글로벌 의료 미학 시장 개요

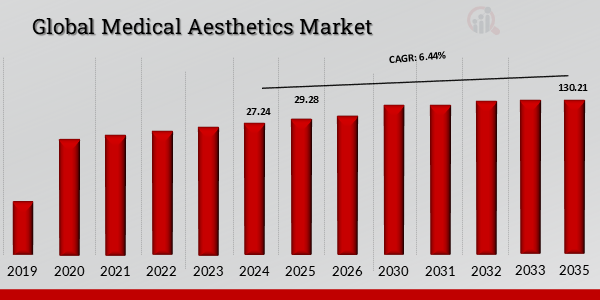

2024년 의료 미학 시장 규모는 272억 4천만 달러로 평가되었습니다. 글로벌 의료 미학 산업은 2025년 292억 8천만 달러에서 2035년까지 1,302억 1천만 달러로 성장할 것으로 예상되며, 예측 기간(2025~2035년) 동안 6.44%의 연평균 성장률(CAGR)을 보일 것으로 예상됩니다.

전 세계적으로 비만 및 노인 인구의 증가, 미용 및 미용 시술에 대한 수요 증가, 미용 수술에 대한 지출 증가 및 미적 산업의 기술 발전이 글로벌 의료 미학 시장을 주도하고 있습니다.

MRFR의 분석가에 따르면 "글로벌 의료 미학 시장은 주로 전 세계 비만 및 노인 인구의 증가, 미용 및 미용 시술에 대한 수요 증가, 미용 수술에 대한 지출 증가, 미학 산업의 기술 발전, 의료 관광 산업 성장에 의해 주도되고 있습니다."

출처: 2차 연구, 1차 연구, MRFR 데이터베이스 및 분석가 검토

메디컬 에스테틱 시장 동향

신흥 경제에서 화장품 시술 채택 증가

신흥 경제에서는 유방 확대, 지방 흡입 수술, 눈꺼풀 수술, 복부 성형술, 보툴리눔 독소, 비수술 지방 감소, 화학적 필링 등과 같은 미용 시술 채택이 증가했습니다. 이는 미용 시술의 인기가 높아지고 가처분 소득이 증가한 데 따른 것입니다. 또한 신흥 경제국의 의료 인프라 개선은 시장 성장을 더욱 촉진합니다.

또한, 신흥 경제국에서 성형외과 의사 수가 증가하면서 상당한 성장 기회가 제공될 것으로 예상됩니다. 예를 들어, ISAPS에 따르면 성형외과 의사 수 추정 기준 상위 30개 국가 목록에는 인도, 아르헨티나, 베네수엘라, 태국, 사우디아라비아 등 여러 신흥 국가가 포함되어 있습니다. 또한, 최소 침습적 미용 시술의 증가는 시장 성장 기회를 더욱 제공합니다.

ISAPS에 따르면 인도는 2019년 전체 수술 건수 약 394,728건, 비수술 시술 건수 약 249,024건을 기록했다. 마찬가지로 아르헨티나도 2019년 전체 수술 건수 약 193,237건, 비외과적 시술 건수 약 232,584건을 기록했다. 이에 따라 신흥국의 미용 시술 도입 증가로 의료 에스테틱 시장도 크게 성장할 것으로 예상된다.

의료 미학 시장 부문 통찰력

글로벌의료미학 제품 통찰력

기술의 발전으로 인해 피부 탄력 강화, 피부 재생 및 재생, 문신 제거, 신체 윤곽 형성 등 의료 미적 시술에 대한 옵션이 생겨났습니다. 글로벌 메디컬 에스테틱 시장은 제품을 기준으로 얼굴 에스테틱, 체형 윤곽 성형 기기, 미용 임플란트, 제모 기기, 피부 에스테틱 기기, 문신 제거 기기 등으로 구분됩니다.

안면 미용 부문은 안면 미용 시술 횟수의 증가로 인해 2020년에 7조 5,118억 2천만 달러로 가장 높은 시장 가치를 보유하고 있습니다. 히알루론산 주사는 피부를 젊고 건강하게 유지하는데 도움을 줍니다. 이에 히알루론산 주사 시술이 늘어나고 있다. 예를 들어 미국성형외과학회에 따르면 2020년 미국에서 시행된 총 히알루론산 주사 시술 건수는 2,619,650건, 2019년에는 2,878,201건이었다.

