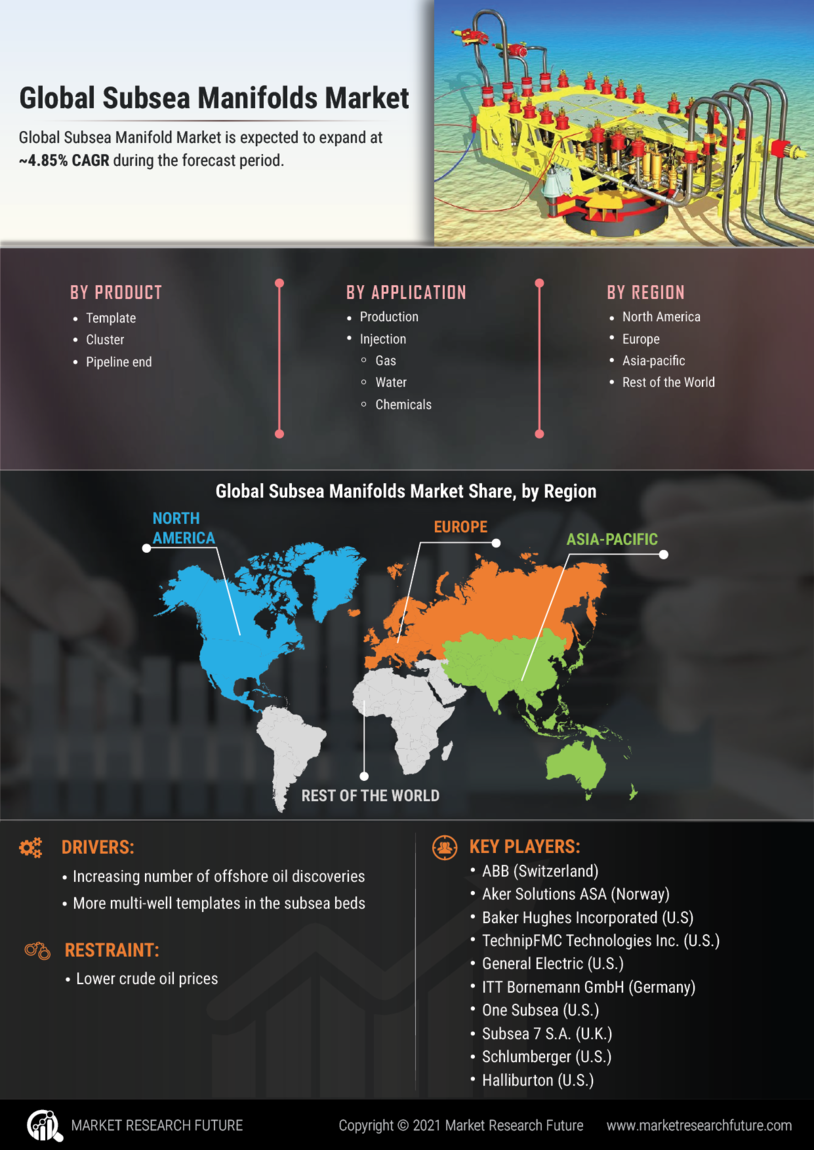

Global Subsea Manifolds Market Overview

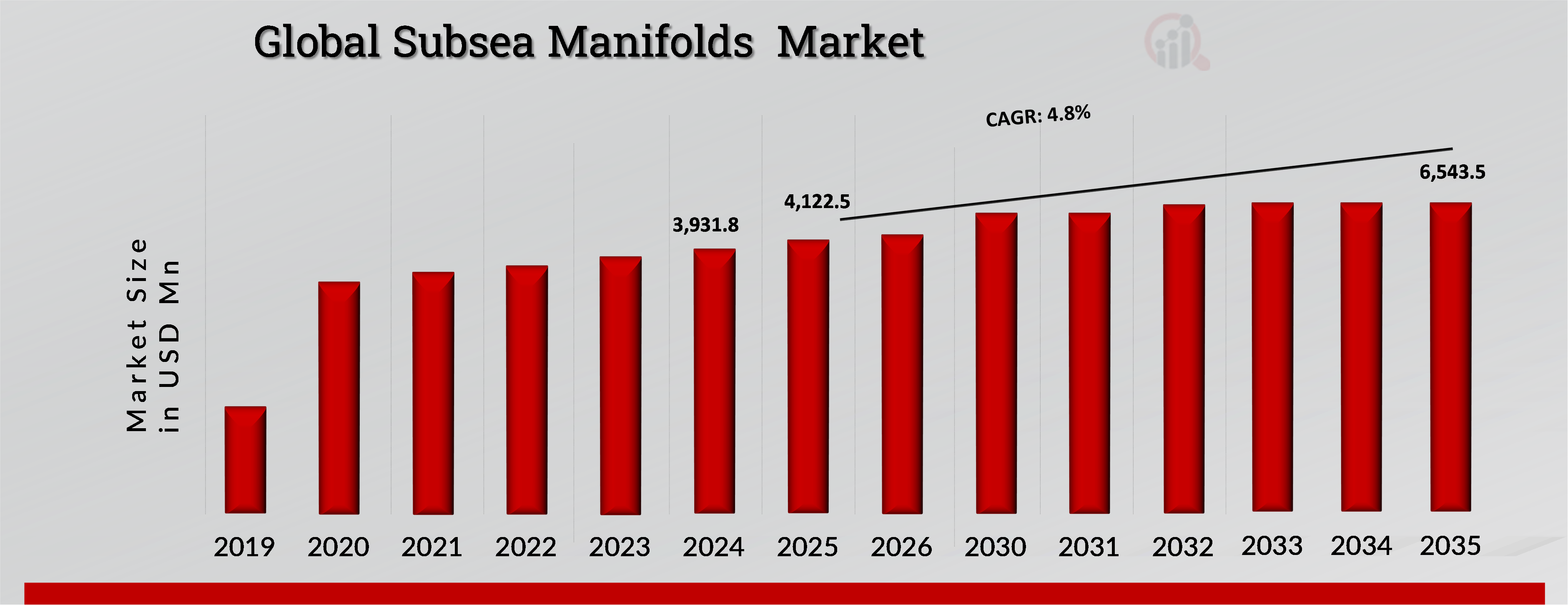

Subsea Manifolds Market Size was valued at USD 3,931.8 Million in 2024. The Global Subsea Manifolds industry is projected to grow from USD 4,122.5 Million in 2024 to USD 6,543.5 Million by 2035, exhibiting a compound annual growth rate (CAGR) of 4.8% during the forecast period (2024 - 2035) Increasing Offshore Oil and Gas Exploration Activities and Growing Demand for Deepwater and Ultra-deepwater Developments is driving the Subsea Manifolds Market.

Source: Secondary Research, Primary Research, MRFR Database, and Analyst Review

Subsea Manifolds Market Trends

Expansion of Subsea Infrastructure in Emerging Markets

The growth of subsea infrastructure in emerging markets represents a substantial opportunity for the Subsea Manifolds Market. As oil and gas production in traditional onshore and shallow sea assets decreases, many energy corporations are going to more remote and undeveloped resources in deepwater and ultra-deepwater regions, particularly in developing countries. These regions, which include sections of Southeast Asia, West Africa, the Middle East, and Latin America, are becoming more recognized as significant growth areas for the oil and gas industry. Subsea manifolds, which manage the flow of hydrocarbons between subsea wells and surface facilities, are critical to the growing offshore oil and gas operations.

