Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

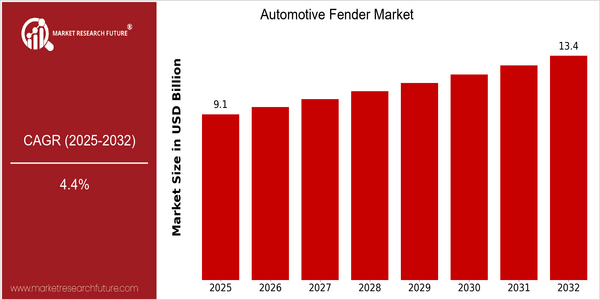

Market Size Snapshot

| Year | Value |

|---|---|

| 2025 | USD 9.08 Billion |

| 2032 | USD 13.36 Billion |

| CAGR (2023-2032) | 4.4 % |

Note – Market size depicts the revenue generated over the financial year

The global market for automobile fenders is set to grow at a significant pace, with a current market size projected at $ 9 billion in 2025, and is expected to increase to $ 13.36 billion by 2032. The CAGR (compound annual growth rate) from 2023 to 2032 is 4.4%. The increasing production of vehicles, especially in emerging economies, as well as the rising demand for lightweight and durable materials, are the key drivers of the market. In addition, the adoption of advanced manufacturing technology and the use of new materials are expected to enhance the production efficiency and performance of fenders, which will also boost the market growth. Companies such as Magna, BASF and other fender manufacturers are actively involved in this growth. They have established cooperative relationships to develop advanced materials and sustainable production methods, and are investing in research and development to improve their product offerings. The emergence of electric vehicles has prompted manufacturers to explore fender designs that can accommodate new technologies while maintaining aesthetics. This trend will continue, and the fender market will be closely related to the development of the automotive industry.

Regional Market Size

Regional Deep Dive

The market for fenders for automobiles is growing at a rapid rate. It is mainly due to the increase in automobile production, the increased use of lightweight materials and the changes in car design. The local characteristics are influenced by the local manufacturing, the local legislation and the local preferences. North America is characterized by a strong presence of the major automobile manufacturers and a shift towards electric cars. Europe is characterized by a focus on the environment and innovation in materials. Asia-Pacific is characterized by rapid industrialization and urbanization, which increases the demand for cars. The Middle East and Africa are slowly developing their car industry, while Latin America is focusing on low-cost manufacturing solutions for local markets.

Europe

- European car makers have begun to adopt a policy of conservation, and the Green Deal of the European Union has stimulated the use of more environment-friendly materials in the manufacture of cars, including the bodywork. Now companies like Volkswagen and BMW are investing in research into biodegradable composites.

- In Europe, the growing importance of electric cars is influencing the shape of the fenders, since manufacturers are trying to optimize aerodynamics and reduce weight. Government subsidies for the production and use of electric vehicles are encouraging innovation in the automobile industry.

Asia Pacific

- A great increase in the manufacture of motor cars is taking place in the countries of the Far East, especially in China and India, which are becoming important centres of fender production. The local companies BYD and Tata Motors are expanding their factories to meet the increasing domestic and foreign demand.

- Technological advancements in manufacturing processes, such as 3D printing and automation, are being adopted by Asian manufacturers to enhance efficiency and reduce costs in fender production, allowing for more customized solutions.

Latin America

- Cost-effective production is the focus in Latin America. Brazil and Mexico, with their low labor costs and advantageous trade relations, are becoming a very attractive location for the automobile industry. This is encouraging local companies to invest in the manufacture of car fenders.

- The region is also seeing a rise in demand for electric vehicles, driven by government incentives and consumer interest in sustainable transportation, prompting manufacturers to adapt their fender designs to accommodate new technologies.

North America

- The Canadian and American automobile industries are increasingly using such advanced materials as aluminum and carbon fibre in the production of their fenders, because of the increasing need to reduce weight in order to improve fuel economy and reduce emissions. These materials are used in the fenders of the Ford and General Motors cars.

- Moreover, the stricter emissions standards imposed by the EPA are putting the brakes on the development of fender designs and materials. As a result, the use of sustainable and recyclable materials is gaining ground.

Middle East And Africa

- The car market in Africa and the Middle East is gradually developing. South Africa and the United Arab Emirates are investing in their own car industries. The South African Automotive Master Plan aims at the local production of car components, including bodywork.

- Government programs promoting local assembly and manufacturing are encouraging international automotive companies to establish operations in the region, leading to increased competition and innovation in fender design and production.

Did You Know?

“Did you know that the automotive fender market is increasingly integrating smart technologies, such as sensors and cameras, to enhance vehicle safety and performance?” — Automotive News

Segmental Market Size

The fender market is an important segment of the automobile industry, and is currently experiencing strong growth due to increased production and increased demand for aesthetic and practical improvements. The fender market is driven by the growing trend towards personalization and the use of lightweight materials to improve fuel efficiency. Regulations aimed at improving safety and reducing emissions are also driving demand for advanced fender designs. The market is currently at a mature stage of development. Leading companies like Toyota and Ford are introducing fender designs that make use of new materials like high-strength steel and carbon fiber. The most important applications are for passenger cars, commercial vehicles and electric vehicles, where fenders play an important role in both protection and aerodynamics. Fenders are also used in buses and trucks. The trend towards sustainable mobility and the growing importance of electric vehicles is driving demand for lightweight fenders that improve performance and fuel efficiency. Moreover, new production methods like 3D printing and automation are enabling more efficient production and more personalization.

Future Outlook

The Automotive Fenders Market is expected to increase at a CAGR of 4.4% between 2025 and 2032, from $ 9 billion to $13.36 billion. This growth is driven by the rising demand for lightweight and durable materials in the manufacturing of cars, as a result of the industry's continuous efforts to improve fuel economy and reduce emissions. Fenders are expected to benefit from the increased use of advanced materials such as carbon fiber and high-strength steel, which will result in improved performance and greater appeal to both car manufacturers and consumers. Also, the development of smart materials and the use of additive manufacturing processes will have a major impact on the future of the fender market. Also, the emergence of regulations aimed at reducing vehicle emissions and promoting electric vehicles (EVs) will also boost market growth. Consequently, the need for fender designs that accommodate the new architectures of the EVs will be greater. Also, the emergence of trends such as personalization and aesthetics will play a major role, as consumers increasingly demand personalization of the vehicle. The fender market will thus experience a significant evolution, driven by technological innovations and changing consumer preferences, and is expected to grow at a strong pace between 2025 and 2032.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Market Size Value In 2022 | USD 8.65 Billion |

| Market Size Value In 2023 | USD 9.08 Billion |

| Growth Rate | 4.40% (2023-2032) |

Automotive Fender Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.