신체 윤곽술 장치 부문은 비침습적 신체 윤곽술 시술의 채택 증가로 인해 CAGR 6.82%로 가장 빠르게 성장하는 부문이 될 것으로 예상됩니다. 예를 들어, 미국 미용성형외과학회에 따르면 셀룰라이트를 치료하는 가장 유망한 방법 중 하나는 레이저 치료를 통한 것이며, 이로 인해 향후 몇 년 동안 체형 성형 및 피부 탄력 강화 시술이 증가할 것으로 예상됩니다.

글로벌 의료 미학 기술 통찰력

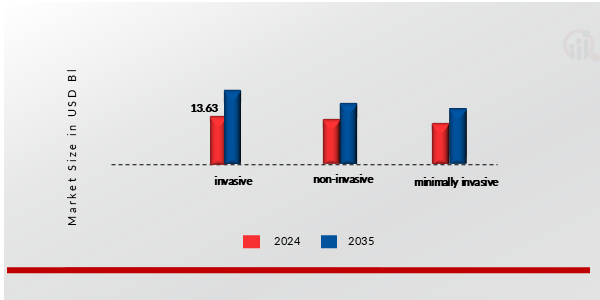

의료 미용 시장은 기술을 기반으로 침습적, 비침습적, 최소 침습적 방식으로 분류됩니다. 침습적 시술은 의료 시술을 수행하기 위해 신체 부위를 절개해야 하는 수술입니다. 코성형, 안면지방흡입, 안면거상술, 가슴성형, 바디리프팅, 허벅지 리프트, 볼·턱 보형물 등이 침습적 시술에 해당하는 주요 시술이다. 미국성형외과학회에 따르면, 미국에서 2020년 코성형 시술 건수는 352,555건으로 집계됐다.

비침습적 시술은 빠른 시술이고, 합병증의 위험이 적으며, 미용 시술에서 비용 효과적인 치료법입니다. 주요 시술로는 비침습적 안면 필러, 레이저 제모, 화학적 박피술, 박피술 등이 있습니다.

최소침습수술은 내시경을 이용하여 시행됩니다. 내시경은 외과 의사가 피부를 크게 절개할 필요 없이 작은 구멍을 통해 수술을 수행하는 데 도움이 됩니다. 눈성형수술, 레이저수술, 안면거상술은 최소침습수술을 통해 진행되는 대표적인 수술이다. 예를 들어, 미국성형외과학회에 따르면, 미국에서 2020년 최소 침습 미용 시술 건수는 13,281,235건이었습니다.

그림 1: 글로벌 의료 미용 시장, BY기술, 2024년 및 2035년(10억 달러)

글로벌 의료 미학 최종 사용 산업 통찰력

최종 사용자를 기준으로 글로벌 메디컬 에스테틱 시장은 병원, 진료소, 피부과, 미용 센터 등으로 분류됩니다. 피부질환 환자 증가와 화장품 지출 증가로 인해 병의원이 가장 큰 시장 점유율을 차지하고 있다. 호주 미용 의사 대학(Cosmetic Physicians College of Australia)에 따르면 호주 시민들은 매년 미용 시술에 약 10억 달러를 지출합니다. 병원과 진료소에서는 흉터 치료, 튼살 치료 등과 같은 다양한 피부 상태를 치료하기 위해 점점 더 새롭고 진보된 기술을 채택하고 있습니다. 이 기술은 피부 상부층을 연마하여 피부에 활력을 불어넣는 기술을 기반으로 합니다.

1인당 국민소득 증가와 생활방식 변화로 인해 화장품 비용이 지속적으로 증가하고 있습니다. 피부과 및 미용 센터는 광손상, 여드름, 과다색소침착 등 다양한 피부 질환으로 고통받는 환자들을 위한 첫 번째 진료 지점입니다. 피부 관리 서비스에 대한 수요가 증가함에 따라 피부과 및 미용 센터의 수가 증가하고 있습니다. 2019년 미국피부외과학회(American Society for Dermatologic Surgery)도 103억 건 이상의 미용 치료를 수행했는데, 이는 2018년에 비해 14% 증가한 수치입니다. 따라서 예측 기간 동안 이 부문에서 창출된 수익은 증가할 가능성이 높습니다. 최소 침습적 치료, 미용 시술의 채택 증가는 글로벌 시장 성장을 강화하는 주요 요인입니다. 다른 부분은 미용실과 스파로 구성되어 있습니다.