Emerging markets are often home to massive, underexplored offshore reserves. For instance, West Africa's offshore oil reserves, particularly those in Angola, Nigeria, and Ghana, are attracting significant investment in subsea infrastructure as operators seek to develop undiscovered deepwater resources. Similarly, the deepwater fields off Brazil's coast, which have emerged as important oil and gas producers in recent years, rely largely on subsea manifolds to improve output and manage complex reservoir flows. As more oil and gas deposits in these locations are discovered, the demand for subsea systems, particularly manifolds, will increase.

The improvement of subsea technology is one of the primary drivers of subsea infrastructure expansion in emerging markets. Many of these markets now allow operators to develop and produce from fields that used to be considered too expensive or technically difficult. Deepwater and ultra-deepwater resources are becoming more accessible due to advancements including subsea production systems, remote monitoring, and enhanced riser technology.

Subsea Manifolds Market Segment Insights

Global Subsea Manifolds Type Insights

Based on Type, the Subsea Manifolds market is segmented into :Template Manifold, Cluster Manifold, Pipeline End Manifold (PLEM). The Template Manifold segment dominated the global market in 2024, while the Template Manifold is projected to be the fastest–growing segment during the forecast period. A template manifold is a pre-engineered subsea structure designed to house and align multiple wellheads within a single framework, ensuring optimal routing of flowlines and umbilicals. This type of manifold is typically used in offshore oil and gas projects with a high density of wells in close proximity.

