Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

Market Size Snapshot

| Year | Value |

|---|---|

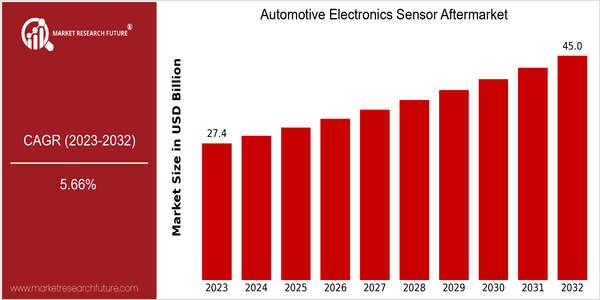

| 2023 | USD 27.42 Billion |

| 2032 | USD 45.0 Billion |

| CAGR (2024-2032) | 5.66 % |

Note – Market size depicts the revenue generated over the financial year

The aftermarket for automobile sensors is expected to grow significantly, from $27.4 billion in 2023 to $45 billion in 2032, at a CAGR of 5.66% from 2024 to 2032. The demand for sensors is expected to rise due to the increasing complexity of vehicle systems and the growing focus on safety, efficiency, and connectivity in modern cars. As vehicles become more technologically advanced, the need for high-performance sensors that can monitor a range of vehicle parameters becomes critical, driving the market growth. Moreover, the growing popularity of electric vehicles and the increasing use of advanced driver assistance systems (ADAS) will continue to fuel the growth of the market. LiDAR, radar, and camera systems are used in ADAS to improve vehicle safety and performance. The major players, such as Robert Bosch, Continental AG, and Denso Corporation, are constantly investing in research and development to enhance their product offerings. Strategic initiatives, such as collaborations and mergers and acquisitions, are further expected to strengthen the market in the coming years.

Regional Market Size

Regional Deep Dive

The aftmarket for automobile sensors is experiencing substantial growth in all regions of the world, driven by the increasing demand for advanced vehicle safety features, the rise of electric vehicles, and the growing trend of vehicle connectivity. In North America, the market is characterized by the strong presence of leading automobile manufacturers and a well-developed aftermarket service network. In Europe, on the other hand, regulatory initiatives are aimed at improving vehicle safety and reducing harmful emissions. The Asia-Pacific region, on the other hand, is booming and rapidly adopting new sensor technologies due to the flourishing automobile industry. In the Middle East and Africa, the market is growing slowly, mainly due to the lack of economic and transport development. The same is true for Latin America, which is characterized by the rapid growth of the vehicle fleet and the modernization of the automobile industry.

Europe

- Europe is at the forefront of adopting stringent emissions regulations, such as the Euro 6 standards, which are driving the demand for advanced sensors that monitor and control vehicle emissions.

- Key players like Bosch and Continental are innovating in the sensor space, focusing on developing smart sensors that can provide real-time data analytics, which is expected to enhance the aftermarket services.

Asia Pacific

- The Asia-Pacific region is witnessing rapid advancements in sensor technology, with countries like Japan and South Korea leading in the development of high-precision sensors for automotive applications.

- Government initiatives in China, such as the 'Made in China 2025' plan, are promoting the adoption of smart automotive technologies, which is likely to boost the demand for automotive electronics sensors in the aftermarket.

Latin America

- Latin America is experiencing a rise in vehicle ownership, particularly in Brazil and Mexico, which is leading to an increased demand for aftermarket automotive electronics sensors.

- The region is also seeing investments from global automotive suppliers, such as Valeo, which are establishing local production facilities to cater to the growing market needs.

North America

- The North American market is heavily influenced by the push for advanced driver-assistance systems (ADAS), with companies like Tesla and General Motors investing significantly in sensor technologies to enhance vehicle safety and automation.

- Recent regulatory changes, such as the National Highway Traffic Safety Administration's (NHTSA) guidelines on vehicle safety, are prompting manufacturers to integrate more sophisticated sensors, thereby expanding the aftermarket opportunities.

Middle East And Africa

- The Middle East and Africa are gradually increasing their focus on automotive safety, with countries like the UAE implementing new regulations that require advanced safety features in vehicles, thereby driving sensor demand.

- Local companies are beginning to collaborate with international firms to enhance their technological capabilities in automotive electronics, which is expected to foster growth in the aftermarket sector.

Did You Know?

“Did you know that the automotive sensor market is expected to see a significant shift towards wireless sensor technologies, which can reduce installation costs and improve vehicle performance?” — Market Research Future

Segmental Market Size

In the aftermarket of the sensors for automobiles, the role of safety, efficiency and performance is played by the smallest of sensors, the smallest of all. The aftermarket for such sensors is currently growing, driven by the increasing demand for advanced driver assistance systems (ADAS) and the increasing complexity of the car's electrical systems. The demand is also driven by the tightening of safety regulations and the rapid development of sensors that enable features such as collision avoidance and active cruise control. In the aftermarket, the uptake of sensors for automobiles is currently in the pilot phase, with companies such as Robert Bosch and Continental leading the way in providing new solutions. The most important applications are the sensors for collision avoidance, tire pressure monitoring and the environment for electric vehicles. There are also important trends that are driving the market forward, such as the drive for a sustainable environment and the increasing demand for safety on new cars. Lidar, radar and other sensors with improved vision are shaping the development of this market, which is aimed at equipping the car with the latest safety and performance features.

Future Outlook

The market for sensors in automobiles is expected to grow at a robust CAGR of 5.6% from 2023 to 2032. This growth will be fueled by the rising demand for advanced driver-assistance systems (ADAS) and the increasing integration of Internet of Things (IoT) technology into vehicles. The focus of both manufacturers and consumers is on safety and interactivity, and this is driving the market for sensors in the automotive industry. By 2032, it is estimated that more than 70% of new vehicles will be equipped with multiple sensors, including LiDAR, cameras, and radar, which will enhance both functionality and safety. The miniaturization of components and the development of more advanced sensors will also drive market growth. Government support for the promotion of electric vehicles and sustainable transportation solutions will further drive the market for sensors in automobiles. In the aftermarket, the shift toward autonomous driving and the growing importance of vehicle-to-everything (V2X) communication will also be important. As the industry evolves, it is critical that companies remain agile and responsive to these trends to be able to capitalize on the emerging opportunities in the aftermarket for sensors in automobiles.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Growth Rate | 6.9% (2023-2032 |

Automotive Electronics Sensor Aftermarket Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.