sub-System | Structural, Actuation System, Steering System, Others | Structural | Actuation System |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | South America | Asia-Pacific |

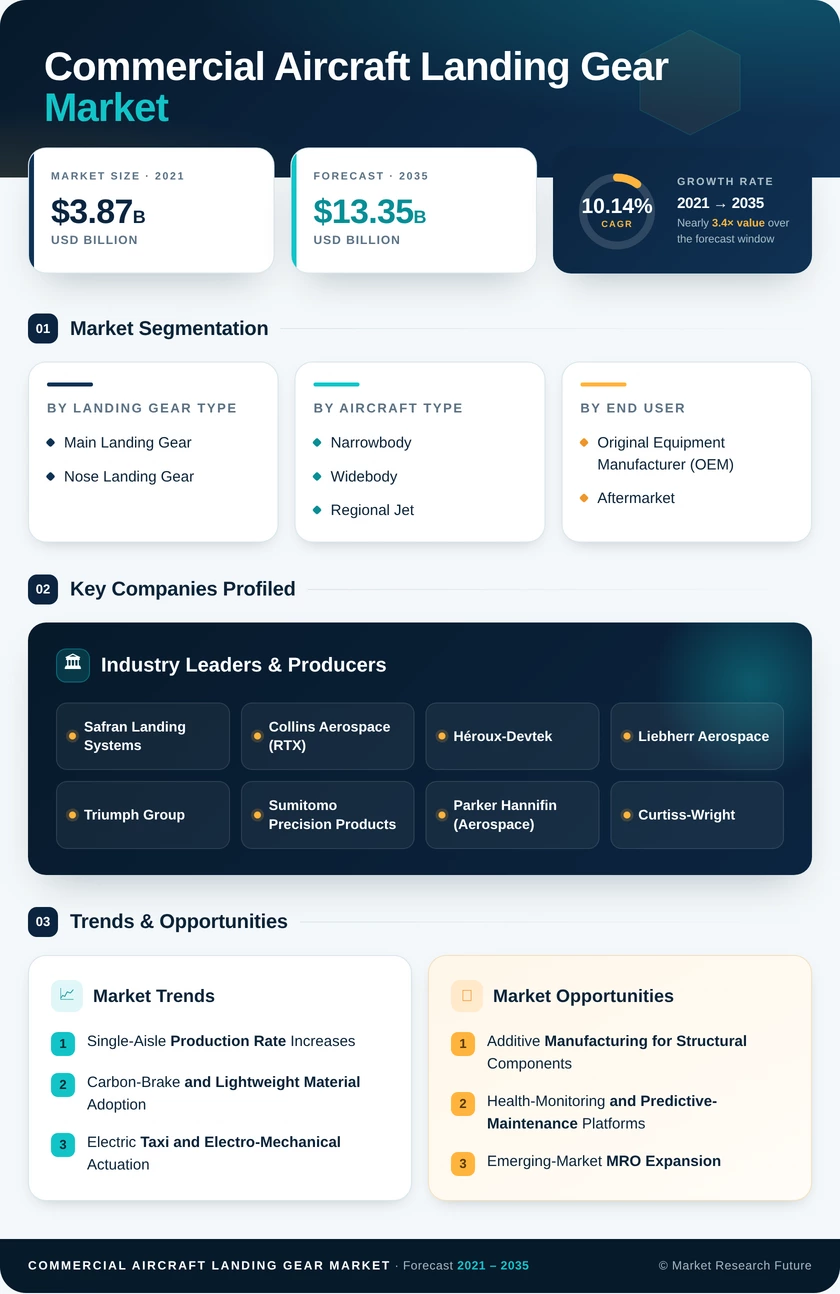

Market Segmentation Overview

By Landing Gear Type

| Sub-Segment | Key Trend |

| Main Landing Gear | Multi-wheel bogie designs incorporating carbon brakes and electric actuators drive premium pricing and account for the majority of per-aircraft gear spend. |

| Nose Landing Gear | Electric nose-wheel taxi retrofits and advanced steerable electronics position nose gear as the fastest-growing type segment through 2035 |

Main landing gear remains the revenue anchor due to structural complexity and higher component count per assembly. Nose gear is transitioning from a relatively commoditized assembly to a technology-rich platform as electric taxi systems gain regulatory approval and airline adoption.

By Aircraft Type

| Sub-Segment | Key Trend |

| Narrowbody | Record A320neo and B737 MAX production rates sustain narrowbody dominance across OEM and aftermarket channels. |

| Widebody | Long-haul fleet renewal by Gulf and Asian carriers drives above-average growth for high-value twin-aisle gear systems. |

| Regional Jet | Embraer E2-family production and next-generation regional programs maintain steady but smaller gear demand. |

Narrowbody gear procurement volumes dwarf other aircraft types due to monthly production rates exceeding 100 combined units across Airbus and Boeing. Widebody gear carries the highest per-unit value, making it the fastest-growing segment by revenue growth rate.

By End User

| Sub-Segment | Key Trend |

| Original Equipment Manufacturer (OEM) | Unprecedented backlogs exceeding 14,000 aircraft secure multi-year OEM gear procurement visibility |

| Aftermarket | Over 8,500 aging A320ceo and B737NG aircraft entering heavy-maintenance cycles accelerate aftermarket growth. |

OEM contracts currently capture the majority share, but the aftermarket is gaining ground as previous-generation narrowbody fleets mature. Power-by-the-hour agreements and independent Commercial Aircraft Landing Gear Market competition are reshaping aftermarket economics.

By Sub-System

| Sub-Segment | Key Trend |

| Structural | Titanium and high-strength steel forgings for gear legs and bogie beams command the largest sub-system share. |

| Actuation System | Electro-hydrostatic and electro-mechanical actuator adoption drives the fastest growth among sub-systems. |

| Steering System | Electronic nose-wheel steering upgrades replace legacy hydraulic systems on both new-build and retrofit programs. |

| Others (Brakes, Wheels, Sensors) | Carbon-brake retrofits and health-monitoring sensor integration expand the addressable content per aircraft. |

Structural components anchor sub-system revenue due to material intensity and forging complexity. Actuation systems are undergoing a generational shift from hydraulic to electric architectures that will redefine supplier positioning over the forecast period.