Its design allows for pre-drilling or pre-installation before the subsea production system is fully operational, which significantly reduces installation time and operational complexity. The use of template manifolds enhances the efficiency of well placement and minimizes the environmental footprint on the seabed. Moreover, they are highly adaptable to varying field requirements, making them suitable for both greenfield developments and brownfield expansions. By centralizing the flow from multiple wells, template manifolds enable seamless integration with upstream and downstream infrastructure, reducing costs and risks associated with subsea operations. They are especially valuable in deepwater fields, where precise well alignment and cost-efficiency are critical.

Global Subsea Manifolds Application Insights

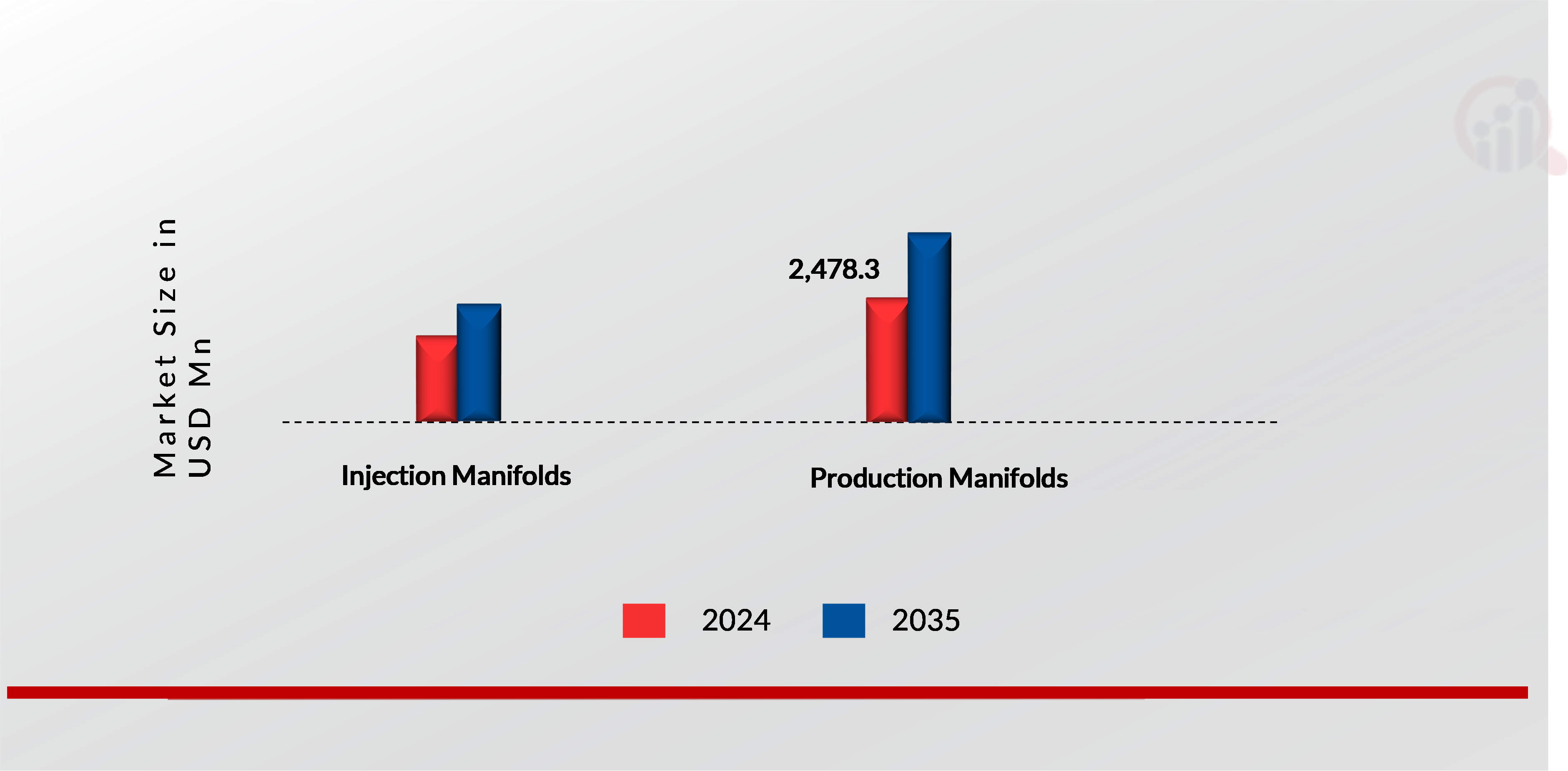

Based on Application, the Subsea Manifolds market is segmented into : Production Manifolds, Injection Manifolds. The Production Manifolds segment dominated the global market in 2024, while the Production Manifolds is projected to be the fastest–growing segment during the forecast period. Production manifolds are a vital component in subsea oil and gas extraction systems, designed to collect and manage the flow of hydrocarbons from multiple wells.

