Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Product Type | Hardware, Software, Services | Hardware | Services |

| Technology Type | Fibre Channel SAN, iSCSI SAN, NVMe-over-Fabrics, Others | Fibre Channel SAN | NVMe-over-Fabrics |

| Organization Size | Large Enterprises, Small and Medium Enterprises | Large Enterprises | Small and Medium Enterprises |

| End-User Industry | BFSI, IT and Telecom, Healthcare and Life Sciences, Media and Entertainment, Cloud Service Providers, Others | BFSI | Cloud Service Providers |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

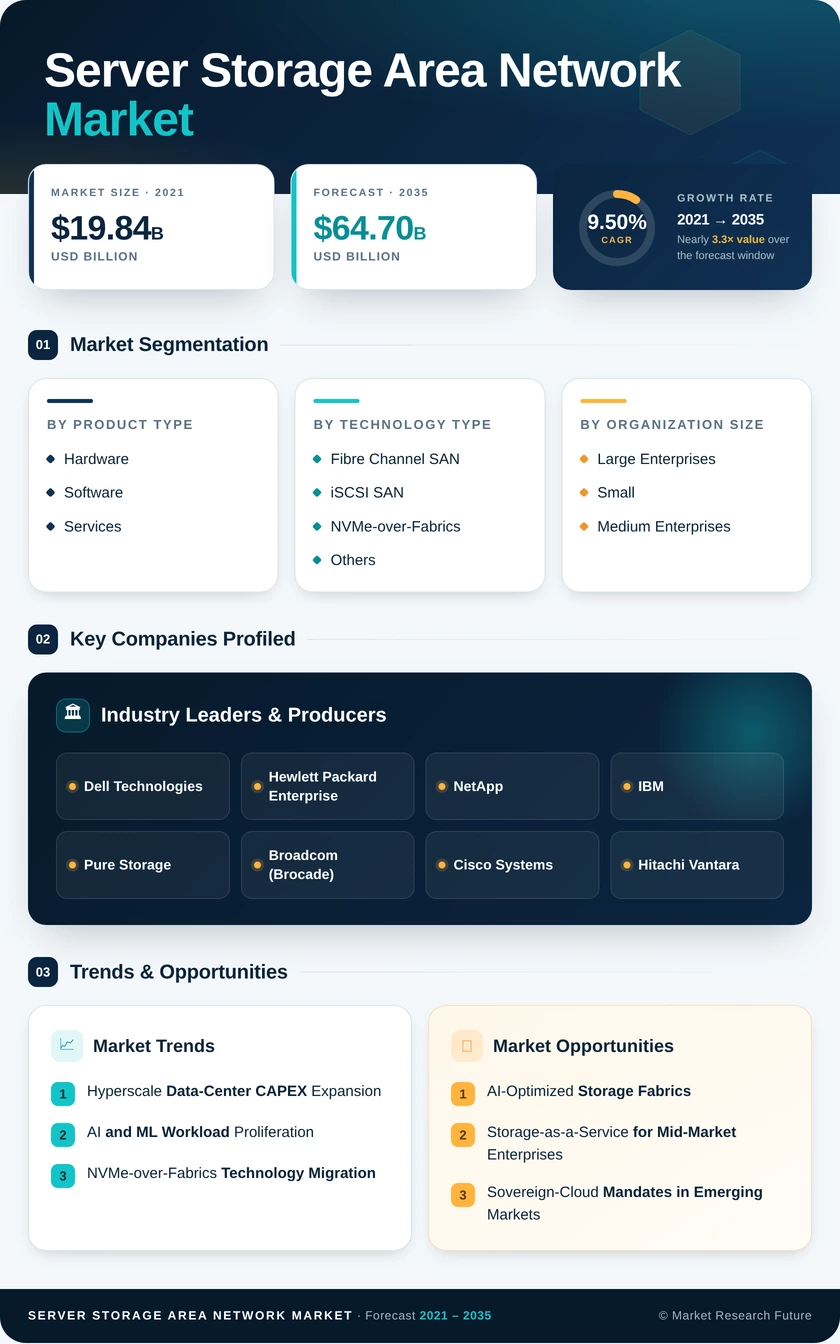

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Hardware | 64 Gbps and 128 Gbps Fibre Channel director upgrades; NVMe all-flash array adoption |

| Software | Software-defined SAN orchestration; AIOps-driven capacity planning |

| Services | Growth of managed-SAN and STaaS consumption models; professional fabric-design services |

Hardware continues to anchor the market's revenue base, though its share is gradually contracting as software-defined platforms commoditize switching and routing functions. Services are gaining momentum as enterprises prioritize operational expenditure flexibility and outsource fabric management to vendors and managed-service providers.

By Technology Type

| Sub-Segment | Key Trend |

| Fibre Channel SAN | Transition from 32 Gbps to 64 Gbps; FC-NVMe-3 standard adoption |

| iSCSI SAN | Cost-effective entry point for SMEs; convergence with standard Ethernet infrastructure |

| NVMe-over-Fabrics | Sub-10-microsecond latency for AI and analytics; rapid adoption in hyperscale environments |

| Others (FCoE, InfiniBand) | Niche HPC and legacy interoperability use cases |

Fibre Channel remains the default for mission-critical workloads where lossless delivery and mature management tooling are essential. NVMe-over-Fabrics is displacing iSCSI in performance-sensitive tiers and is expected to narrow the gap with Fibre Channel over the forecast period.

By Organization Size

| Sub-Segment | Key Trend |

| Large Enterprises | Multi-petabyte SAN estates; regulatory-driven refresh cycles |

| Small and Medium Enterprises | Cloud-managed SAN appliances; subscription-based entry models |

Large enterprises drive the majority of SAN spending due to mission-critical uptime requirements and compliance mandates. SMEs are the fastest-growing segment as simplified appliances and consumption models lower the technical and financial barriers to SAN adoption.

By End-User Industry

| Sub-Segment | Key Trend |

| BFSI | Real-time transaction processing; regulatory archiving under PCI DSS and Basel III |

| IT and Telecom | 5G core network storage; edge data-center buildout |

| Healthcare and Life Sciences | PACS/DICOM imaging growth; genomics data pipeline acceleration |

| Media and Entertainment | 4K/8K content ingest and post-production workflows |

| Cloud Service Providers | Multi-tenant block-storage services; custom SAN fabric designs |

| Others (Government, Manufacturing) | Smart-city data platforms; Industry 4.0 digital-twin storage |

BFSI leads end-user demand thanks to stringent latency and data-integrity requirements imposed by global financial regulators. Cloud service providers are the fastest-growing vertical as regional and sovereign-cloud operators replicate hyperscaler storage architectures.