Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Automotive Night Vision System Market Type | Far Infrared (LWIR), Near Infrared (NIR), Short-Wave Infrared (SWIR) | Far Infrared (LWIR) | Short-Wave Infrared (SWIR) |

| Display Type | Head-Up Display, Instrument Cluster, Central Infotainment Screen, Navigation System | Head-Up Display | Central Infotainment Screen |

| Component Type | Night Vision Cameras, IR Illumination Sources, Image Processing ECUs, Display Modules | Night Vision Cameras | IR Illumination Sources |

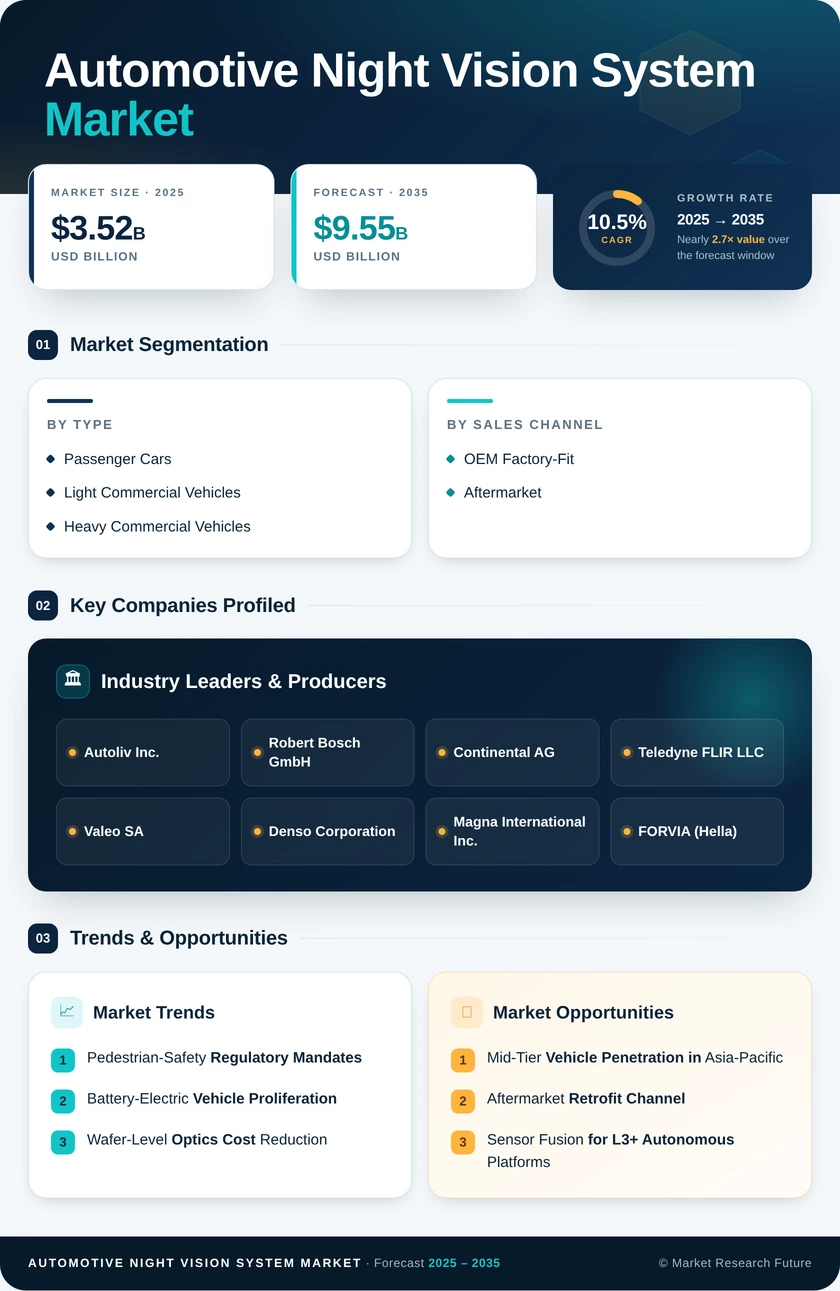

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles | Passenger Cars | Light Commercial Vehicles |

| Sales Channel | OEM Factory-Fit, Aftermarket | OEM Factory-Fit | Aftermarket |

Market Segmentation Overview

By Automotive Night Vision System Market Type

| Sub-Segment | Key Trend |

| Far Infrared (LWIR) | Passive thermal detection; dominant share due to no active illumination requirement |

| Near Infrared (NIR) | Cost-effective LED/laser-illuminated systems for mid-tier vehicles |

| Short-Wave Infrared (SWIR) | Gallium arsenide sensor advances enabling material discrimination and fog penetration |

Far Infrared technology remains the backbone of the Automotive Night Vision System Market, owing to its fully passive operation mode that detects emitted body heat. Short-Wave Infrared is gaining traction in R&D pipelines as next-generation platforms demand multi-spectral classification capabilities for autonomous driving perception stacks.

By Display Type

| Sub-Segment | Key Trend |

| Head-Up Display (HUD) | Augmented-reality windshield overlay minimizes driver distraction |

| Instrument Cluster | Legacy pathway leveraging existing digital cluster real estate |

| Central Infotainment Screen | Growing with large-format BEV cockpit display architectures |

| Navigation System | Budget integration option using the existing navigation screen |

Head-Up Displays lead adoption because they project thermal imagery into the driver's forward field of view. Central Infotainment Screens are rapidly gaining share as automakers consolidate cockpit functions onto single large-format displays in electric vehicle platforms.

By Component Type

| Sub-Segment | Key Trend |

| Night Vision Cameras | Core hardware integrating a microbolometer array and germanium optics |

| IR Illumination Sources | Growing alongside active NIR system deployments |

| Image Processing ECUs | AI classifier demand driving compute-module upgrades |

| Display Modules | Tied to HUD and infotainment integration trends |

Night Vision Cameras represent the highest-value component per unit. IR Illumination Sources are the fastest-growing component category, propelled by the expansion of active Near Infrared system architectures in cost-sensitive vehicle segments.

By Vehicle Type

| Sub-Segment | Key Trend |

| Passenger Cars | Regulatory mandates and consumer safety expectations drive the dominant share |

| Light Commercial Vehicles | Fleet operator safety mandates accelerating adoption |

| Heavy Commercial Vehicles | Long-haul night driving and cargo-carrier safety needs |

Passenger Cars dominate in volume, while Light Commercial Vehicles represent the fastest-growing category as fleet procurement policies increasingly require advanced nighttime safety features to reduce liability and insurance costs.

By Sales Channel

| Sub-Segment | Key Trend |

| OEM Factory-Fit | Regulatory compliance drives factory-level integration as standard or an option |

| Aftermarket | Retrofit demand is growing in markets with a large aging vehicle parc |

OEM Factory-Fit installations account for the vast majority of revenue because regulatory mandates apply at the manufacturing stage. The Aftermarket channel is expanding as plug-and-play retrofit kits become available at lower price points for vehicles not originally equipped with thermal night-vision capability.