These manifolds act as central hubs where oil, gas, and water streams converge before being transported to processing facilities. Production manifolds play a key role in optimizing flow rates, pressure regulation, and flow assurance, ensuring consistent and efficient hydrocarbon recovery. Equipped with advanced control systems, production manifolds can monitor and adjust flow rates based on well performance, reservoir pressure, and downstream processing capacity.

They are typically deployed in offshore fields with multiple wells producing simultaneously, reducing the need for separate flowlines for each well. Additionally, production manifolds help minimize environmental risks by integrating safety systems such as emergency shut-down valves. In deepwater and ultra-deepwater fields, production manifolds are critical for managing the challenges posed by high pressures and temperatures. Their robust design and operational flexibility make them an essential component in modern offshore oil and gas production, enabling operators to maximize reservoir potential while maintaining system reliability.

Figure 1: SUBSEA MANIFOLDS MARKET, BY APPLICATION, 2024 & 2035 (USD Million)

Global Subsea Manifolds Water Depth Insights

Based on Application, the Subsea Manifolds market is segmented into: Production Manifolds, Injection Manifolds. The Shallow Water segment dominated the global market in 2024, while the Shallow Water is projected to be the fastest–growing segment during the forecast period. Production manifolds are a vital component in subsea oil and gas extraction systems, designed to collect and manage the flow of hydrocarbons from multiple wells. These manifolds act as central hubs where oil, gas, and water streams converge before being transported to processing facilities.

Production manifolds play a key role in optimizing flow rates, pressure regulation, and flow assurance, ensuring consistent and efficient hydrocarbon recovery. Equipped with advanced control systems, production manifolds can monitor and adjust flow rates based on well performance, reservoir pressure, and downstream processing capacity. They are typically deployed in offshore fields with multiple wells producing simultaneously, reducing the need for separate flowlines for each well.

Additionally, production manifolds help minimize environmental risks by integrating safety systems such as emergency shut-down valves. In deepwater and ultra-deepwater fields, production manifolds are critical for managing the challenges posed by high pressures and temperatures. Their robust design and operational flexibility make them an essential component in modern offshore oil and gas production, enabling operators to maximize reservoir potential while maintaining system reliability.

Global Subsea Manifolds Manufacturing Techniques Insights

Based on Manufacturing Techniques, the Subsea Manifolds market is segmented into: Powder Metallurgy and Hot Isostatic Pressing (PM HIP), Traditional. The Traditional segment dominated the market in 2024, while the Traditional segment is projected to be the fastest–growing segment during the forecast period. Traditional manufacturing techniques, such as casting, forging, and machining, remain widely used in the production of subsea manifolds.

These methods are well-established and cost-effective, making them suitable for simpler manifold designs and applications in shallow to moderate water depths. Casting involves pouring molten metal into molds to form the desired shape, while forging uses compressive forces to shape heated metal. Machining further refines the component to achieve precise dimensions and finishes.

