Market Summary

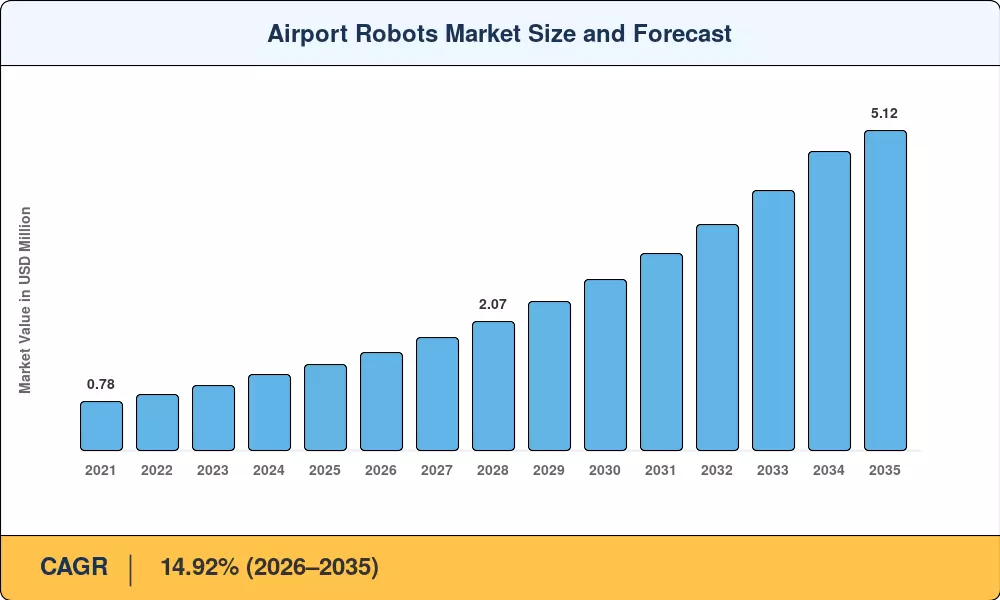

The Airport Robots Market reached an estimated USD 1.38 billion in 2025 and is projected to grow from USD 1.57 billion in 2026 to USD 5.12 billion by 2035, registering a CAGR of 14.92% during the forecast period. Post-pandemic passenger volume recovery — global air traffic exceeded 4.4 billion passengers in 2024 according to IATA [2] — has collided with persistent labor shortages across ground handling and terminal operations, creating a structural pull toward robotic automation. Airport operators worldwide are channeling capital expenditure toward autonomous airport service robots as a way to absorb capacity growth without expanding physical footprints.

There is a technology inflection happening. AI-driven robotic platforms using LiDAR, computer vision, and natural language processing are replacing legacy manual tasks such as luggage handling, terminal cleaning and perimeter security. In 2024, Singapore’s Changi Airport Group invested more than USD 65 million for a phased implementation of baggage handling robot systems and autonomous cleaning units in Terminals 1-4 [3]. These deployments prove that airport cleaning automation robot systems and passenger assistance airport robot kiosks may reduce turnaround times by 20-30% while decreasing operational personnel needs.

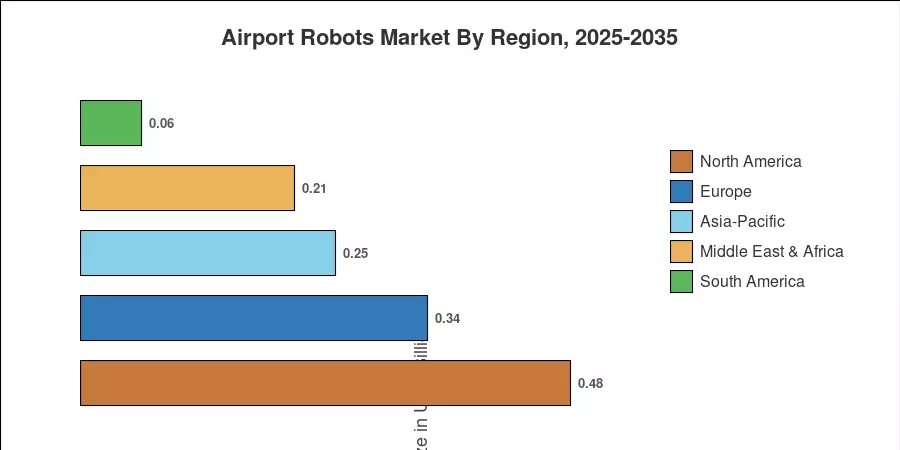

North America is the leader in the Airport Robots Market with around 34.5% of the global market share due to TSA security measures and federal innovation grants [4]. The Asia-Pacific area is the fastest expanding with a predicted CAGR of 18.2% due to active smart-airport plans in China, Japan and South Korea Europe follows in second place, with EU-funded digitization efforts under Horizon Europe anchoring the position. In the coming decade, AI robot security patrol solutions and autonomous logistics platforms will redefine airport operations from curb to gate.

Key Report Takeaways

• By Application

- Terminal operations captured approximately 73% of the Airport Robots Market revenue in 2025, reflecting strong demand for information kiosks, autonomous airport service robots, and cleaning units deployed in passenger-facing zones

- Landside solutions — including autonomous valet parking and curbside logistics — are forecast to expand at a 15.6% CAGR through 2035 as sensor technology matures and regulatory pilots scale

• By Robot Type

- Non-humanoid platforms held a dominant share of the Airport Robots Market in 2025, valued at approximately USD 1.04 billion, owing to their lower unit cost and faster deployment timelines

- Humanoid units are projected to grow at a 16.8% CAGR through 2035, driven by multilingual passenger assistance airport robot use cases in high-traffic terminals

• By End Use

- Security systems led the Airport Robots Market with roughly 34.2% share in 2025, powered by AI robot security patrol adoption at major hub airports

- Cleaning and disinfection robots are advancing at a 17.4% CAGR, the fastest among all end-use segments, reflecting sustained post-COVID hygiene investment

• By Geography

- North America accounted for approximately USD 0.48 billion of Airport Robots Market revenue in 2025, led by the United States

- Asia-Pacific is set to post the fastest expansion at an 18.2% CAGR through 2035, with China and Japan as primary growth engines

Airport Robots Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines primary interviews with airport operators, robotics OEMs, and system integrators alongside secondary data from IATA, ACI, national aviation authorities, and company financials. Historical figures (2021–2024) reflect actual deployments and procurement records; 2025 is the base year, and 2026–2035 values are modeled using a constant CAGR of 14.92%.