Infrared Detector Market Summary

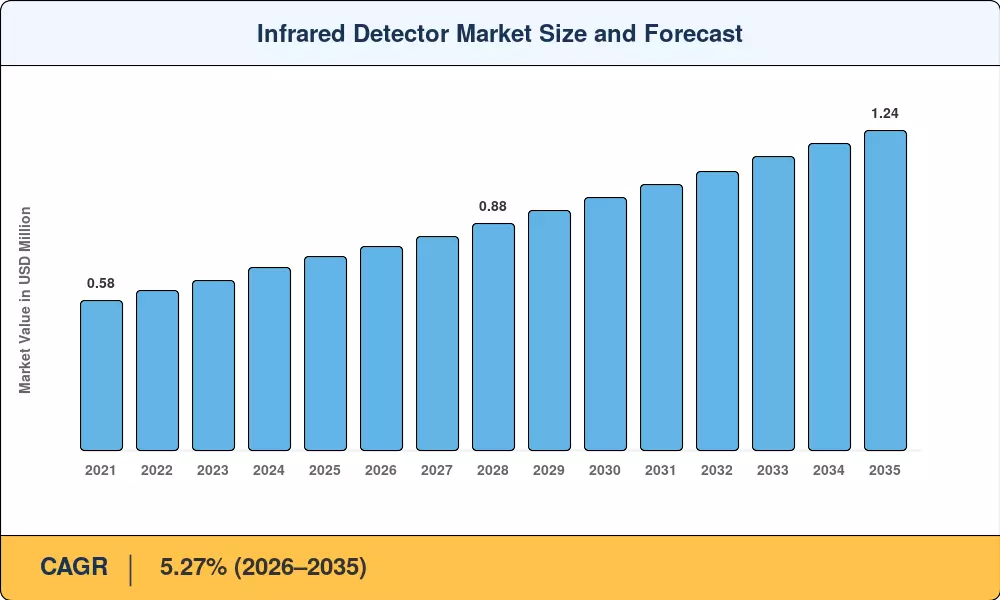

The Infrared Detector Market reached an estimated USD 0.75 billion in 2025 and is projected to grow from USD 0.79 billion in 2026 to USD 1.24 billion by 2035, registering a CAGR of 5.27% during the forecast period. Two catalysts are reshaping the spending landscape: the European Union's quarterly thermography audit mandates under its revised Energy Performance of Buildings Directive, and the rapid scale-up of solid-state LiDAR integration into electric vehicle platforms, where automakers committed over USD 2.8 billion in sensor procurement contracts during 2024 alone [2]. Together, these forces are pulling demand away from legacy pyroelectric modules and toward higher-performance IR thermal sensors and photodetector infrared arrays.

The Infrared Detector Market is undergoing a technical turnaround. Passive pyroelectric sensors were formerly the standard for motion detection and basic heat detection technologies, but are now being surpassed by wafer-level-packaged uncooled microbolometers that integrate vacuum encapsulation, anti-reflection coatings and readout circuitry into packages smaller than 10 mm per side. Meanwhile, photo quantum systems using indium-gallium-arsenide (InGaAs) and mercury-cadmium-telluride (MCT) substrates are finding favor in automotive ADAS and defense programs due to their higher frame rates and better noise performance [3]. U.S. Department of Defense requested USD 410 million for next-generation infrared imaging systems in its FY 2025 budget request [4].

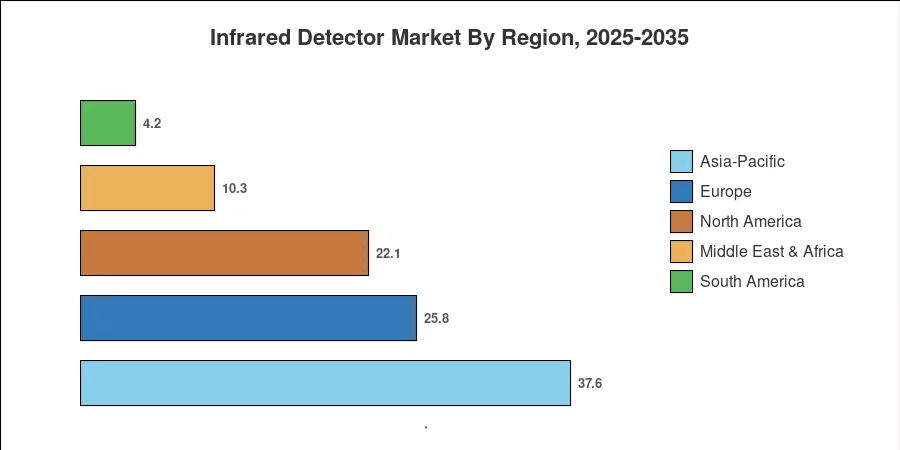

Asia-Pacific is the biggest Infrared Detector Market with a ~38% share of the worldwide market due to the vertically integrated LiDAR supply chain in China and the increasing production base of thermal camera sensors in South Korea. The Middle East & Africa is the fastest-growing geography, with a CAGR of 7.84% forecast for the region as green-hydrogen complexes shift from pilot facilities to megawatt-scale operations that require continuous hydrogen-leak monitoring with IR thermal sensors [5]. Regulatory mandates and industrial maintenance demand provide Europe with the second-largest share at around 26%. In the coming decade, infrared imaging systems will migrate from specialist defense applications to widespread automobile, smart-building and energy-infrastructure installations.

Key Report Takeaways

• By Detector Type

- Thermal detectors commanded 72.3% of the Infrared Detector Market revenue in 2025, with uncooled microbolometer films accounting for the bulk of that share

- Photo quantum detectors are forecast to expand at a 12.7% CAGR through 2035, fueled by automotive ADAS demand for InGaAs-based photodetector infrared arrays

• By End-Use

- Automotive ADAS and LiDAR applications are set to post a 19.8% CAGR, making them the highest-growth application segment through 2035

- Industrial manufacturing represented approximately USD 0.23 billion of 2025 demand, reflecting steady adoption of heat detection technology for predictive maintenance

• By Geography

- Asia-Pacific leads global volume with a 38% share, supported by China's dominance in LiDAR component manufacturing

- The Middle East & Africa region is growing at the fastest pace as hydrogen-leak monitoring installations accelerate across the Gulf Cooperation Council states

- North America accounts for roughly 22% of the Infrared Detector Market, with the U.S. defense sector serving as the primary demand engine

Infrared Detector Market Size and Forecast (2021–2035)

Market Research Future (MRFR) market size is based on a bottom-up revenue model of component producers, and a top-down validation of end-use industry procurement budgets. Historical values (2021-2024) are collected from company filings and trade association data. The 2025 base year is triangulated using import-export databases and channel surveys. Forecast values for 2026-2035 are based on a calibrated CAGR of regulatory pipelines, technology adoption curves and macroeconomic factors.