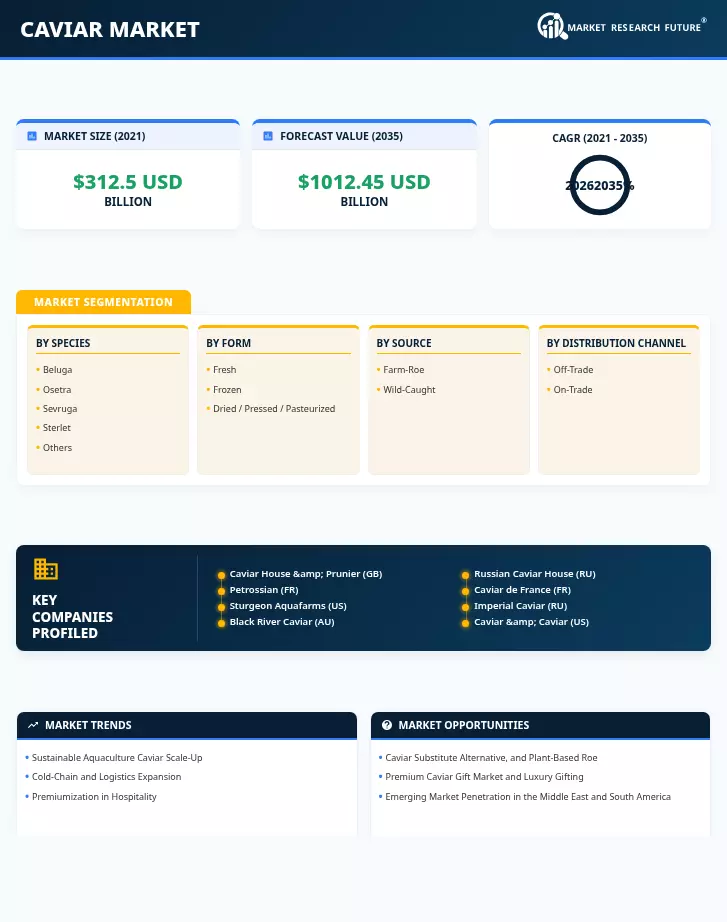

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Species | Beluga, Osetra, Sevruga, Sterlet, Others | Beluga | Sevruga |

| By Form | Fresh, Frozen, Dried / Pressed / Pasteurized | Fresh | Frozen |

| By Source | Farm-Roe, Wild-Caught | Farm-Roe | Wild-Caught |

| By Distribution Channel | Off-Trade, On-Trade | Off-Trade | On-Trade |

| By Region | North America, Europe, Asia-Pacific, South America, Middle East & Africa | Asia-Pacific | Europe |

Market Segmentation Overview

By Species

| Sub-Segment | Key Trend |

| Beluga | Ultra-premium positioning sustained by scarcity and CITES restrictions on Huso huso |

| Osetra | Fastest-scaling farm-raised species; versatile flavor profile drives culinary adoption |

| Sevruga | Competitive pricing from new aquaculture capacity; the strongest forecast CAGR in the species category |

| Sterlet | Entry-level sturgeon roe; gateway product for new consumers in emerging markets |

| Others | Paddlefish, hackleback, and bowfin roe serve regional niche demand in North America |

Beluga's dominance reflects its heritage status in the caviar hierarchy, though supply constraints have shifted production investment toward osetra and sevruga. Sevruga's rapid growth stems from shorter maturation cycles relative to beluga, making it economically attractive for farm operators.

By Form

| Sub-Segment | Key Trend |

| Fresh | Preferred by chefs and connoisseurs; limited shelf life drives premium pricing |

| Frozen | Blast-freezing technology enables e-commerce distribution and long-range export |

| Dried / Pressed / Pasteurized | Shelf-stable formats growing in ingredient use, gifting, and airline catering |

Fresh roe commands the highest per-gram price and represents the majority of consumption by volume. Frozen formats are closing the quality gap through rapid-chill innovations, unlocking direct-to-consumer channels and cross-border trade.

By Source

| Sub-Segment | Key Trend |

| Farm-Roe | Dominates production; ESG certifications (ASC, organic) are increasingly standard |

| Wild-Caught | Tiny base but strong growth as Caspian quotas cautiously expand under CITES |

Farm-roe's near-total dominance is a direct consequence of the 2006 CITES moratorium on wild Caspian harvests, which accelerated aquaculture investment globally. Wild-caught roe commands extreme premiums and functions as a heritage-branding asset.

By Distribution Channel

| Sub-Segment | Key Trend |

| Off-Trade | Retail, specialty stores, and e-commerce; DTC brands are gaining share rapidly |

| On-Trade | Hotels, airlines, fine-dining restaurants; fastest CAGR driven by premiumization |

Off-trade channels benefit from e-commerce growth and holiday gifting demand, while on-trade venues leverage caviar as an experiential differentiator in luxury hospitality settings.

By Region

| Sub-Segment | Key Trend |

| North America | DTC e-commerce growth; domestic sturgeon farming expansion in California and Florida |

| Europe | Fastest-growing region; heritage consumption in France, production scale-up in Italy and Spain |

| Asia-Pacific | Largest market; China dominates global sturgeon farming; Japan drives premium import demand |

| South America | Nascent market led by Brazil's luxury dining scene; early-stage farming trials in Argentina |

| Middle East & Africa | Tourism-driven demand centered in the UAE and Saudi Arabia; high per-capita hotel consumption |

Asia-Pacific's production leadership and Europe's consumption-side premiumization together define the global competitive axis. Emerging regions offer high growth rates from small bases, driven primarily by luxury hospitality expansion.