In recent developments within the Global Healthcare mobility solution market, companies such as Cerner, McKesson Corporation, and Epic Systems have been increasingly leveraging mobile technologies to enhance patient engagement and care delivery. In September 2023, Medtronic expanded its portfolio by acquiring a mobile health startup to strengthen its position in digital healthcare solutions. Similarly, Oracle's recent collaboration with GE Healthcare aims to integrate cloud services with healthcare analytics, providing more robust data solutions.

Current affairs highlight a significant uptick in investments directed towards telehealth services, driven by the ongoing demand for remote patient monitoring solutions post-pandemic. Companies like AT and T and Verizon Communications are focusing on 5G advancements to support the growing network requirement for mobile health applications. The market saw a notable growth valuation in 2022, driven by an increasing focus on personalized care through mobile applications and health devices.

Over the last two to three years, strategic partnerships and mergers have been pivotal in enhancing the technological capabilities of established players such as Siemens Healthineers and Philips Healthcare, emphasizing the dynamic shifts and competitive strategies within this sector.

Healthcare Mobility Solutions Market Drivers

Rapid Adoption of Mobile Health Applications

The Global Healthcare Mobility Solutions Market Industry is experiencing significant growth due to the rapid adoption of mobile health applications. According to the World Health Organization (WHO), mobile health usage has increased by over 50% in the past decade, reaching approximately 3 billion users globally. Major organizations such as the World Health Organization and national health services have been actively promoting mobile health solutions to enhance healthcare accessibility.

These applications not only facilitate patient engagement but also improve healthcare delivery efficiency. The integration of features such as telemedicine, appointment scheduling, and health monitoring is driving the adoption further, signifying a growing trend towards holistic mobile health solutions responsive to the dynamic healthcare landscape worldwide.

Increase in Government Initiatives for Healthcare Technology

Government initiatives aimed at enhancing healthcare through technology are significantly bolstering the Global Healthcare Mobility Solutions Market Industry. Many countries are introducing policies that encourage the integration of mobile solutions in healthcare. For instance, the U.S. Centers for Medicare and Medicaid Services reported an investment exceeding $1 billion in telehealth services during the COVID-19 pandemic, facilitating remote consultations and care.Such initiatives lay the groundwork for a more connected healthcare infrastructure, increasing the adoption of mobility solutions aimed at improving healthcare accessibility and patient outcomes globally.

Growing Prevalence of Chronic Diseases

The ever-increasing prevalence of chronic diseases globally is driving the expansion of the Global Healthcare Mobility Solutions Market Industry. The World Health Organization estimates that chronic diseases contribute to approximately 60% of global deaths annually, highlighting a pressing healthcare challenge.

Established organizations like the American Heart Association are actively addressing these concerns by advocating for mobile solutions that support chronic disease management.Mobile healthcare solutions play a pivotal role in monitoring and managing health conditions such as diabetes, hypertension, and cardiovascular diseases, thereby fostering improved health outcomes and reducing healthcare costs associated with chronic diseases.

Technological Advancements in Mobile Health Solutions

Technological advancements are a key driver of growth in the Global Healthcare Mobility Solutions Market Industry. Innovations in mobile device capabilities, such as improved connectivity, application performance, and data analytics tools, have made it easier to implement effective mobile health solutions. For example, advancements in artificial intelligence are enabling predictive analytics in healthcare, which allows providers to anticipate patient needs and optimize care delivery.

Organizations like the International Telecommunication Union report substantial increases in mobile broadband subscriptions, facilitating more effective communication between patients and healthcare providers. This continuous evolution of technology ensures that the industry remains dynamic, scalable, and capable of meeting the diverse needs of the evolving global healthcare landscape.

Healthcare Mobility Solutions Market Segment Insights:

Healthcare Mobility Solutions Market Device Type Insights

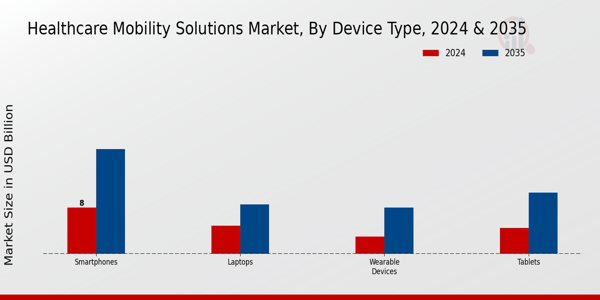

The Global Healthcare Mobility Solutions Market under the device type segment is notably varied and encompasses essential technologies that empower healthcare delivery and patient engagement. As of 2024, the overall market is expected to hold a valuation of 20.37 USD Billion, with specific device types contributing significantly to this figure. The Smartphones segment leads the way with a projected value of 8.0 USD Billion in 2024, showcasing its dominance as a vital tool in healthcare mobility due to their widespread usage and accessibility.

Their capabilities for telemedicine, real-time health monitoring, and access to medical information have positioned smartphones as a majority holding within the market.Following this, Tablets are projected to be valued at 4.5 USD Billion in the same year, serving as crucial devices in clinical settings for accessing patient records, educational resources, and telehealth applications. This segment's importance lies in its portability and ease of use in various healthcare environments. Wearable Devices are anticipated to generate a valuation of 3.0 USD Billion in 2024.

This segment significantly impacts health tracking and monitoring, providing patients and providers with actionable insights into health metrics such as heart rate and physical activity levels, thus driving patient engagement and promoting proactive health management.Laptops round out the device segment with an expected value of 4.87 USD Billion in 2024, utilized extensively for tasks requiring more robust computing power such as data analysis, electronic health record management, and various healthcare applications.

