Dimethylaminopropylamine Market Summary

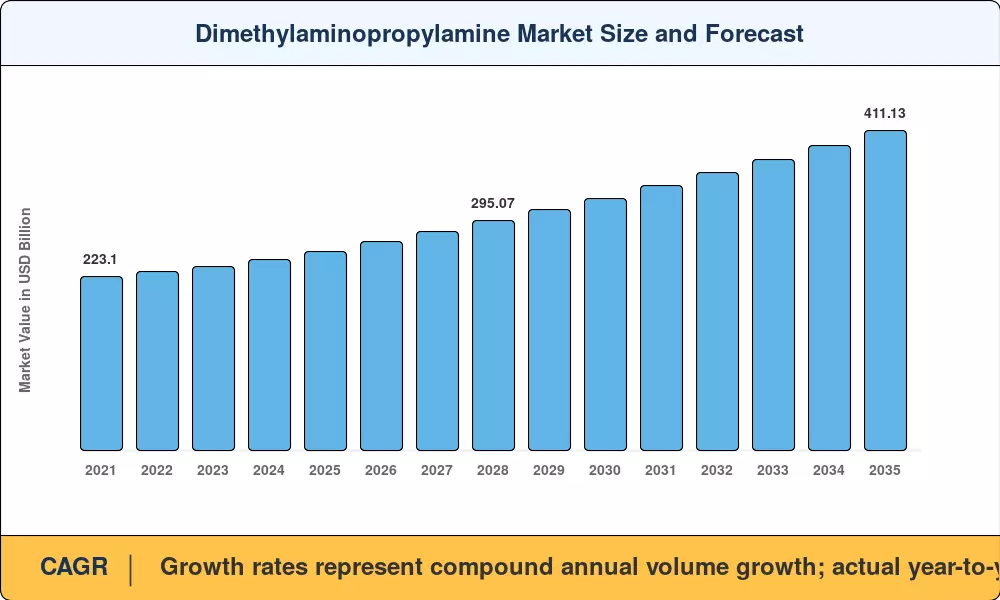

The Dimethylaminopropylamine Market reached an estimated 256.00 kilotons in 2025 and is projected to grow from 268.41 kilotons in 2026 to 411.13 kilotons by 2035, registering a CAGR of 4.85% across the forecast period. Demand acceleration is anchored in two structural catalysts: tightening wastewater discharge standards under the EU Urban Wastewater Treatment Directive recast and the rapid reformulation of personal-care products toward sulfate-free, betaine-based surfactant systems. Both forces channel incremental volume directly through DMAPA-derived intermediates, creating sustained pull across geographies [1][2].

Value creation in the dimethylaminopropylamine market is changing due to a generational shift in downstream chemistry. Cocamidopropyl betaine and cocamidopropyl hydroxysultaine routes—amphoterics that have gentler skin profiles, lower aquatic toxicity, and compatibility with cold-process manufacturing—are gradually replacing legacy quaternary ammonium compounds produced from fatty-acid feedstocks. Since 2023, China and India have committed over USD 1.2 billion in capacity to parallel investment in low-VOC epoxy curing systems, where DMAPA is used as a building block for amidoamine hardeners [3][4].

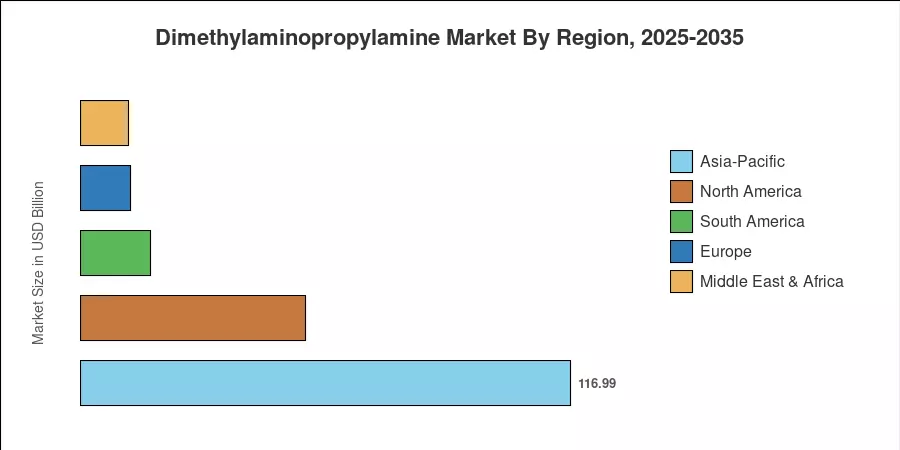

With integrated amine complexes in Nanjing, Zhejiang, and Gujarat, the Asia-Pacific accounts for about 45.7% of the world's volume. With a predicted 5.40% CAGR through 2035, the area is also the one with the fastest growth rate in the dimethylaminopropylamine market. Due to stringent EU Annex III nitrosamine limitations, pharmaceutical-grade and cosmetic-grade demand drives Europe's second-largest share, at about 22%. About 21% of the world's usage comes from North America, which is increasingly focused on flocculant uses for water treatment.

Key Report Takeaways

• By Grade

- Industrial grade accounted for approximately 64.5% of the Dimethylaminopropylamine Market volume in 2025, reflecting its dominance across water-treatment and epoxy-curing end uses.

- Cosmetic and low-amine specialty grades are forecast to expand at a 5.25% CAGR through 2035, driven by reformulation mandates in personal care.

• By Application

- Beauty and personal care surfactants led with a 5.38% projected CAGR, the fastest application segment in the Dimethylaminopropylamine Market.

- Water and wastewater treatment chemicals captured roughly 28% of volume in 2025, underpinned by municipal infrastructure spending.

• By End-Use Industry

- Personal care and cosmetics represented the largest end-use vertical at approximately 47.2% share in 2025.

- Construction and coatings are accelerating on the strength of low-emission epoxy formulations.

• By Region

- Asia-Pacific captured 45.7% of the 2025 market volume in the Dimethylaminopropylamine Market.

- South America posted the second-highest forecast CAGR among developing regions, driven by Brazilian agrochemical demand.

Dimethylaminopropylamine Market Size and Forecast (2021–2035)

Market Research Future derives historical volume from trade-flow databases (UN Comtrade, ITC Trade Map), production capacity audits at major amine complexes, and proprietary downstream consumption models calibrated against quarterly price indices. Forecast projections apply bottom-up demand modeling across application segments, validated against top-down macroeconomic indicators [5][6].