Global Subsea Manifolds Regional Insights

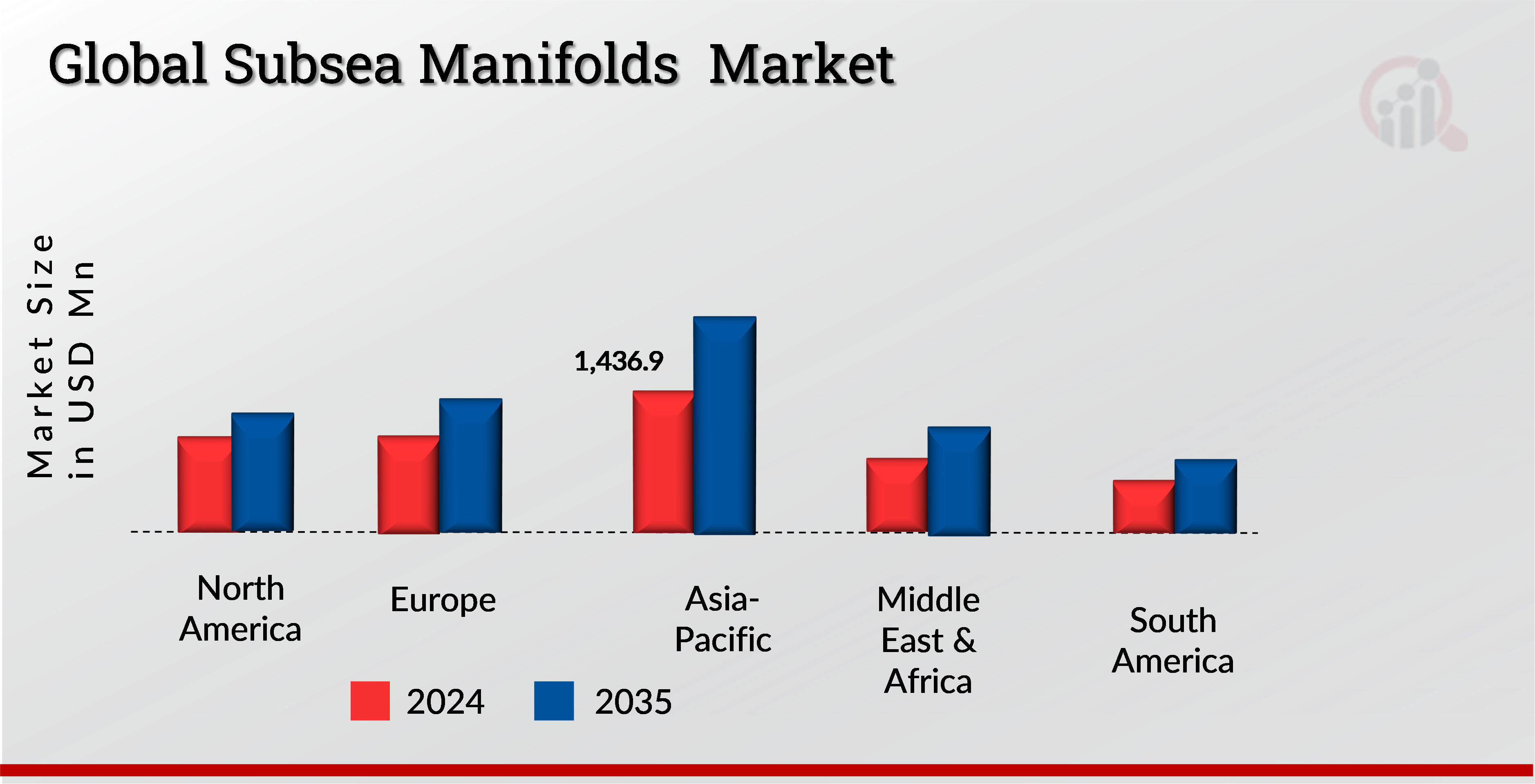

By Region, the study provides market insights into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The Asia-Pacific Subsea Manifolds market accounted for largest market share in 2024 and South America is expected to exhibit a significant CAGR growth during the study period. The Asia-Pacific (APAC) region is the largest market for subsea manifolds due to rapid growth in offshore oil and gas exploration.

Countries like Australia, China, India, and Malaysia have vast offshore reserves, driving demand for subsea infrastructure. The shift to deeper, more complex fields, particularly in deepwater and ultra-deepwater, has increased reliance on advanced subsea systems, including manifolds. Additionally, the rise of FPSOs and growing energy needs across the region, coupled with favorable government policies and technological advancements, further boosts market demand. APAC's significant offshore projects and investments in energy diversification make it a key hub for subsea manifold solutions.

South America, particularly Brazil, is expected to exhibit significant CAGR growth in the subsea manifolds market due to expanding offshore oil and gas reserves, especially in the pre-salt fields of the Santos Basin. These reserves are located in deepwater and ultra-deepwater, requiring advanced subsea technologies, including manifolds, to optimize production. Brazil's major investments in offshore exploration, led by Petrobras, and government policies promoting energy sector growth further drive demand. As the region moves toward more complex and remote fields, the need for efficient subsea infrastructure to manage fluid flow and enhance production becomes critical. This, combined with technological advancements, positions South America for strong market growth during the study period.

Figure 2: Subsea Manifolds Market, by region, 2024 & 2035 (USD Million)

Further, the major countries studied in the market report are the U.S., Canada, Mexico, Germany, France, Italy, UK, Spain, Japan, UAE, South Africa, Saudi Arabia, Argentina, and Brazil.

