Global market valuation was derived through revenue mapping and rig activity analysis. The methodology included:

Identification of 35+ key manufacturers and service providers across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa

Technology mapping across nuclear magnetic resonance, electromagnetic, acoustic, and hybrid MWD systems

Component analysis covering sensors (directional, gamma ray, resistivity), software (data analytics, visualization platforms), and hardware (downhole tools, surface systems)

End-use segmentation across onshore (conventional, unconventional, shale) and offshore (shallow water, deepwater, ultra-deepwater) drilling operations

Analysis of reported and modeled annual revenues specific to MWD service lines and equipment portfolios

Coverage of manufacturers and service providers representing 75-80% of global market share in 2024

Extrapolation using bottom-up (active rig count × MWD service intensity × day rates by region) and top-down (company revenue validation across Schlumberger, Halliburton, Baker Hughes, Weatherford, NOV, and regional players) approaches to derive segment-specific valuations

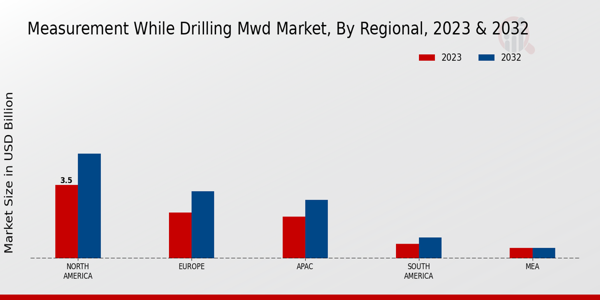

시장 Regional Image")

시장 key player")

시장 key player")

시장 key player")

시장 key player")

시장 key player")

시장 key player")

.webp?v=1782130000)