The collectively rising figures point to a broader trend towards digital transformation in healthcare, where mobility solutions are increasingly becoming integral to improving patient outcomes, enhancing operational efficiency, and enabling remote care capabilities. Each device type plays a unique role, reflecting technological advancements and changing consumer preferences in the healthcare landscape, driving the growth trajectory of the Global Healthcare Mobility Solutions Market for years to come.

Source: Primary Research, Secondary Research, MRFR Database and Analyst Review

Healthcare Mobility Solutions Market Application Insights

In the Global Healthcare Mobility Solutions Market, among the various Applications, Remote Patient Monitoring stands out as a crucial tool for managing chronic diseases, enabling healthcare providers to monitor patients’ health statuses in real-time, thereby improving the quality of care. Telemedicine has transformed the way patients access healthcare services, particularly in underserved areas, facilitating increased patient engagement and access to specialized care through digital platforms.

Healthcare Workflow Management optimizes clinical processes and administrative tasks, leading to enhanced operational efficiency within healthcare facilities. Medication Management systems are also vital, ensuring the accuracy and safety of medication administration, which is crucial for patient outcomes.

As these Applications evolve, they tackle challenges such as high healthcare costs and access disparities, paving the way for innovative solutions that enhance patient care and operational efficiencies in the Global Healthcare Mobility Solutions Market.Major stakeholders recognize the potential for market growth driven by these applications as they meet the increasing demand for flexible, efficient, and patient-centered healthcare solutions.

Healthcare Mobility Solutions Market End-Use Insights

The Global Healthcare Mobility Solutions Market is poised for significant growth,Within this segment, hospitals play a crucial role in utilizing mobility solutions to enhance patient care and streamline operations. Home care services are witnessing a surge, driven by the growing population of elderly individuals preferring in-home healthcare.

Healthcare providers are adopting mobility solutions to improve patient engagement and data management, significantly transforming traditional healthcare delivery methods.Pharmacies also contribute to the market by integrating mobile technology for inventory management and patient communication. Together, these sectors highlight the importance of mobility solutions in facilitating improved healthcare delivery, ultimately driving the Global Healthcare Mobility Solutions Market revenue. The increasing focus on enhancing patient outcomes, managing chronic diseases, and ensuring efficient medication management supports the growth and innovation across these diverse end-use applications.

As healthcare organizations worldwide adapt to new technologies, the market's dynamics reflect not only changes in healthcare practices but also the opportunities for ongoing improvement and efficiency.

Healthcare Mobility Solutions Market Technology Insights

This market's growth is primarily driven by the increasing demand for efficient healthcare services and enhanced patient engagement. Among the major contributors, Cloud Computing facilitates real-time data access and efficient health information management, significantly improving operational efficiencies for healthcare providers.Mobile Applications have revolutionized patient interaction, offering tools for everything from appointment scheduling to medication reminders, thus driving substantial adoption and user engagement. Wireless Communication acts as a backbone for seamless data transmission in healthcare settings, ensuring that critical information is shared promptly among healthcare professionals.

The Internet of Things enhances monitoring capabilities by connecting devices that collect real-time health data, subsequently optimizing patient care. As such, these technologies not only contribute to improved healthcare outcomes but also strengthen the overall framework of the Global Healthcare Mobility Solutions Market, aligning with trends towards digital health transformation and the growing emphasis on preventative care.

Healthcare Mobility Solutions Market Regional Insights

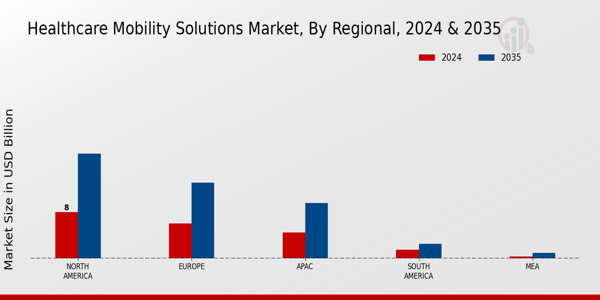

The Global Healthcare Mobility Solutions Market is experiencing substantial growth across its regional segments, contributing significantly to the overall market landscape. By 2024, North America is projected to dominate this market with a valuation of 8.0 USD Billion, expected to expand to 18.0 USD Billion by 2035, driven largely by advanced healthcare infrastructure and increased demand for digital health solutions.

Europe follows closely, with a market valuation of 6.0 USD Billion in 2024, growing to 13.0 USD Billion by 2035, influenced by strong government support for healthcare digitization.The Asia-Pacific (APAC) region, recognized for its rapid technological adoption, is valued at 4.5 USD Billion in 2024 and is expected to reach 9.5 USD Billion by 2035, indicating a growing trend towards healthcare innovation in this region.

South America, while smaller, has a market value of 1.5 USD Billion in 2024, expected to reach 2.5 USD Billion by 2035, highlighting a gradual but noticeable shift towards mobile healthcare solutions. The Middle East and Africa (MEA) region, although the least valued at 0.37 USD Billion in 2024, projected to grow to 1.0 USD Billion in 2035, signifies a budding interest in healthcare mobility solutions stemming from rising healthcare challenges and the necessity for effective healthcare delivery models.

Source: Primary Research, Secondary Research, Market Research Future Database and Analyst Review

Leave a Comment