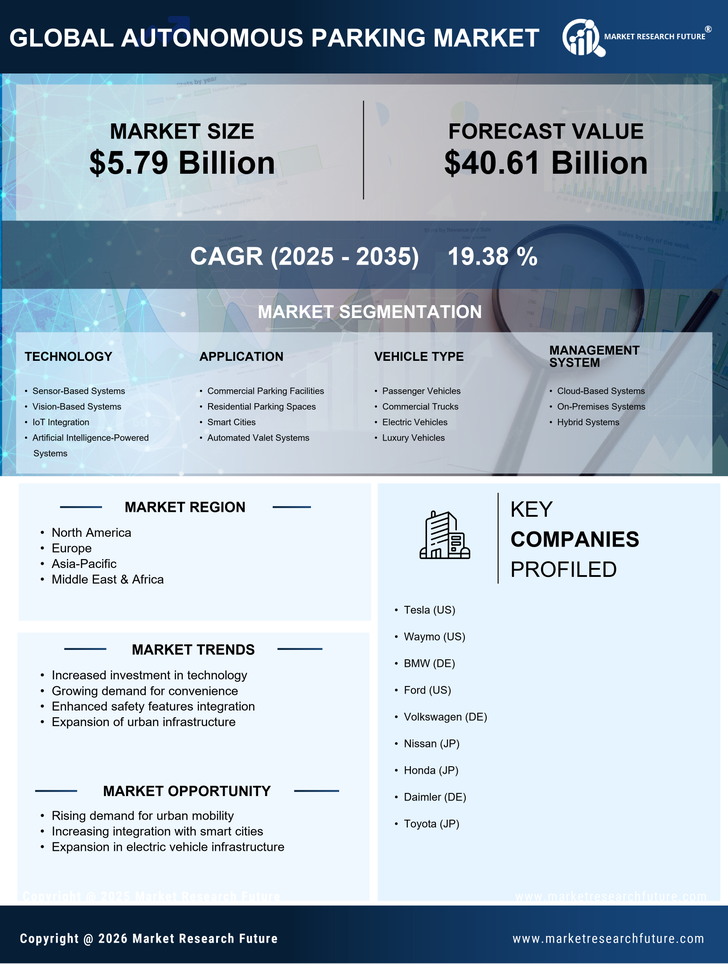

Segmentierung des Marktes für autonomes Parken

Markt für autonomes Parken nach Technologie (Milliarden USD, 2019-2032)

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken nach Anwendung (Milliarden USD, 2019-2032)

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken nach Fahrzeugtyp (Milliarden USD, 2019-2032)

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken nach Managementsystem (Milliarden USD, 2019-2032)

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken nach Endbenutzer (Milliarden USD, 2019-2032)

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Markt für autonomes Parken nach Region (Milliarden USD, 2019-2032)

Nordamerika

Europa

Südamerika

Asien-Pazifik

Mittlerer Osten und Afrika

Regionale Perspektive des Marktes für autonomes Parken (Milliarden USD, 2019-2032)

Perspektive Nordamerika (Milliarden USD, 2019-2032)

Markt für autonomes Parken in Nordamerika nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in Nordamerika nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in Nordamerika nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in Nordamerika nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in Nordamerika nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Markt für autonomes Parken in Nordamerika nach regionalem Typ

USA

Kanada

Perspektive USA (Milliarden USD, 2019-2032)

Markt für autonomes Parken in den USA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in den USA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in den USA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in den USA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in den USA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

KANADA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in KANADA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in KANADA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in KANADA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in KANADA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in KANADA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Perspektive Europa (Milliarden USD, 2019-2032)

Markt für autonomes Parken in Europa nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in Europa nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in Europa nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in Europa nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in Europa nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Markt für autonomes Parken in Europa nach regionalem Typ

Deutschland

Vereinigtes Königreich

Frankreich

Russland

Italien

Spanien

Rest von Europa

DEUTSCHLAND Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in DEUTSCHLAND nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in DEUTSCHLAND nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in DEUTSCHLAND nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in DEUTSCHLAND nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in DEUTSCHLAND nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

VEREINIGTES KÖNIGREICH Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken im VEREINIGTEN KÖNIGREICH nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken im VEREINIGTEN KÖNIGREICH nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken im VEREINIGTEN KÖNIGREICH nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken im VEREINIGTEN KÖNIGREICH nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken im VEREINIGTEN KÖNIGREICH nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

FRANKREICH Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in FRANKREICH nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in FRANKREICH nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in FRANKREICH nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in FRANKREICH nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in FRANKREICH nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

