Automotive Sensor Market Summary

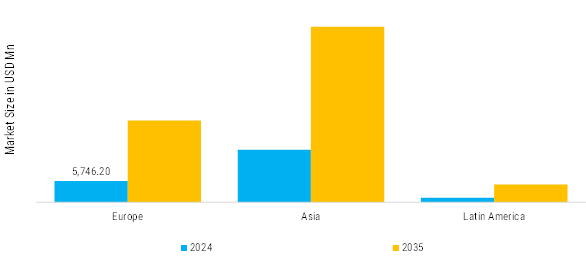

As per Market Research Future analysis, the Automotive Sensors Market Size was valued at USD 32,487.25 million in 2024. The Automotive Sensors Industry is projected to grow from USD 38,010.08 million in 2025 to USD 1,14,102.14 million by 2035, exhibiting a compound annual growth rate (CAGR) of 11.6% during the forecast period 2025 - 2035.

Key Market Trends & Highlights

The Automotive Sensors Market is undergoing rapid transformation in 2026, propelled by electrification, autonomy, and connectivity.

- AI-embedded sensors process data in real-time for predictive analytics and decision-making in ADAS systems.

- Multi-modal fusion combines radar, LiDAR, cameras, and ultrasonics for 360-degree perception in autonomous vehicles.

- IoT-enabled sensor networks enable V2V/V2I data sharing for traffic optimization and predictive maintenance.

- Eco-friendly sensors use recyclable materials and low-energy designs to meet emission regs. Trends shift to biodegradable housings and solar-powered units for telematics.

Market Size & Forecast

| 2024 Market Size | 32,487.25 (USD Million) |

| 2035 Market Size | 1,14,102.14 (USD Million) |

| CAGR (2025 - 2035) | 11.6% |

Major Players

Continental AG, Infineon Technologies AG, NXP Semiconductors N.V., Murata Manufacturing Co., Ltd., ZF Friedrichshafen AG, Valeo S.A., Onsemi, OmniVision Technologies, Inc., AMPRO Technologie GmbH, TE Connectivity, Denso Corporation, Panasonic Corporation, Sensata Technoliges, Analog Device.