Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

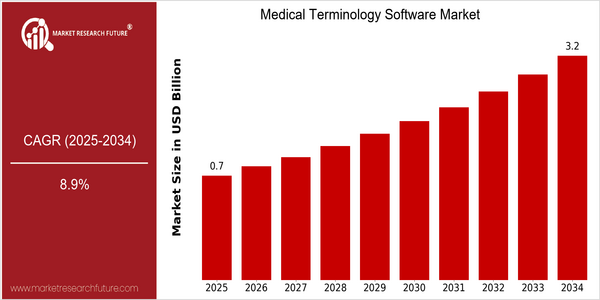

Medical Terminology Software Market Size Snapshot

| Year | Value |

|---|---|

| 2025 | USD 0.67 Billion |

| 2034 | USD 3.25 Billion |

| CAGR (2025-2034) | 8.9 % |

Note – Market size depicts the revenue generated over the financial year

The Medical Terminology Software Market is set to reach USD 2.13 billion by 2025, growing at a CAGR of 9.6% during the forecast period. The increasing complexity of health data and the need for accurate clinical documentation have driven the demand for medical terminologies. A number of factors, such as the growing adoption of EHRs, the development of artificial intelligence and natural language processing, and the growing need for interoperability between medical systems, are driving the growth of the medical terminology market. These technological developments are enhancing the efficiency and accuracy of medical coding, thereby reducing the administrative burden on health care service providers. The key players in the market, such as 3M Health Information Systems, Optum, and Cerner, are focusing on strengthening their market positions through strategic initiatives, such as acquisitions and product innovations.

Regional Deep Dive

Medical terminology software market is expected to witness significant growth on account of the increasing need for accurate medical documentation, interoperability between different healthcare systems, and the rising adoption of EHRs. North America is characterized by an advanced healthcare system and a strong regulatory framework. Europe is characterized by a diverse landscape influenced by the difference in healthcare policies and technological advancements. The Asia-Pacific region is witnessing rapid digital transformation of the healthcare sector, with the emerging economies investing heavily in health IT solutions. The Middle East and Africa are gradually adopting medical terminology software, with the government initiatives to improve the healthcare system. Latin America is focusing on increasing the access to healthcare through technology.

North America

- In the United States, the implementation of the 21st Century Cures Act has led to a sharp increase in the use of standardized medical terminology and a significant increase in the use of medical terminology software.

- Cerner and Epic have a leading position in the market, and have continuously improved their products to meet the needs of end users and comply with regulations.

- The rise of telemedical services, which was hastened by the COVID-19 epidemic, has created a demand for medical terminology software which can be easily incorporated in the virtual care platforms.

Europe

- The General Data Protection Regulation (GDPR) of the European Union is driving the use of medical terminology software in hospitals. This is mainly to ensure the privacy and security of personal data.

- In the field of medical terminology, Philips and Siemens Healthineers are investing in the development of AI-based medical terminology solutions to improve clinical decision-making and patient outcomes, and thereby showcasing innovation in the region.

- Germany and the United Kingdom are among the countries which have set themselves the task of establishing patient-oriented medicine, and therefore need a system which will accurately register and interpret complex medical data.

Asia-Pacific

- India and China are rapidly digitising their health systems, and in India, the National Digital Health Mission is encouraging the use of medical terminology software.

- The rise of health-tech companies in the region, such as Practo and HealthifyMe, has spurred innovation and competition in the medical terminology software market, and has resulted in the development of solutions tailored to local needs.

- In Asia, where the use of herbal medicine is more common, the need for a unified medical terminology has been emphasized.

MEA

- The Vision 2021 initiative aims to improve healthcare through technology, and this has led to a growing investment in medical terminology software to assist health care professionals.

- The Council of Health in Saudi Arabia has been advocating the use of standardized medical terminology in order to improve the quality of care and patient safety in the Kingdom.

- Economic factors, such as fluctuations in oil prices, are affecting health budgets, which governments are trying to optimize by using medical terminology software.

Latin America

- The Ministry of Health is launching a programme to encourage the use of clinical terminology programmes in order to improve data collection and health care management.

- Latin American hospitals are increasingly adopting new information technology solutions to manage the documentation and treatment of chronic patients.

- The diversity of the population in the region requires the development of medical terminology software which can accommodate several languages and dialects, which influences the development of the product.

Did You Know?

“In fact, 80% of the data collected in the medical field is unstructured, and it is mainly medical terminology software that is responsible for converting this data into actionable information.” — HealthIT.gov

Segmental Market Size

The Medical Terminology Software plays an important role in promoting communication and data interoperability in the health sector. This market is currently growing steadily, mainly driven by the increasing need for accurate medical coding and billing and the need for better EHRs. This is a result of the growing trend towards value-based care, which requires more accurate documentation, and the implementation of regulatory standards such as ICD-10, which requires health care organizations to use standardized terminology.

The use of medical terminology software is now a reality, with the leading vendors such as Epic and Cerner deploying their solutions in hospitals and other health-care institutions. These solutions are used for clinical documentation, billing and interoperability between different information systems. The need for effective telemedicine is also a trend that is driving the use of medical terminology software. Artificial intelligence and natural language processing are also driving the evolution of this market, enabling more sophisticated data analysis and ensuring that medical coding is done more accurately.

Future Outlook

From 2025 to 2034, the Medical Terminology Software Market is expected to increase from $67 million to $3.25 billion, with a robust compound annual growth rate (CAGR) of 8.9 percent. The growth of this market is mainly driven by the rising adoption of EHRs and the need for a standardized medical terminology in different healthcare systems. Moreover, as the demand for interoperability and data accuracy increases, the demand for advanced medical terminology software solutions is expected to grow, which will ultimately lead to enhanced patient care and operational efficiency.

The development of artificial intelligence and natural language processing are expected to have a significant impact on the medical terminology software market. These two areas of development will provide more intuitive and more efficient solutions and will facilitate the integration of medical terminology with existing health information systems. The growing trend towards telemedicine and remote patient monitoring, accelerated by the pandemic of COVID-09, is expected to further increase the need for comprehensive medical terminology solutions that can support various models of care. By 2034, it is expected that more than 70 percent of hospitals will use advanced medical terminology solutions, confirming their importance in the changing face of medicine.

The growing importance of personalized medicine and the integration of big data into the medical field will also help to expand the market. The demand for medical terminology interpretation and processing software will also increase as medical practitioners seek to make the most of data for clinical decision-making. Also, regulatory initiatives aimed at improving data standards will also support the growth of the market. In general, the medical terminology software market will grow at a fast pace, driven by the burgeoning needs of the medical industry and technological advancements.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Market Size Value In 2022 | USD 0.4 Billion |

| Market Size Value In 2023 | USD 0.47 Billion |

| Growth Rate | 19.20% (2023-2032) |

Medical Terminology Software Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.