Wound Debridement Products Size

Market Size Snapshot

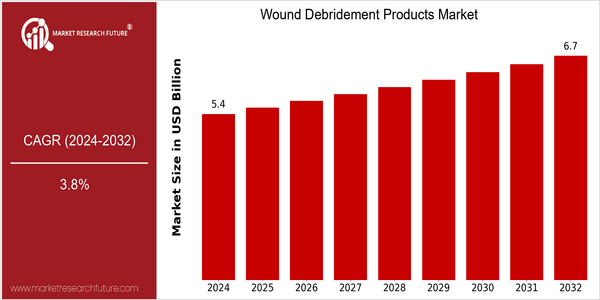

| Year | Value |

|---|---|

| 2024 | USD 5.4 Billion |

| 2032 | USD 6.7 Billion |

| CAGR (2024-2032) | 3.8 % |

Note – Market size depicts the revenue generated over the financial year

The wound-cleaning products market is set to grow at a steady pace, with a market size of $5.4 billion in 2024, which is projected to reach $6.7 billion by 2032, at a CAGR of 3.8%. The steady growth of the wound-cleaning products market is driven by the growing number of chronic wounds, such as diabetic ulcers and pressure ulcers, and the growing elderly population, which is susceptible to these diseases. The technological development of wound-cleaning products, such as the development of bioactive dressings and new debridement devices that increase the healing efficiency, is also driving the market. Rising health care expenditure and the increasing focus on patient-centric care are encouraging health care professionals to adopt more effective wound-management solutions. Strategic initiatives undertaken by market players, such as Smith & Nephew, Mölnlycke Health Care, and ConvaTec, to expand their product portfolios and strengthen their market positions, are driving the market. Moreover, the integration of digital health and wound care is expected to drive the market.

Regional Market Size

Regional Deep Dive

The market for wound-care products is characterized by growing demand across different regions, which is mainly driven by an increase in chronic wounds, surgical procedures, and an aging population. The market dynamics in the different regions are influenced by the different healthcare systems, the regulatory environment, and the cultural attitudes towards wound care. Moreover, the market is expected to evolve with advancements in technology and new product offerings, which will improve patient outcomes and drive market growth.

Europe

- In Europe the market is influenced by the growing number of diabetics and their associated complications, which increases the demand for wound-healing solutions. Also, associations such as the European Wound Management Association (EWMA) are actively promoting best practice and innovations in wound care, which influences the market.

- The European Union's Medical Devices Regulation has introduced stricter requirements for compliance and manufacturers have been prompted to invest in quality improvements and new product development. This regulatory change is expected to improve the safety and efficacy of wound debridement products, which will in turn enhance confidence in the products.

Asia Pacific

- In the Asia-Pacific region, the wound-cleaning market is growing rapidly, driven by a growing healthcare budget and an increased awareness of advanced wound-care solutions. Japan and Australia are at the forefront, with high investments in medical technology and in medical technology.

- This is a region where telemedicine and digital health are gaining ground. Companies such as Acelity and Coloplast are utilizing these new opportunities to improve patient outcomes and expand their presence in the market.

Latin America

- The progressive spread of advanced wound-cleaning products in Latin America is being driven by the growing burden of chronic diseases and the aging population. The region’s health-care systems are gradually shifting towards more modern wound-cleaning practices, which are influenced by international standards.

- Local manufacturers are beginning to invest in R&D to create cost-effective solutions tailored to the specific needs of the region. This trend will inevitably increase the availability of wound debridement products and improve the quality of care.

North America

- The North American market is experiencing a number of technological developments in the field of wound debridement, particularly with the introduction of bioengineered products and wound dressings that promote rapid healing. The companies Smith & Nephew and Medtronic are leading the way with their innovations that are aimed at meeting the increasing demand for effective wound management.

- A new trend in the market is the new regulation of wound care products by the Food and Drug Administration. It is expected that the availability of products for debridement will be increased, which will eventually benefit both the health care provider and the patient.

Middle East And Africa

- In the Middle East and Africa the wound-care market is developing. The development is due to the growing interest in the improvement of the health services and the increasing number of chronic wounds. Government initiatives to improve access to care are driving demand for advanced wound-care products.

- There is a growing interest on the part of international companies in the region’s prospects for growth and the opportunities for investment. Local associations and collaborations are increasingly common, which should enhance product availability and the innovation potential for wound care solutions.

Did You Know?

“Did you know that chronic wounds affect approximately 1-2% of the global population, with the incidence expected to rise due to the aging demographic and increasing prevalence of diabetes?” — World Health Organization (WHO)

Segmental Market Size

Among the most important categories of wound care products is the category of wound debridement products. The market for these products is currently growing at a steady rate, due to the increasing awareness of wound management procedures. The main reasons for this growth are the increasing number of chronic wounds, such as diabetic ulcers and pressure sores, and the aging population, which requires effective wound care solutions. Also, the regulatory framework is increasingly encouraging the use of advanced wound care products. The market for wound debridement products is currently in a mature phase, with companies such as Smith & Nephew and Mölnlycke offering the most advanced products. These products are used primarily for surgical debridement in hospitals and in outpatient care, and are used in the form of hydrogels and enzymatic debriders. However, trends such as the focus on patient-centred care and the emphasis on a sustainable approach to health care are accelerating the growth of the market, while technological developments such as negative pressure wound therapy and bioengineered skin substitutes are shaping the evolution of the market.

Future Outlook

From 2024 to 2032, the market for wound debridement products is expected to grow steadily, with a projected rise from $5.4 billion to $6.7 billion, at a CAGR of 3.8%. The growth is based on the increased occurrence of chronic wounds, such as diabetic ulcers and pressure sores, caused by the aging of the population and the rise in diabetes and obesity. With the growing emphasis in health care on wound management, the demand for effective debridement solutions is expected to increase significantly, which will lead to a higher market penetration and a higher rate of use among health care workers and patients. Further market growth is expected to be driven by technological advances, such as the development of new debridement devices and biologically active wound dressings. The integration of smart technology, such as wound monitoring systems and telehealth solutions, will improve the treatment outcomes and the use of debridement products, thus increasing the penetration of the market. Also, government regulations and reimbursement systems that support wound management will create a favorable environment for market growth. Also, the trend towards minimally invasive procedures and the growing emphasis on individualized medicine will further shape the market for wound debridement products and ensure that it will continue to be an evolving and dynamic sector of the health care industry.

Leave a Comment