Dry Shampoo Market Summary

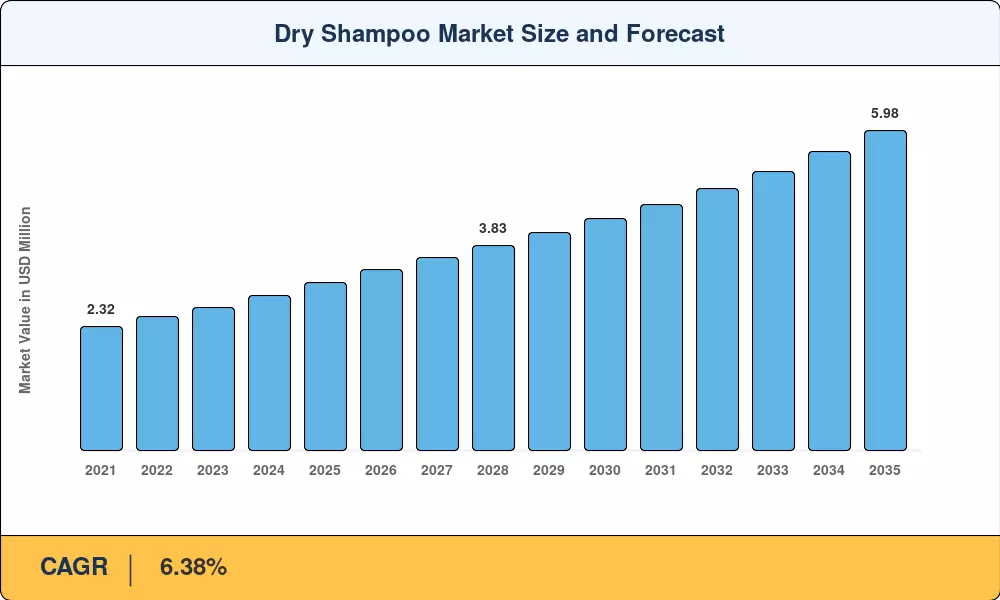

The Dry Shampoo Market was valued at USD 3.14 billion in 2025 and is projected to reach USD 3.38 billion in 2026 before climbing to USD 5.98 billion by 2035, registering a CAGR of 6.38% during the 2026–2035 forecast period. Two catalysts are reshaping baseline demand: tightening VOC emission limits under California's Consumer Products Program and the EU Cosmetics Regulation 1223/2009, both of which reward brands that invest in compliant, propellant-free formulations[2]. Consumers increasingly treat dry shampoo as a daily grooming essential rather than an emergency substitute, and retail shelf space for volumizing dry shampoo spray has expanded by double digits across mass-market channels in the past three years.

Product innovation is the defining force in the Dry Shampoo Market today. Legacy aerosol-only portfolios are giving way to hybrid lineups that include natural dry shampoo formula variants, rice-starch powders, and peptide-based odor-neutralizing actives developed through green biotechnology. The United States MoCRA legislation, which mandates ingredient transparency and adverse-event reporting, has raised the compliance bar — an estimated USD 120 million in incremental testing costs industry-wide — yet it is simultaneously weeding out counterfeit products and boosting consumer trust in official retail channels [3].

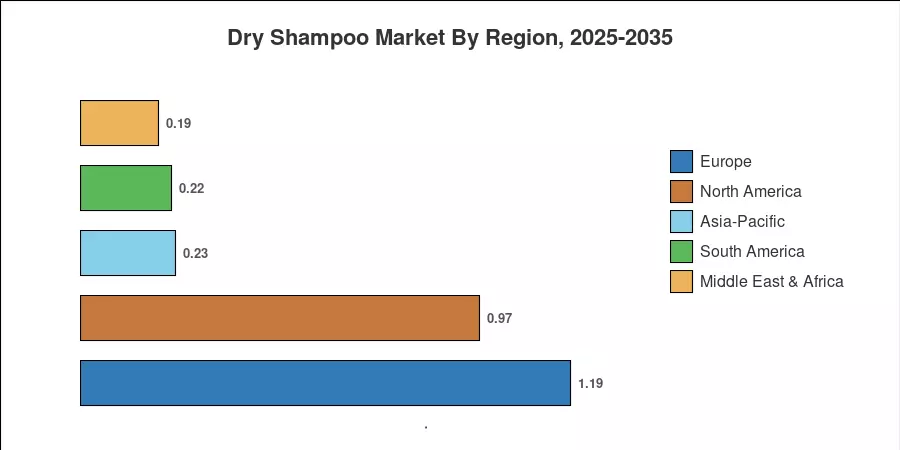

Europe leads the Dry Shampoo Market with roughly 37.8% of global revenue, driven by mature salon culture and strong private-label penetration across the Nordic countries. Asia-Pacific is the fastest-growing region at an anticipated 7.24% CAGR, fueled by urbanization in India and China and the rapid expansion of travel-size dry shampoo offerings tailored to on-the-go lifestyles. North America holds the second-largest share at approximately 31%, anchored by heavy DTC e-commerce spending and influencer-driven brand launches As scalp refreshing dry cleanser technology matures, the next decade will see the Dry Shampoo Market evolve from a convenience category into a full-fledged scalp-care platform.

Key Report Takeaways

• By Product Type

- Spray aerosols commanded roughly 69.9% of the Dry Shampoo Market in 2025, reflecting entrenched consumer preference for quick-application volumizing dry shampoo spray formats

- Powder variants are forecast to grow at a 7.17% CAGR through 2035, buoyed by demand for propellant-free and natural dry shampoo formula options

• By Nature

- Conventional formulations accounted for approximately USD 2.42 billion in 2025, underscoring the Dry Shampoo Market's reliance on cost-effective mass production

- Organic variants are projected to expand at a 7.48% CAGR as clean-beauty positioning and scalp refreshing dry cleanser ingredients gain traction

• By Region

- Europe generated the largest regional share of the Dry Shampoo Market in 2025 at 37.8%

- Asia-Pacific is anticipated to register a 7.24% CAGR, the highest among all regions, led by rising disposable incomes and growing awareness of dry shampoo for oily hair concerns

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue modeling from manufacturer shipments with top-down validation through trade-channel audits and customs data. Historical figures (2021–2024) reflect actuals; the base year 2025 blends preliminary actuals with model estimates. Forecast years (2026–2035) apply a calibrated CAGR adjusted for macroeconomic scenarios and regulatory pipelines.