Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

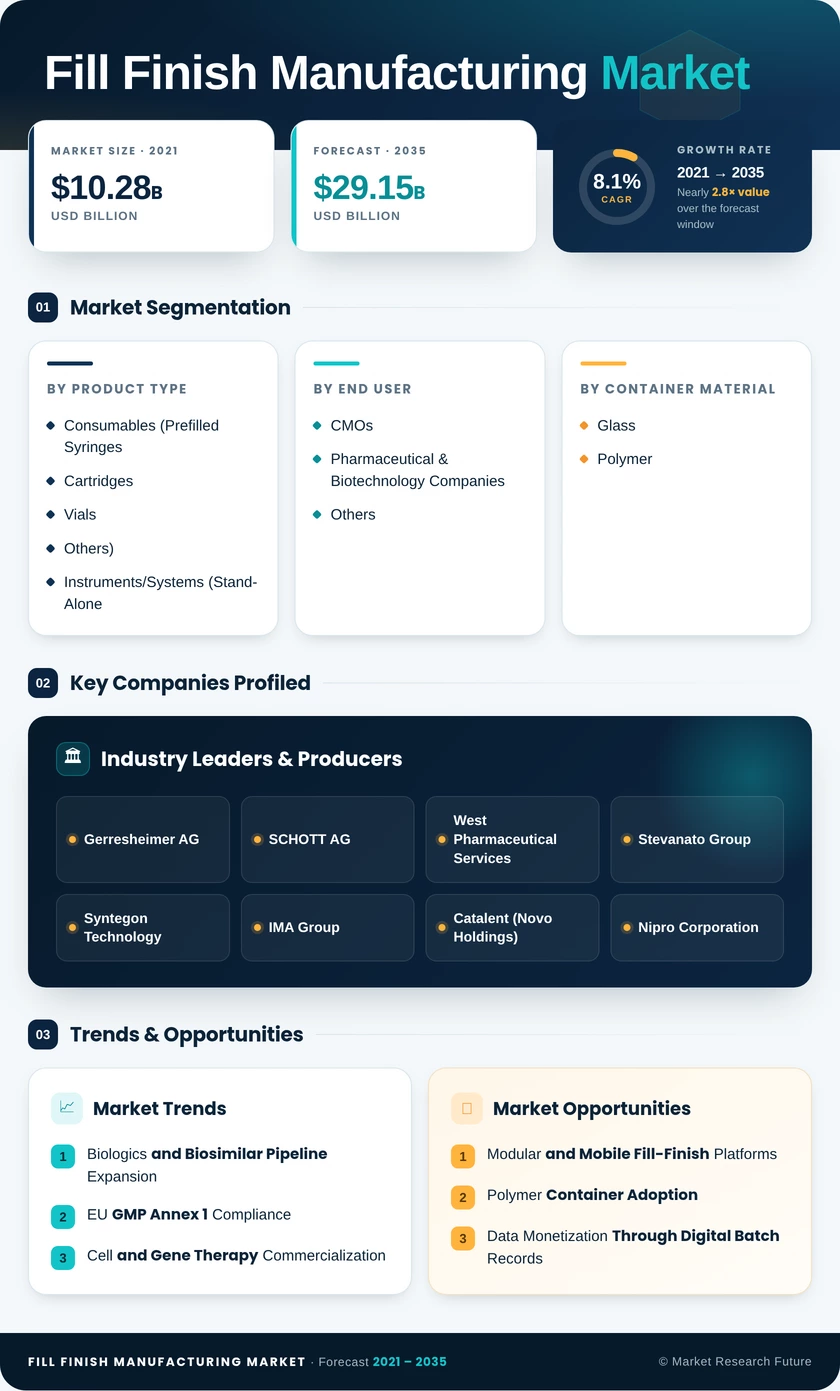

| Product Type | Consumables (Prefilled Syringes, Cartridges, Vials, Others); Instruments/Systems (Stand-Alone, Integrated, Automated, Semi-Automated/Manual) | Consumables | Instruments/Systems |

| End User | CMOs; Pharmaceutical & Biotechnology Companies; Others | Pharmaceutical & Biotechnology Companies | CMOs |

| Container Material | Glass; Polymer | Glass | Polymer |

| Geography | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Prefilled Syringes | Rising self-administration demand for biologics in autoimmune and metabolic indications |

| Cartridges | Growth in pen-injector platforms for GLP-1 agonists and insulin analogs |

| Vials | Continued dominance in hospital-administered injectables and lyophilized products |

| Other Consumables | Nested tubs, stoppers, seals, and RTU components are gaining standardization. |

| Stand-Alone Systems | Suited for low-volume, high-flexibility clinical filling |

| Integrated Systems | End-to-end line configurations reduce manual handoffs. |

| Automated Systems | High-speed robotic filling for commercial-scale biologics |

| Semi-Automated/Manual | Legacy systems still prevalent in emerging-market facilities |

Consumables represent the volume backbone of the market, with prefilled syringes emerging as the highest-growth sub-segment as patient-centric drug delivery gains momentum across therapeutic areas. Instruments and systems investment is accelerating as manufacturers pursue fully automated, isolator-based platforms.

By End User

| Sub-Segment | Key Trend |

| Contract Manufacturing Organizations | Rapid capacity build-out to absorb outsourced biologics and cell therapy programs |

| Pharmaceutical & Biotechnology Companies | Captive filling operations for blockbuster products; selective outsourcing for pipeline candidates |

| Others | Academic medical centers, government vaccine manufacturers, and specialty compounders |

Pharmaceutical and biotechnology companies maintain the largest share, but the outsourcing trend toward CDMOs is reshaping competitive dynamics as innovator firms prioritize asset-light business models for early-phase programs.

By Container Material

| Sub-Segment | Key Trend |

| Glass | Regulatory precedent and chemical inertness sustain dominance; supply concentration is a vulnerability. |

| Polymer | COP/COC formats are gaining traction for biologics stability, breakage elimination, and sustainability goals |

Glass containers remain the industry default, but the transition toward polymer alternatives is accelerating as drug-product compatibility studies and regulatory filings increasingly support non-glass primary packaging.

By Geography

| Sub-Segment | Key Trend |

| North America | Dense CDMO corridor, Biosecure Act reshoring, FDA biologics pipeline |

| Europe | Annex 1 compliance upgrade cycle, biosimilar contract filling, equipment OEM cluster |

| Asia-Pacific | Government-backed capacity build-out, vaccine self-sufficiency, CDMO scale-up |

| South America | Technology transfer programs, domestic production mandates |

| Middle East & Africa | WHO prequalification pathways, pandemic preparedness infrastructure |

Regional growth patterns reflect divergent investment drivers: mature markets are upgrading existing capacity for compliance and automation, while emerging regions are building new sterile filling infrastructure from the ground up.