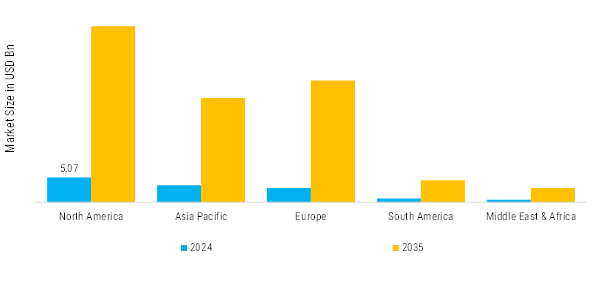

Based on region, the Global Commercial Heat-Treating Market is segmented into North America, Europe, Asia-Pacific, South America and Middle East and Africa. North America accounted for the largest market share in 2024 and is anticipated to reach USD 5.07 Billion by 2035. Asia-Pacific is projected to grow at the highest CAGR of 6.82% during the forecast period.

North America: Growing Strong manufactures

Binder’s market possesses a vast infrastructure, strong manufacturing base, and varied end-use industries that include construction, automotive, packaging, and education. In both locations, binders such as industrial adhesive for construction, asphalt binder for construction, and paper binder for office use can be sold indirectly or directly. Direct sales are more often the norm in industrial applications, either with end-users such as government departments or construction companies buying binder products directly from manufacturers.

South America: Emerging automotive Sectors

In the case of the United States, one can name a few agencies, like the Federal Highway Administration and various state Departments of Transportation, that require specific performance grades for asphalt binders that are used in road construction, leading to direct sales of these binders with certified suppliers on a contract basis. The requirement in the automotive and aerospace sectors to get industrial-grade adhesives for performance and compliance often leads them to procure these products directly from the manufacturers. In Canada, too, public infrastructure projects are directed purchases from provincial and federal tenders that contract pre-qualified suppliers, especially for very large construction or transportation infrastructure projects. But for commercial and consumer purposes, we see more of indirect sales. School binders, general-purpose adhesives, and packaging-related bonding agents are mostly distributed through distributors, wholesalers, retail chains, and online platforms.

Europe: Access Binders Gain Development

The education sector, the office, and the home usually gain access to binder products in smaller quantities via retailers and third-party suppliers. Indeed, indirect importation accounts for a sizeable share of consumer-grade binder products sourced mainly by Canada from U.S.-based manufacturers. This supply chain is, of course, assured by a speedy flow across the borders due to convenient trade regulations and logistics systems that allow timely and widespread distribution.

Middle-East & Africa: Growing food packaging

Middle-East & Africa placed priority on product quality and safety through their regulatory frameworks, which in turn have some bearing on the sourcing and distribution of binders. For instance, adhesives-makers destined for the food packaging or medical application markets will have some labelling and compliance requirements to conform to that will influence the choice of selling either directly to clients or certified intermediaries.

Asia-Pacific: Large Scale technical Binders

Binder’s market is characterized by a maturation level with great regulation in which direct sales have a large influence in large-scale technical applications and where indirect sales have stepped into play and enabled consumer and small-business use of binders.