Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

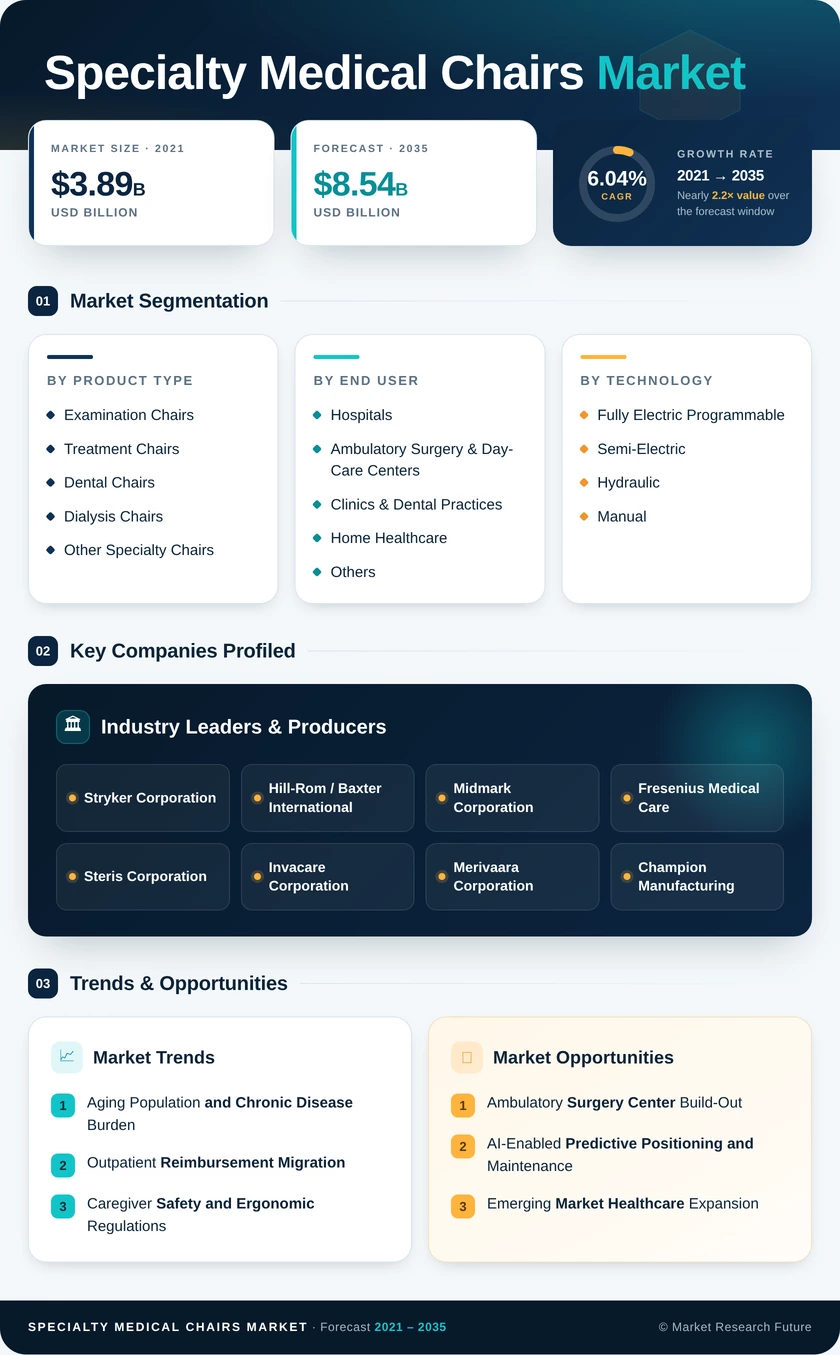

| Product Type | Examination Chairs, Treatment Chairs, Dental Chairs, Dialysis Chairs, Other Specialty Chairs | Examination Chairs (40.7% share, 2025) | Treatment Chairs (7.84% CAGR) |

| End User | Hospitals, Ambulatory Surgery & Day-Care Centers, Clinics & Dental Practices, Home Healthcare, Others | Hospitals (39.8% share, 2025) | Ambulatory Surgery & Day-Care Centers (9.95% CAGR) |

| Technology | Fully Electric Programmable, Semi-Electric, Hydraulic, Manual | Fully Electric Programmable (41.4% share, 2025) | Fully Electric Programmable (leading CAGR) |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (39.2% share, 2025) | Asia-Pacific (8.14% CAGR) |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Examination Chairs | Transition to barrier-free, height-adjustable electric models in primary care |

| Treatment Chairs | Multi-hour session ergonomics for infusion and chemotherapy applications |

| Dental Chairs | Integration of LED operating lights and digital imaging mounts |

| Dialysis Chairs | Extended-comfort designs for 3–4-hour renal therapy sessions |

| Other Specialty Chairs | Niche growth in ophthalmic, podiatric, and ENT-specific configurations |

Product type segmentation reflects the functional diversity of clinical environments where specialty seating is deployed. Examination chairs serve the broadest installed base across primary care, urgent care, and emergency departments, while treatment chairs are experiencing accelerated adoption driven by ambulatory infusion therapy volumes.

By End User

| Sub-Segment | Key Trend |

| Hospitals | Fleet replacement aligned with Joint Commission and pressure-injury standards |

| Ambulatory Surgery & Day-Care Centers | Fastest-growing segment driven by reimbursement migration |

| Clinics & Dental Practices | Private-practice modernization and patient-experience competition |

| Home Healthcare | Compact, patient-operated designs for hospital-at-home programs |

| Others | Research institutions, military medical, and correctional healthcare |

End-user segmentation captures the migration of procedural volumes from traditional inpatient settings to ambulatory and decentralized care environments. Hospitals remain the largest buyer, but growth momentum is shifting toward ambulatory surgery centers and home healthcare as payer policies incentivize lower-cost care delivery sites.

By Technology

| Sub-Segment | Key Trend |

| Fully Electric Programmable | IoT sensor integration, EHR connectivity, over-the-air updates |

| Semi-Electric | Cost-effective mid-tier adoption in multi-provider clinics |

| Hydraulic | Legacy installed base in emerging markets with gradual replacement |

| Manual | Entry-level positioning for basic examination settings |

Technology segmentation reflects the ongoing electrification of specialty medical seating. Fully electric programmable platforms command the largest share and fastest growth, driven by caregiver safety mandates and healthcare IT integration requirements. Hydraulic and manual chairs continue to serve cost-sensitive and low-acuity environments but face declining share over the forecast period.