Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

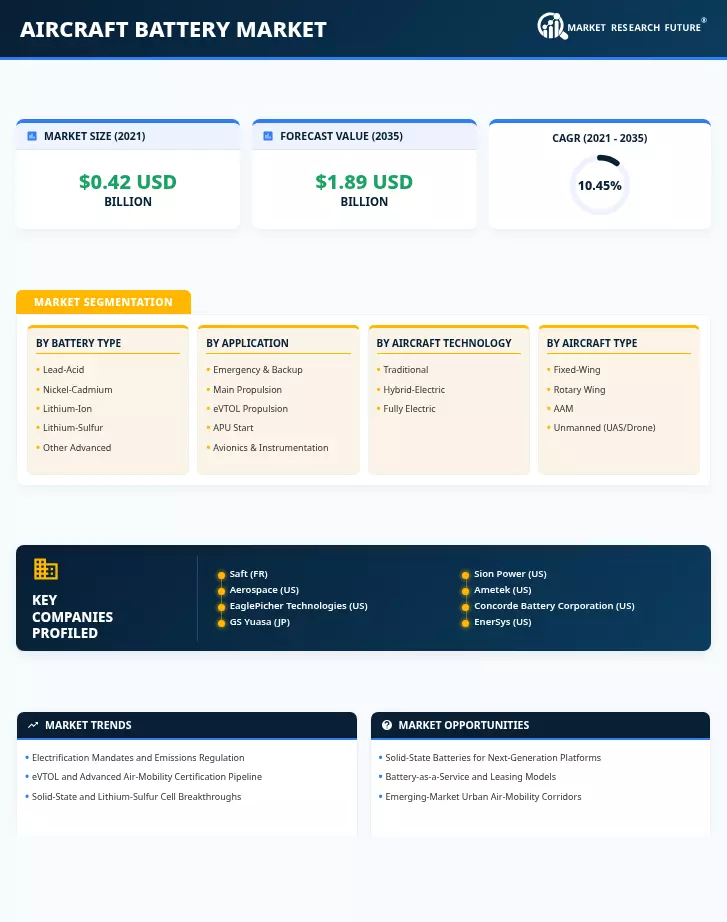

| Battery Type | Lead-Acid, Nickel-Cadmium, Lithium-Ion, Lithium-Sulfur, Other Advanced | Lithium-Ion (56.1% share, 2025) | Lithium-Sulfur (25.4% CAGR) |

| Application | Emergency & Backup, Main Propulsion, eVTOL Propulsion, APU Start, Avionics & Instrumentation | Emergency & Backup (40.8% share, 2025) | eVTOL Propulsion (31.2% CAGR) |

| Aircraft Battery Market | Traditional, Hybrid-Electric, Fully Electric | Traditional (~62% share, 2025) | Fully Electric (~32% CAGR) |

| Aircraft Type | Fixed-Wing, Rotary Wing, AAM, Unmanned (UAS/Drone) | Fixed-Wing (65.2% share, 2025) | AAM (31.5% CAGR) |

| Power Density | Below 300 Wh/kg, 300–500 Wh/kg, Above 500 Wh/kg | Below 300 Wh/kg (72.1% share, 2025) | Above 500 Wh/kg (29.1% CAGR) |

| End User | OEM, Aftermarket | OEM (65.4% share, 2025) | Aftermarket (8.2% CAGR) |

Market Segmentation Overview

By Battery Type

| Sub-Segment | Key Trend |

| Lead-Acid | Declining share as general-aviation operators transition to lithium-ion drop-in replacements. |

| Nickel-Cadmium (NiCd) | Legacy installed base in military rotary-wing; phase-outs accelerating under REACH regulation |

| Lithium-Ion (Li-ion) | Dominant chemistry with expanding TSO certifications for main-ship and emergency roles |

| Lithium-Sulfur (Li-S) | Rapid R&D with prototype packs now in eVTOL flight testing; cycle-life improvements critical |

| Other Advanced | Solid-state and lithium-air cells in laboratory-to-pilot transition; aviation certification post-2029 |

Lithium-ion remains the workhorse chemistry in aviation, benefiting from automotive-scale cost reductions and a growing portfolio of FAA/EASA-certified part numbers. Lithium-sulfur and solid-state alternatives are progressing rapidly through prototype flight testing, and their eventual certification will reshape competitive dynamics across the Aircraft Battery Market.

By Application

| Sub-Segment | Key Trend |

| Emergency & Backup Power | Mandatory on all certified aircraft; transitioning from NiCd to Li-ion chemistry |

| Main Propulsion | Growing as fully electric regional platforms approach certification |

| eVTOL Propulsion | Fastest-growing application driven by AAM corridor commercialization |

| APU Start | Narrowbody fleet modernization is creating steady replacement demand. |

| Avionics & Instrumentation | Glass-cockpit retrofits and IFE power upgrades are sustaining mid-single-digit growth. |

Emergency and backup power remains the largest application by revenue. Still, the strategic center of gravity is shifting toward propulsion applications as eVTOL and hybrid-electric platforms move from prototype to production.

By Aircraft Battery Market

| Sub-Segment | Key Trend |

| Traditional | Largest share; battery demand driven by auxiliary and emergency systems |

| Hybrid-Electric | Demonstrators transitioning to certification; regional turboprop conversions leading. |

| Fully Electric | Highest CAGR; eVTOL and light sport aircraft platforms at the forefront |

Traditional aircraft platforms generate the bulk of current battery revenue through auxiliary and emergency installations. Still, fully electric platforms are capturing the fastest growth trajectory as type-certification milestones unlock commercial orders.

By Aircraft Type

| Sub-Segment | Key Trend |

| Fixed-Wing | Dominant share from commercial narrowbody/widebody fleets |

| Rotary Wing | Defense and offshore helicopter operations are sustaining steady demand. |

| Advanced Air Mobility (AAM) | Fastest growth from eVTOL certification and vertiport buildout |

| Unmanned (UAS/Drone) | Mid-tier growth from cargo drone logistics and ISR missions |

Fixed-wing aircraft account for the majority of installed battery units, but the advanced air-mobility segment is growing at the fastest rate as new eVTOL platforms enter service and urban vertiport networks expand globally.

By Power Density

| Sub-Segment | Key Trend |

| Below 300 Wh/kg | Current-generation Li-ion packs; dominant installed base |

| 300–500 Wh/kg | Silicon-anode and high-nickel cathode cells are entering qualification. |

| Above 500 Wh/kg | Solid-state and Li-S cells in early-stage flight testing |

Cells below 300 Wh/kg dominate today's fleet, but aggressive R&D in solid-state and lithium-sulfur chemistries is pushing the frontier above 500 Wh/kg, with aviation qualification expected in the early 2030s.

By End User

| Sub-Segment | Key Trend |

| OEM | Line-fit dominance; battery selection locked during aircraft design |

| Aftermarket | Accelerating as first-generation Li-ion packs reach replacement age |

OEM channels capture the majority of revenue because battery specifications are determined during platform certification. Aftermarket volumes are rising as early lithium-ion installations approach their 8–10-year service-life limits, creating a growing replacement cycle.