Global Subsea Manifolds Key Market Players & Competitive Insight

Many global, regional, and local vendors characterize the Subsea Manifolds Market. The market is highly competitive, with all the players competing to gain market share. Intense competition, rapid advances in technology, frequent changes in government policies, and environmental regulations are key factors that confront market growth. The vendors compete based on cost, product quality, reliability, and government regulations. Vendors must provide cost-efficient, high-quality products to survive and succeed in an intensely competitive market.

The major players in the market include SLB, Aker Solutions, TechnipFMC plc, Subsea7, Oceaneering International, Inc., among others. The Subsea Manifolds Market is a consolidated market due to increasing competition, acquisitions, mergers and other strategic market developments and decisions to improve operational effectiveness.

Key Companies in the Subsea Manifolds Market include

- SLB

- Aker Solutions

- TechnipFMC plc

- Subsea7

- Oceaneering International, Inc

Global Subsea Manifolds Industry Developments

- In July 2024, SLB OneSubsea and Subsea 7 have been awarded an integrated EPCI contract for bp's North Sea Murlach development. SLB OneSubsea will provide two vertical monobore trees, a two-slot manifold, and associated topside controls. Subsea 7 will be responsible for installing 8 kilometers of rigid flowline and two flexible jumpers, including a new gas lift flowline tied back to the Eastern Trough Area Project (ETAP) facility.

-

- In August 2023, Aker BP, Aker Solutions, and Subsea 7 have officially launched production work on the first of three seabed installations (subsea manifolds) for the Skarv Satellite Project (SSP) at Aker Solutions’ workshop facilities in Sandnessjøen.

Subsea Manifolds Market Segmentation

Subsea Manifolds Market by Type Outlook (USD Million, 2019-2035)

- Template Manifold

- Cluster Manifold

- Pipeline End Manifold (PLEM)

Subsea Manifolds Market by Application Outlook (USD Million, 2019-2035)

- Production Manifolds

- Injection Manifolds

Subsea Manifolds Market by Water Depth Outlook (USD Million, 2019-2035)

Subsea Manifolds Market by Manufacturing Techniques Outlook (USD Million, 2019-2035)

- Powder Metallurgy and Hot Isostatic Pressing (PM HIP)

- Traditional

Global Subsea Manifolds Regional Outlook

|

Report Attribute/Metric

|

Details

|

|

Market Size 2024

|

USD 3,931.8 Million

|

|

Market Size 2024

|

USD 4,122.5 Million

|

|

Market Size 2035

|

USD 6,543.5Million

|

|

Compound Annual Growth Rate (CAGR)

|

4.8% (2024-2035)

|

|

Base Year

|

2024

|

|

Market Forecast Period

|

2025-2035

|

|

Historical Data

|

2019- 2023

|

|

Market Forecast Units

|

Value (USD Million)

|

|

Report Coverage

|

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends

|

|

Segments Covered

|

Type, Application, Water Depth, Manufacturing Techniques and Region

|

|

Geographies Covered

|

North America, Europe, Asia-Pacific, Middle East & Africa, and South America.

|

|

Countries Covered

|

The U.S., Canada, Mexico, Germany, France, Italy, UK, Spain, China, Japan, India, UAE, South Africa, Saudi Arabia, Argentina, and Brazil.

|

|

Key Companies Profiled

|

SLB, Aker Solutions, TechnipFMC plc, Subsea7, Oceaneering International, Inc., among others

|

|

Key Market Opportunities

|

· EXPANSION OF SUBSEA INFRASTRUCTURE IN EMERGING MARKETS

· IMPACT ANALYSIS OF COVID - 19

|

|

Key Market Dynamics

|

· INCREASING OFFSHORE OIL AND GAS EXPLORATION ACTIVITIES

· GROWING DEMAND FOR DEEPWATER AND ULTRA-DEEPWATER DEVELOPMENTS

|

Subsea Manifolds Market Highlights:

Frequently Asked Questions (FAQ) :

The Subsea Manifolds Market size is expected to be valued at USD 6,543.5 Million in 2035.

The global market is projected to grow at a CAGR of 4.8% during the forecast period, 2024-2035.

Asia Pacific had the largest share of the global market.

The key players in the market are SLB, Aker Solutions, TechnipFMC plc, Subsea7, Oceaneering International, Inc., among others.

The Production Manifolds category dominated the market in 2024.

The Template Manifold segment had the largest revenue share of the global market.