Home Healthcare Market Summary

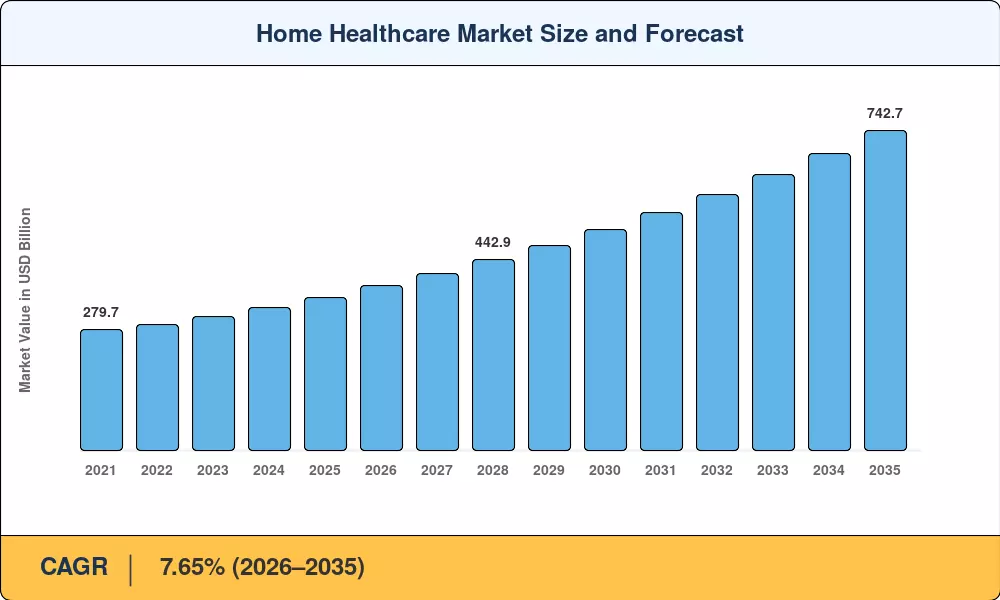

The Global Home Healthcare Market size was valued at USD 355.00 Billion in 2025, and the market is projected to grow from USD 382.20 Billion in 2026 to USD 742.70 Billion by 2035, registering a CAGR of 7.65% during the forecast period 2026–2035. This trajectory is anchored by aging demographics across OECD nations and a decisive policy shift toward value-based reimbursement that rewards care delivered outside hospital walls. The U.S. Centers for Medicare & Medicaid Services broadened its Acute Hospital Care at Home waiver program in 2024, enabling over 300 health systems to bill inpatient-equivalent rates for residential episodes — a direct fiscal catalyst that reshaped capital allocation across the Home Healthcare Market [2].

Technology transformation is rewriting the delivery model. Legacy paper-based scheduling and manual vitals logging are giving way to cloud-hosted agency platforms, edge-computing biosensors, and AI-driven clinical decision support. The global digital health investment pool channeled roughly USD 18.5 Billion into connected home-care technologies between 2022 and 2024, with remote patient monitoring devices and predictive analytics attracting the largest funding rounds [3]. Device miniaturization has cut the per-unit cost of continuous glucose monitors and portable ECG patches by an estimated 30% since 2021, widening access in cost-sensitive emerging economies [4].

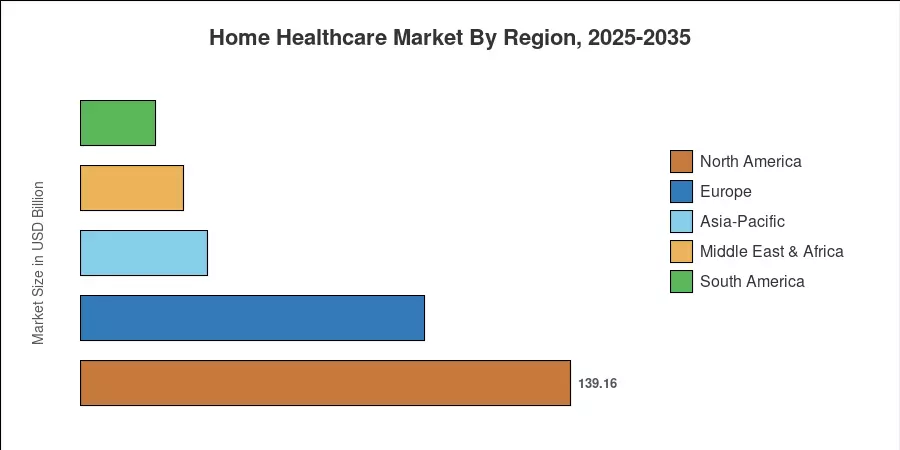

North America retained a 39.20% revenue share in 2025, driven by deep Medicare fee-for-service penetration and a mature staffing infrastructure. Asia-Pacific is on track to be the fastest-growing geography at a 10.15% CAGR through 2035, fueled by rising geriatric populations in Japan, rapid insurance expansion in India, and government digitization mandates across ASEAN [5]. Europe held the second-largest share at 27.50%, supported by EU-funded integrated care programs. The Home Healthcare Market will increasingly be defined by the convergence of clinical-grade wearables, telehealth platforms, and payer-led care-coordination models through the remainder of the decade.

Key Report Takeaways

• By Healthcare Type

- Equipment commanded the leading share of the Home Healthcare Market in 2025, anchoring 45.20% of total revenue through therapeutic and diagnostic device categories.

- Software Platforms are forecast to deliver the fastest segment expansion, advancing at a 13.10% CAGR to 2035 as agencies migrate from on-premise scheduling tools to cloud-native suites.

• By Indication

- Cardiovascular conditions accounted for 24.70% of the 2025 Home Healthcare Market revenue mix, reflecting high demand for portable cardiac monitors.

- Diabetes care is projected to grow at an 11.70% CAGR through 2035, propelled by the global surge in continuous glucose monitoring adoption.

• By Region

- North America dominated the Home Healthcare Market with a 39.20% share in 2025.

- Asia-Pacific is poised for the fastest regional CAGR of 10.15% over the forecast window.

Market Size and Forecast (2021–2035)

Market Research Future derives size estimates through a triangulated approach combining top-down revenue analysis, bottom-up device and service shipment data, primary interviews with 120+ home health agency executives, and validated secondary databases from CMS, WHO, and regional payer authorities.