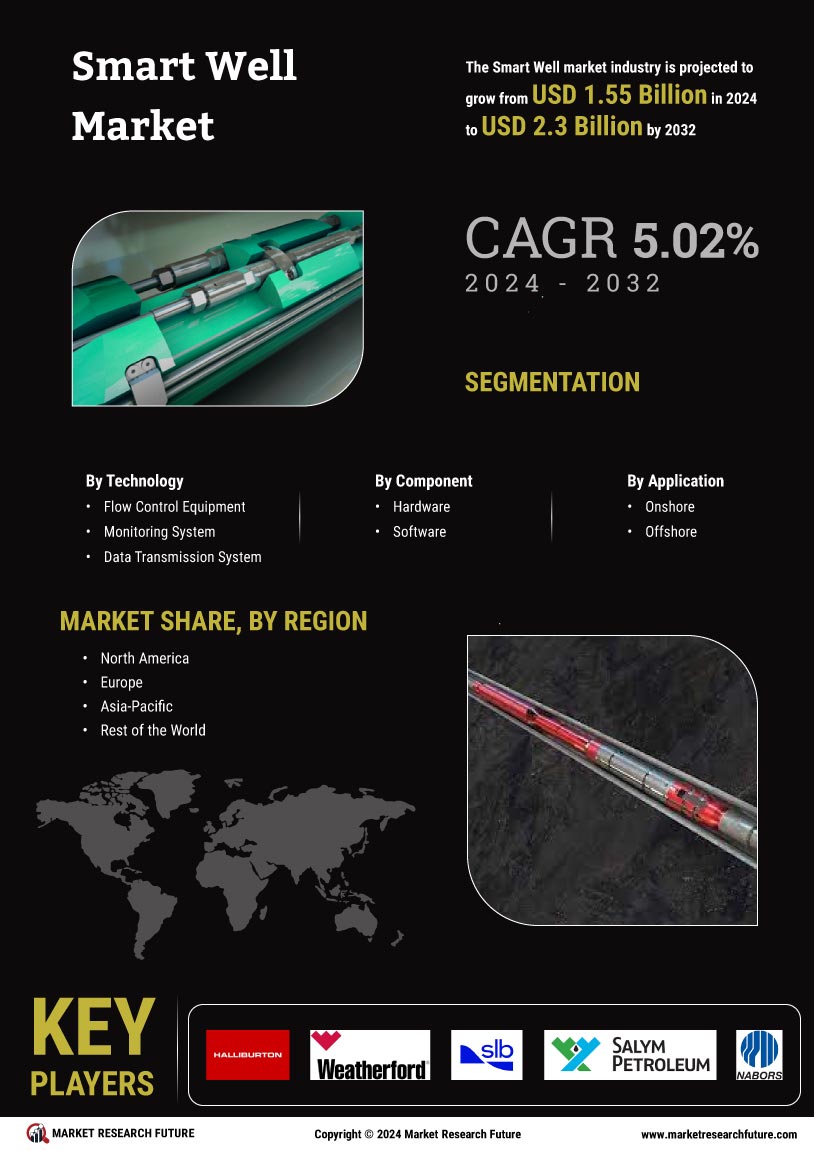

Smart Well Market Segmentation

Smart Well Market By Smart Well Market (USD Billion, 2025-2035)

- Flow Control Equipment

- Monitoring System

- Data Transmission System

Smart Well Market By Component (USD Billion, 2025-2035)

- Hardware

- Software

Smart Well Market By Application (USD Billion, 2025-2035)

- Onshore

- Offshore