Low Migration Inks Size

Market Size Snapshot

| Year | Value |

|---|---|

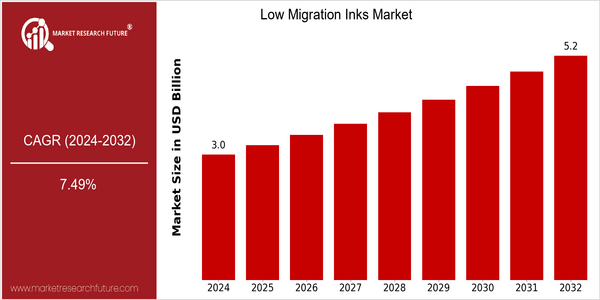

| 2024 | USD 2.95 Billion |

| 2032 | USD 5.25 Billion |

| CAGR (2024-2032) | 7.49 % |

Note – Market size depicts the revenue generated over the financial year

Low-migration inks market is set to grow at a CAGR of 5.2% between 2024 and 2032. During the forecast period, the market is expected to reach a value of $1.1 billion. The rising demand for low-migration inks is primarily driven by the growing concern for food safety and regulatory compliance in packaging applications, especially in the food and beverage industry. Since the migration of ink into consumables is a matter of concern for manufacturers, the use of low-migration inks is becoming an important part of packaging strategies. The advancements in ink formulation and printing processes are also boosting the market growth. The development of bio-based inks and the improvement in printing technology are enabling companies to achieve high-quality prints while meeting the strictest of safety standards. In addition, the rising R&D spending by market players such as Sun Chem, Siegwerk, and DIC, is resulting in the development of new low-migration ink formulations. These players are also enhancing their market positions through strategic collaborations and acquisitions.

Regional Market Size

Regional Deep Dive

The low migration inks market is growing at a significant rate in different regions. The growing consumer awareness of food safety and the stringent regulations on packaging materials are the major factors driving the growth of this market. In North America and Europe, the demand for low migration inks is very high due to the increasing demand for sustainable packaging solutions and the need to comply with the food safety standards. Meanwhile, the rapid industrialization and development of the packaging industry in the Asia-Pacific region will drive the market growth. Each region has its own characteristics influenced by local regulations, cultural preferences, and economic conditions, which will affect the future development of low migration inks.

Europe

- The European Union's Green Deal and the Circular Economy Action Plan are pushing for sustainable packaging solutions, leading to increased demand for low migration inks that align with these initiatives.

- Companies such as Flint Group and Siegwerk are actively collaborating with packaging manufacturers to create inks that not only meet regulatory standards but also reduce environmental impact.

Asia Pacific

- Rapid urbanization and a growing middle class in countries like China and India are driving demand for packaged goods, thereby increasing the need for low migration inks in food and beverage packaging.

- Local companies are beginning to adopt advanced printing technologies, such as digital printing, which often utilize low migration inks to enhance print quality and safety.

Latin America

- In Brazil, the National Health Surveillance Agency (ANVISA) is tightening regulations on food packaging, which is driving the adoption of low migration inks among local manufacturers.

- Emerging companies in the region are beginning to recognize the importance of sustainable packaging, leading to increased investments in low migration ink technologies.

North America

- The FDA has implemented stricter regulations regarding food packaging, prompting manufacturers to adopt low migration inks to ensure compliance and enhance consumer safety.

- Key players like Sun Chemical and INX International are investing in R&D to develop innovative low migration ink solutions, which are expected to drive market growth and meet the evolving needs of the packaging industry.

Middle East And Africa

- The region is witnessing a rise in food safety regulations, particularly in the Gulf Cooperation Council (GCC) countries, which is leading to a greater emphasis on low migration inks in food packaging.

- Companies like DIC Corporation are expanding their operations in the MEA region, focusing on developing low migration ink solutions tailored to local market needs.

Did You Know?

“Low migration inks are formulated to minimize the transfer of ink components to food products, making them essential for safe food packaging.” — European Printing Ink Association (EuPIA)

Segmental Market Size

The Low-Migration Inks Market is a vital part of the label and packaging industries, especially in the food and pharmaceuticals sectors where safety and compliance are of the utmost importance. This market is currently experiencing growth, as a result of an increased consumer awareness of food safety and stringent regulations aimed at reducing chemical migration from packaging materials. Sun Chem and Flint Group are at the forefront of this market, developing and supplying low-migration ink solutions that meet these demands. Adoption of low-migration inks is already widespread, especially in Europe and North America where regulations such as the European Union’s (EU) Framework Regulation on Food Contact Materials are already in place. The main applications include flexible packaging, labels and cartons, especially in the food and beverage industry, where companies such as Coca-Cola and Nestlé place a high priority on food safety. Moreover, the growing trend for sustainable and eco-friendly packaging solutions is driving the market as companies seek to comply with safety regulations and meet their green goals. Lastly, newer printing methods such as digital and UV-curing are also enhancing efficiency and reducing waste.

Future Outlook

The Low Migration Inks Market is set for substantial growth from 2024 to 2032, with a projected CAGR of 7.49% from $2.95 billion to $5.25 billion. This growth is primarily driven by the rising demand for food safety and regulatory compliance in packaging applications, with consumers and manufacturers putting greater emphasis on safety standards. Industry-wide adoption of low migration inks is expected to increase in the near future, especially in the food and beverage sector. By 2030, it is projected that over 60% of food and beverage packaging will use low migration inks. Meanwhile, technological advancements will also play a crucial role in shaping the future of the low migration inks market. In particular, innovations in ink formulations and printing processes will further enhance the performance and versatility of low migration inks, opening up new applications in the pharmaceutical and cosmetics industries. Moreover, new regulations and policies aimed at reducing the toxic exposure in consumer products will drive the adoption of low migration inks. The growing emphasis on sustainability will also spur the development of inks that use sustainable and eco-friendly materials, in line with the increasing efforts to reduce the impact on the environment. The low migration inks market is set to grow substantially, with a combination of regulatory, technological, and consumer trends putting safety and the environment at the forefront.

Leave a Comment