RUSSLAND Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in RUSSLAND nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in RUSSLAND nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in RUSSLAND nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in RUSSLAND nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in RUSSLAND nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

ITALIEN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in ITALIEN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in ITALIEN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in ITALIEN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in ITALIEN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in ITALIEN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

SPANIEN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in SPANIEN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in SPANIEN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in SPANIEN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in SPANIEN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in SPANIEN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

REST VON EUROPA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken im REST VON EUROPA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken im REST VON EUROPA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken im REST VON EUROPA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken im REST VON EUROPA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken im REST VON EUROPA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

APAC Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in APAC nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in APAC nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in APAC nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in APAC nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in APAC nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Markt für autonomes Parken in APAC nach regionalem Typ

China

Indien

Japan

Südkorea

Malaysia

Thailand

Indonesien

Rest von APAC

CHINA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in CHINA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in CHINA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in CHINA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in CHINA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in CHINA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

INDIEN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in INDIEN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in INDIEN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in INDIEN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in INDIEN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in INDIEN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

JAPAN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in JAPAN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in JAPAN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in JAPAN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in JAPAN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in JAPAN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

SÜDKOREA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in SÜDKOREA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in SÜDKOREA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in SÜDKOREA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in SÜDKOREA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in SÜDKOREA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

MALAYSIA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in MALAYSIA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in MALAYSIA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in MALAYSIA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in MALAYSIA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in MALAYSIA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

THAILAND Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in THAILAND nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in THAILAND nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in THAILAND nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in THAILAND nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in THAILAND nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

INDONESIEN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in INDONESIEN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in INDONESIEN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in INDONESIEN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in INDONESIEN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in INDONESIEN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

REST VON APAC Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken im REST VON APAC nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken im REST VON APAC nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken im REST VON APAC nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken im REST VON APAC nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken im REST VON APAC nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Perspektive Südamerika (Milliarden USD, 2019-2032)

Markt für autonomes Parken in Südamerika nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in Südamerika nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in Südamerika nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in Südamerika nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in Südamerika nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Markt für autonomes Parken in Südamerika nach regionalem Typ

Brasilien

Mexiko

Argentinien

Rest von Südamerika

BRAZILIEN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in BRAZILIEN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in BRAZILIEN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in BRAZILIEN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in BRAZILIEN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in BRAZILIEN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

MEKSIKO Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in MEKSIKO nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in MEKSIKO nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in MEKSIKO nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in MEKSIKO nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in MEKSIKO nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

ARGENTINIEN Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in ARGENTINIEN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in ARGENTINIEN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in ARGENTINIEN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in ARGENTINIEN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in ARGENTINIEN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

REST VON SÜDAMERIKA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken im REST VON SÜDAMERIKA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken im REST VON SÜDAMERIKA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken im REST VON SÜDAMERIKA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken im REST VON SÜDAMERIKA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken im REST VON SÜDAMERIKA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

MEA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in MEA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in MEA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in MEA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in MEA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in MEA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

Markt für autonomes Parken in MEA nach regionalem Typ

GCC-Länder

Südafrika

Rest von MEA

GCC-LÄNDER Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in GCC-LÄNDERN nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in GCC-LÄNDERN nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in GCC-LÄNDERN nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in GCC-LÄNDERN nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in GCC-LÄNDERN nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

SÜDAFRIKA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken in SÜDAFRIKA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken in SÜDAFRIKA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken in SÜDAFRIKA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken in SÜDAFRIKA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken in SÜDAFRIKA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber

REST VON MEA Perspektive (Milliarden USD, 2019-2032)

Markt für autonomes Parken im REST VON MEA nach Technologietyp

Sensorbasierte Systeme

Visionsbasierte Systeme

IoT-Integration

Von künstlicher Intelligenz unterstützte Systeme

Markt für autonomes Parken im REST VON MEA nach Anwendungstyp

Kommerzielle Parkeinrichtungen

Wohnparkplätze

Intelligente Städte

Automatisierte Valet-Systeme

Markt für autonomes Parken im REST VON MEA nach Fahrzeugtyp

Personenwagen

Lastkraftwagen

Elektrofahrzeuge

Luxusfahrzeuge

Markt für autonomes Parken im REST VON MEA nach Managementsystemtyp

Cloudbasierte Systeme

On-Premises-Systeme

Hybridsysteme

Markt für autonomes Parken im REST VON MEA nach Endbenutzertyp

Öffentlicher Sektor

Privater Sektor

Immobilienentwickler

Flottenbetreiber