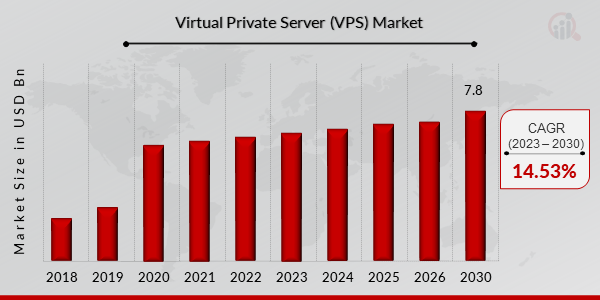

What is the current valuation of the Virtual Private Server Market?

The overall market valuation was 3.9 USD Million in 2024.

What is the projected market size for the Virtual Private Server Market by 2035?

The projected valuation for 2035 is 17.06 USD Million.

What is the expected CAGR for the Virtual Private Server Market during the forecast period?

The expected CAGR for the Virtual Private Server Market from 2025 to 2035 is 14.52%.

Which companies are considered key players in the Virtual Private Server Market?

Key players include Amazon Web Services, Microsoft Azure, Google Cloud, DigitalOcean, and others.

How does the Virtual Private Server Market segment by application?

The market segments by application include Web Hosting, Game Hosting, Application Development, Data Backup, and Virtual Desktop.

What are the projected revenues for Web Hosting in the Virtual Private Server Market?

Web Hosting is projected to grow from 1.56 USD Million in 2024 to 6.88 USD Million by 2035.

What is the revenue outlook for large enterprises in the Virtual Private Server Market?

Large enterprises are expected to see revenues increase from 1.56 USD Million in 2024 to 6.93 USD Million by 2035.

How is the Virtual Private Server Market expected to evolve in terms of deployment type?

The market is expected to grow across deployment types, with Public Cloud projected to rise from 1.56 USD Million to 6.93 USD Million by 2035.

What pricing models are prevalent in the Virtual Private Server Market?

The prevalent pricing models include Pay-as-you-go, Subscription-based, and One-time Payment.

What is the revenue forecast for the Subscription-based pricing model?

The Subscription-based model is projected to grow from 1.95 USD Million in 2024 to 8.67 USD Million by 2035.