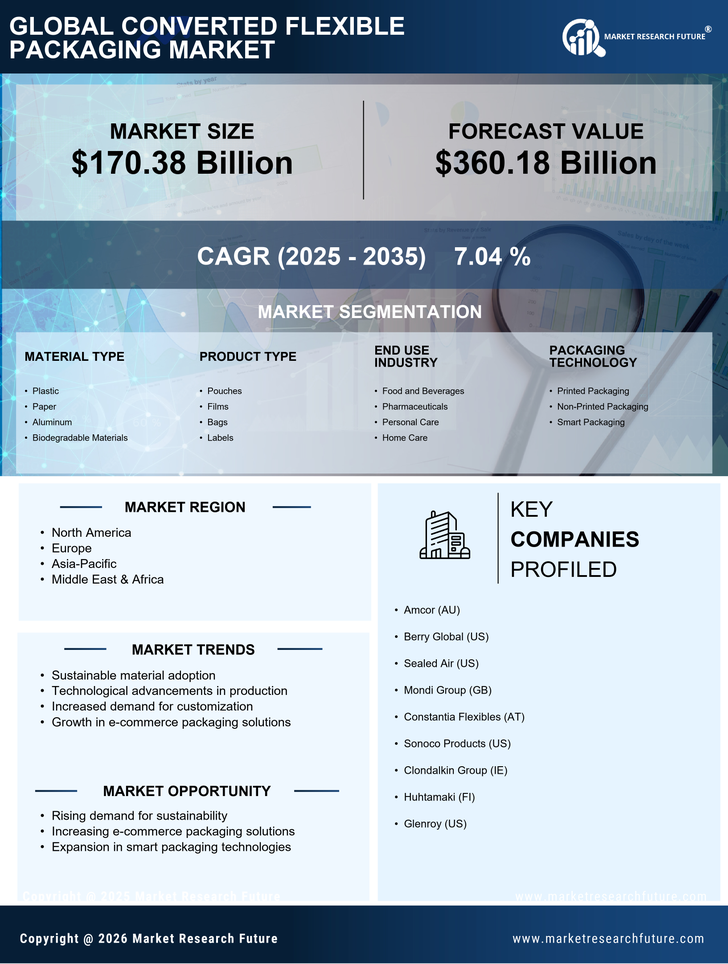

Converted Flexible Packaging Market Segmentation

Converted Flexible Packaging Market By Material Type (USD Billion, 2025-2035)

- Plastic

- Paper

- Aluminum

- Biodegradable Materials

Converted Flexible Packaging Market By Product Type (USD Billion, 2025-2035)

- Pouches

- Films

- Bags

- Labels

Converted Flexible Packaging Market By End Use Industry (USD Billion, 2025-2035)

- Food and Beverages

- Pharmaceuticals

- Personal Care

- Home Care

Converted Flexible Packaging Market By Packaging Technology (USD Billion, 2025-2035)

- Printed Packaging

- Non-Printed Packaging

- Smart Packaging