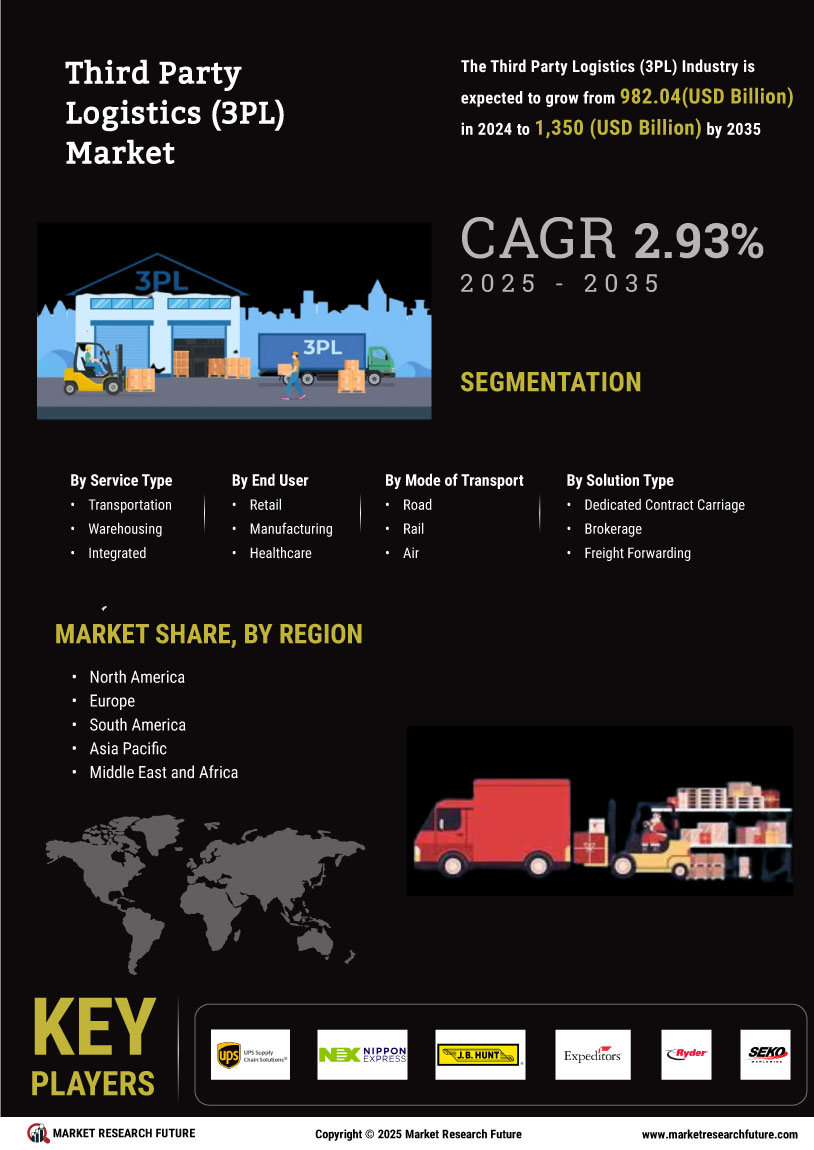

Focus on Cost Efficiency

Cost efficiency remains a pivotal driver in the Third Party Logistics 3PL Market Industry, as businesses seek to minimize expenses while maximizing service quality. By outsourcing logistics functions to 3PL providers, companies can leverage economies of scale and specialized expertise, resulting in significant cost savings. In 2025, it is projected that businesses utilizing 3PL services will experience a reduction in logistics costs by approximately 15% compared to in-house operations. This financial incentive encourages more companies to partner with 3PL providers, thereby fostering growth within the industry. The emphasis on cost efficiency is likely to persist as businesses navigate competitive pressures.

Increased Global Trade Activities

The Third Party Logistics 3PL Market Industry is significantly influenced by the rise in global trade activities. As international trade continues to expand, businesses are increasingly reliant on 3PL providers to navigate complex logistics challenges associated with cross-border transactions. In 2025, global trade is expected to grow by approximately 5%, further amplifying the demand for efficient logistics solutions. 3PL providers play a crucial role in facilitating customs clearance, transportation, and warehousing, which are essential for successful international operations. This growing interdependence between global trade and logistics services is likely to drive the expansion of the 3PL market.

Emphasis on Sustainability Practices

Sustainability practices are becoming increasingly important within the Third Party Logistics 3PL Market Industry, as companies strive to reduce their environmental impact. Many 3PL providers are adopting green logistics strategies, such as optimizing transportation routes and utilizing eco-friendly packaging materials. In 2025, it is anticipated that around 40% of 3PL companies will implement sustainability initiatives as part of their operational framework. This shift not only aligns with consumer preferences for environmentally responsible practices but also enhances the competitive edge of 3PL providers. The focus on sustainability is likely to shape the future of logistics, driving innovation and attracting environmentally conscious clients.

Technological Advancements in Logistics

Technological advancements are reshaping the Third Party Logistics 3PL Market Industry, as companies increasingly adopt innovative solutions to enhance operational efficiency. The integration of technologies such as artificial intelligence, machine learning, and the Internet of Things (IoT) is streamlining logistics processes. For instance, AI-driven analytics can optimize route planning and inventory management, leading to reduced operational costs. In 2025, it is estimated that over 60% of 3PL providers have implemented some form of advanced technology in their operations. This trend not only improves service delivery but also enhances customer satisfaction, making technology a critical driver in the evolving logistics landscape.

Rising Demand for E-commerce Fulfillment

The Third Party Logistics 3PL Market Industry is experiencing a notable surge in demand driven by the rapid expansion of e-commerce. As online shopping continues to gain traction, businesses are increasingly relying on 3PL providers to manage their logistics and supply chain operations. In 2025, the e-commerce sector accounted for approximately 20% of total retail sales, a figure that is projected to rise further. This trend compels retailers to seek efficient logistics solutions, thereby enhancing the role of 3PL providers in ensuring timely deliveries and inventory management. The ability of 3PL companies to offer scalable solutions tailored to the fluctuating demands of e-commerce is likely to solidify their position in the market.