Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

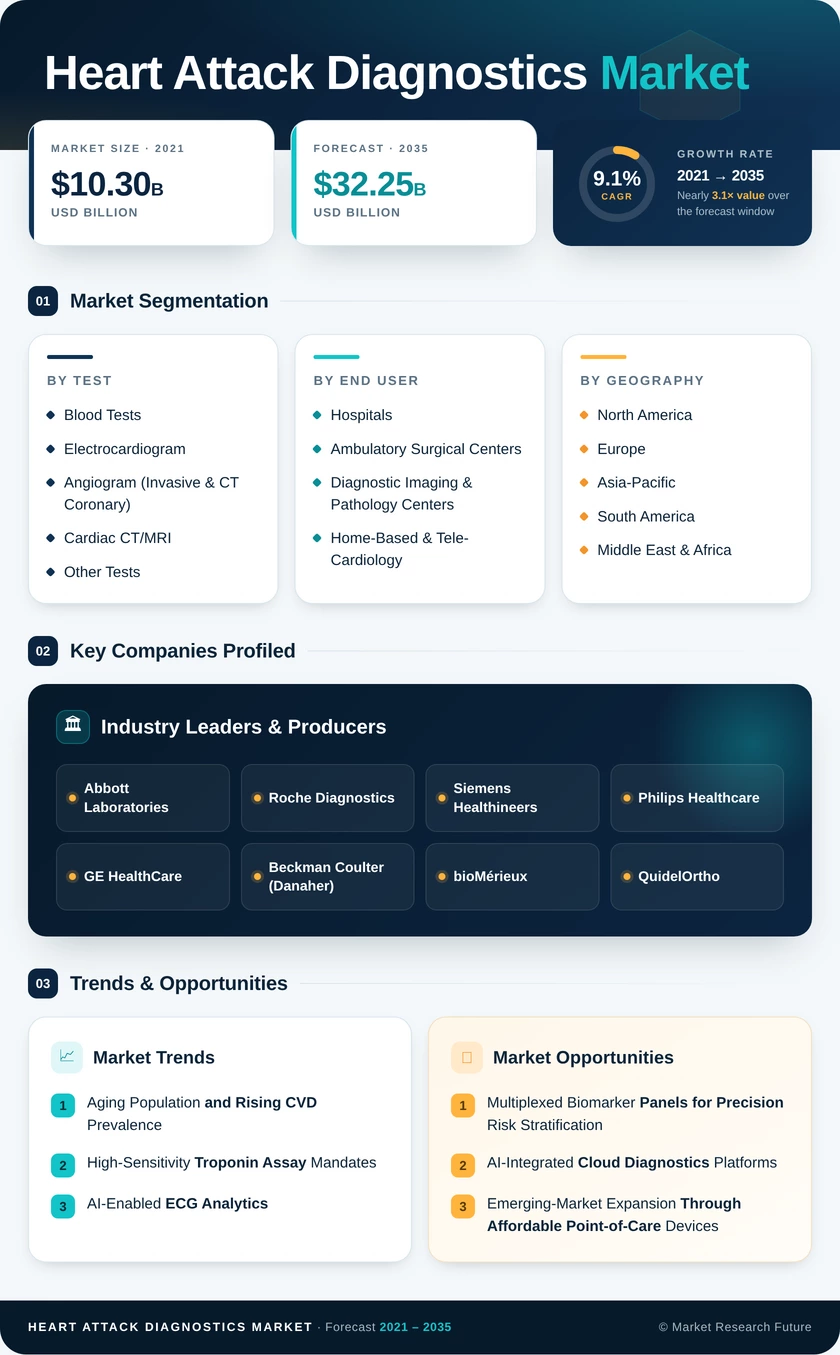

| By Test | Blood Tests; Electrocardiogram; Angiogram (Invasive & CT Coronary); Cardiac CT/MRI; Other Tests | Blood Tests | Electrocardiogram (AI/Wearable) |

| By End User | Hospitals; Ambulatory Surgical Centers; Diagnostic Imaging & Pathology Centers; Home-Based & Tele-Cardiology | Hospitals | Home-Based & Tele-Cardiology |

| By Geography | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Test

| Sub-Segment | Key Trend |

| Blood Tests | High-sensitivity troponin assays enabling one-hour MI rule-out protocols |

| Electrocardiogram | AI-augmented waveform analysis with cloud-based retraining loops |

| Angiogram (Invasive & CT Coronary) | Non-invasive CT coronary angiography replacing catheter-based procedures |

| Cardiac CT/MRI | Subclinical ischemia screening in asymptomatic high-risk populations |

| Other Tests | Emerging biomarkers (H-FABP, copeptin) are entering clinical validation |

Blood-based testing anchors the diagnostic pathway because every major guideline — from the ESC to the AHA — positions high-sensitivity troponin as the first-line biomarker for acute coronary syndrome evaluation. Electrocardiogram platforms are gaining ground rapidly as AI integration pushes sensitivity beyond 90% in prospective validation studies.

By End User

| Sub-Segment | Key Trend |

| Hospitals | High-throughput core-lab automation with sub-30-minute turnaround |

| Ambulatory Surgical Centers | Growth in outpatient stress-testing and elective cardiac procedures |

| Diagnostic Imaging & Pathology Centers | Increasing primary-care referrals for cardiac CT and biomarker panels |

| Home-Based & Tele-Cardiology | Remote-monitoring reimbursement driving wearable-device prescriptions |

Hospitals capture the majority of diagnostic spending due to their role as first-contact points for acute chest-pain presentations. Home-based and tele-cardiology settings represent the frontier of growth, driven by payer incentives that reward out-of-hospital monitoring and early intervention.