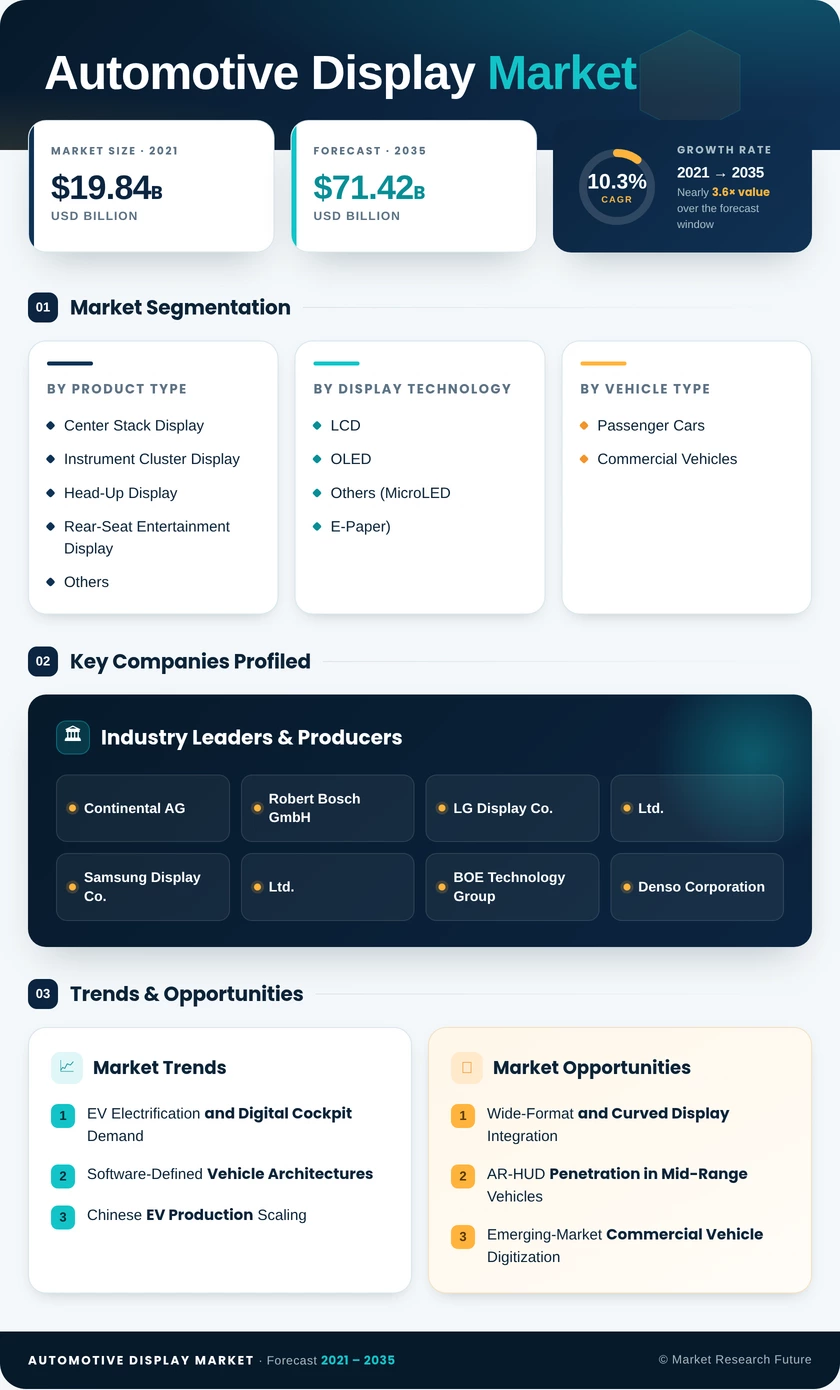

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Product Type | Center Stack Display, Instrument Cluster Display, Head-Up Display, Rear-Seat Entertainment Display, Others | Center Stack Display | Head-Up Display |

| Display Automotive Display Market | LCD, OLED, Others (MicroLED, E-Paper) | LCD | OLED |

| Vehicle Type | Passenger Cars, Commercial Vehicles | Passenger Cars | Commercial Vehicles |

| Display Size | ≤5-Inch, 6–10 Inch, >10 Inch | 6–10 Inch | >10 Inch |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | Asia-Pacific | Asia-Pacific |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Center Stack Display | Migration from 8-inch to 12–15 inch panels; integration of HVAC and vehicle settings |

| Instrument Cluster Display | Replacement of analog gauges with fully digital reconfigurable clusters |

| Head-Up Display | AR-HUD waveguide combiners enabling navigation overlay on windshield |

| Rear-Seat Entertainment Display | Premium-segment growth driven by passenger content consumption |

| Others | Electronic mirror replacements and pillar-mounted information displays |

Center stack displays continue to absorb the largest share of OEM display budgets. Screen sizes are trending upward across all vehicle tiers, with wide-format and portrait-orientation panels becoming standard in new EV architectures.

By Display Automotive Display Market

| Sub-Segment | Key Trend |

| LCD | Cost-efficient workhorse technology with mature supply chain; dominates volume segments |

| OLED | Superior contrast and flexibility enabling curved form factors; ASPs declining with Gen 8.5 ramp |

| Others (MicroLED, E-Paper) | Early-stage adoption for ambient lighting accents and low-power instrument displays |

LCD maintains its dominant position on the strength of established manufacturing capacity and favorable pricing. OLED is closing the cost gap and gaining spec-in wins across premium and upper-mid-range vehicle platforms.

By Vehicle Type

| Sub-Segment | Key Trend |

| Passenger Cars | Consumer-driven demand for digital cockpits; EV platforms increasing display content |

| Commercial Vehicles | Regulatory mandates for digital tachographs and telematics dashboards driving adoption |

Passenger cars account for the vast majority of display revenue, but commercial vehicles represent the fastest-growing segment as fleet operators face mandatory digitization requirements across multiple jurisdictions.

By Display Size

| Sub-Segment | Key Trend |

| ≤5-Inch | Declining share as rear-camera and secondary displays migrate to larger formats |

| 6–10 Inch | Mainstream cluster and center stack size; high-volume workhorse category |

| >10 Inch | Fastest growing driven by wide-format panoramic and curved display architectures |

The shift toward larger display sizes reflects both consumer expectation and OEM strategy. Panels exceeding 10 inches deliver higher ASPs and serve as visible differentiators on showroom floors, incentivizing automakers to specify them across expanding model lineups.