Personal Cloud Size

Market Size Snapshot

| Year | Value |

|---|---|

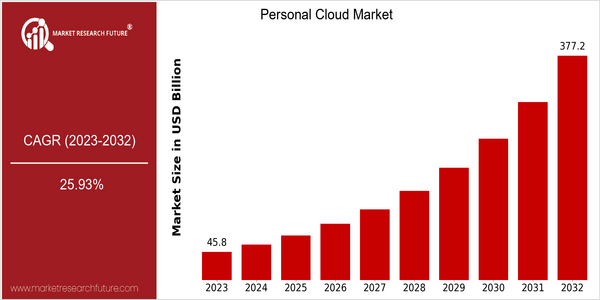

| 2023 | USD 45.81 Billion |

| 2032 | USD 377.17 Billion |

| CAGR (2024-2032) | 25.93 % |

Note – Market size depicts the revenue generated over the financial year

Personal Cloud Market - Expected to Grow at a Fast Pace, Worth $ 45.81 Billion in 2023, and Worth $ 377.17 Billion by 2032. Its CAGR from 2024 to 2032 is expected to be 25.93%. The main factors driving the market are the increasing importance of digital storage and the wide use of smart devices, and the demand for secure and convenient data management. Also, the rise of remote work and the need for remote collaboration tools will drive the market. Also, the technological advances, such as the improvement of encryption, the increase in speed, and the integration of artificial intelligence into cloud services, will drive the market. Also, the major players in the industry, such as Google, Microsoft and Dropbox, have been actively investing in research and development and strategic cooperation to enhance their market positions. Product launches that focus on easy-to-use UIs and increased storage capacity can attract more users, and thus further establish their positions in the market.

Regional Market Size

Regional Deep Dive

The Personal Cloud Market is experiencing significant growth in all regions. This growth is mainly due to the growing demand for data storage solutions, enhanced security features and the proliferation of smart devices. In North America, the market is characterized by high cloud adoption rates for both consumers and businesses, technological developments, and a high level of concern for data security. In Europe, the market is characterized by a diverse landscape, where the GDPR and other data protection regulations affect the trust of consumers and the dynamics of the market. In Asia-Pacific, the digital transformation is very strong, and the growing middle class and the increasing penetration of the Internet lead to a significant increase in the adoption of personal cloud services. The Middle East and Africa region is gradually embracing cloud technology, which is supported by government initiatives to digitalize. Latin America is also on the rise, with the focus on the provision of affordable cloud solutions for small and medium-sized businesses.

Europe

- The implementation of the General Data Protection Regulation (GDPR) has led to a heightened focus on data security and privacy, compelling cloud service providers to enhance their compliance measures.

- European companies such as OVHcloud are innovating by offering localized cloud solutions that prioritize data sovereignty, appealing to consumers concerned about data privacy.

Asia Pacific

- The rapid growth of the digital economy in countries like India and China is driving the demand for personal cloud services, with local players like Alibaba Cloud and Tencent Cloud expanding their offerings.

- Government initiatives promoting digital literacy and infrastructure development are facilitating the adoption of personal cloud solutions, particularly among small businesses and individual users.

Latin America

- The increasing smartphone penetration in Latin America is driving the demand for personal cloud services, with companies like UOL Diveo offering affordable solutions tailored to local consumers.

- Government programs aimed at boosting digital infrastructure are expected to enhance access to personal cloud services, particularly in rural areas.

North America

- The rise of remote work has significantly increased the demand for personal cloud solutions, with companies like Dropbox and Google Drive enhancing their offerings to cater to this trend.

- Regulatory changes, particularly around data privacy laws, have prompted organizations to invest in more secure personal cloud solutions, with companies like Microsoft leading the charge in compliance and security features.

Middle East And Africa

- Countries in the Middle East, such as the UAE, are investing heavily in smart city initiatives, which are expected to drive demand for personal cloud services as part of their digital transformation strategies.

- Local startups are emerging in the personal cloud space, with companies like Cloud4C providing tailored solutions to meet the unique needs of businesses in the region.

Did You Know?

“As of 2023, over 60% of consumers in North America are using at least one personal cloud service for data storage and sharing, reflecting a significant shift towards digital solutions.” — example.com

Segmental Market Size

Personal Clouds are an important part of the Cloud, and they are now enjoying a steady growth, due to the increasing demand for privacy and control over their own data. The need for remote access to personal files, especially in the post-pandemic world, is growing. The new regulations such as the General Data Protection Regulation (GDPR) also force individuals and companies to look for more secure solutions. Personal Cloud solutions are currently in the mass deployment stage, and companies like Synology and Western Digital are leading the way with their easy-to-use Personal Cloud appliances. The main applications are home media, file sharing and backup, with notable applications in the creative industries, where large files need to be accessed remotely. The trend to remote work and the green agenda are also driving the market, while the edge and the increased encryption will shape the evolution and ensure that Personal Clouds remain relevant and secure.

Future Outlook

Personal Cloud Market will grow from $46.8 billion in 2023 to $377.7 billion in 2032, at a CAGR of 25.93%. This growth will be driven by an increasing demand for data storage services, improved security, and the proliferation of smart devices. In the next few years, as more and more consumers and businesses recognize the importance of data ownership and control, the penetration of personal cloud solutions is expected to rise significantly, and it could exceed 60% of households by 2032. In addition, technological advancements, such as improved encryption, AI-driven data management, and IoT-enabled device integration, will further accelerate the development of the market. In addition, the increasing trend of remote work and digital collaboration will also drive the demand for reliable and accessible cloud storage solutions. Moreover, government regulations such as data protection laws and the growing awareness of cyber threats will also play an important role in promoting the development of the market. As the public awareness of data rights and the benefits of personal cloud services increases, the market will continue to develop, thereby promoting innovation and competition among service providers.

Leave a Comment