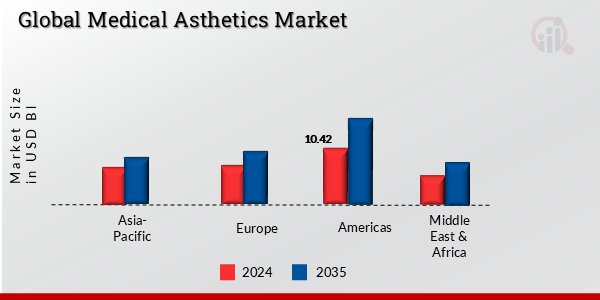

글로벌 의료 미학 지역 통찰력

의료 미학 시장에 대한 보고서는 미주, 유럽, 아시아 태평양, 중동 및 아프리카 등 지역을 기준으로 분류되었습니다. 미주 의료 미학 시장은 2024년 가장 큰 시장 점유율을 차지했으며, 아시아 태평양 지역은 연구 기간 동안 상당한 CAGR 성장을 보일 것으로 예상됩니다. 미주 지역의 글로벌 메디컬 에스테틱 시장은 북미와 라틴 아메리카로 구분됩니다. 이 지역에서는 북미가 시장을 장악할 것으로 예상된다. 미주 지역은 잘 발달된 의료 부문, 미용 치료 및 기타 노화 방지 관련 미용 시술에 대한 수요 증가, 선두 업체로 인해 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

또한, 미용 수술의 증가는 이들 국가의 의료 미용 시장의 성장을 주도할 가능성이 높습니다. 미국성형외과학회(American Society of Plastic Surgeons)에 따르면 2020년 미국에서 156억 건의 미용 시술이 수행되었습니다. 또한 안면 회춘 시술은 계속해서 성장을 경험하고 있습니다. 2020년과 2019년에는 각각 44억 건과 51억 건이 넘는 보툴리눔 독소 A형 주사로 현재까지 가장 높은 보툴리눔 독소 A형 주사 건수를 기록했습니다. 또한, 비침습적 지방 감소 및 피부 타이트닝 시술이 환자들 사이에서 인기를 얻고 있습니다. 예를 들어, 미국성형외과학회에 따르면 2020년 미국에서 비수술적 피부 타이트닝 시술 건수는 188,509건이었습니다. 더욱이, 이 지역에 눈에 띄는 많은 플레이어의 존재는 미주 시장의 주요 원동력입니다.

아시아 태평양 지역은 글로벌 메디컬 에스테틱 시장에서 가장 빠르게 성장하는 시장입니다. 거대한 환자 인구의 존재, 기술의 급속한 발전, 시장 발전을 위한 엄청난 기회가 아시아 태평양 지역 의료 미용 시장의 성장을 주도하고 있습니다. 이 지역 정부는 또한 시민들의 삶의 질을 향상시키기 위해 선진국의 더 나은 치료 옵션을 활용하기를 기대하고 있습니다. 또한, 얼굴 미학에 대한 수용이 증가함에 따라 이 지역의 의료 미학 시장이 활성화되고 있습니다.

아시아 개발 은행에 따르면 아시아의 노인 인구는 2050년까지 약 9,230억 명에 이를 것으로 예상됩니다. 인도, 중국, 일본이 시장의 주요 기여자입니다. 따라서 미용 시술의 높은 비용과 인식 부족으로 인해 시장 성장이 둔화될 수 있습니다. 아시아 태평양은 주로 일본, 중국, 인도, 대한민국 및 호주와 같은 국가로 구성됩니다. 또한, 국제미용성형외과학회에 따르면 2019년 인도에서는 약 79,248건의 지방흡입 시술이 이루어졌습니다.

그림 2: 지역별 글로벌 의료 미용 시장, 2024년 및 2035년(10억 달러)

또한 시장 보고서에서 연구된 주요 국가는 미국, 캐나다, 멕시코, 독일, 프랑스, 이탈리아, 영국, 스페인, 일본, UAE, 남아프리카, 사우디 아라비아, 아르헨티나 및 브라질입니다.

글로벌 의료 미학 주요 시장 참가자 및 경쟁 통찰력

많은 글로벌, 지역 및 현지 공급업체가 의료 미학 시장의 특징을 나타냅니다. 시장은 경쟁이 치열하며 모든 플레이어가 시장 점유율을 얻기 위해 경쟁합니다. 치열한 경쟁, 급속한 기술 발전, 정부 정책의 빈번한 변화, 환경 규제 등이 시장 성장에 직면하는 핵심 요소입니다. 공급업체는 비용, 제품 품질, 신뢰성 및 정부 규정을 기반으로 경쟁합니다. 공급업체는 경쟁이 치열한 시장에서 생존하고 성공하려면 비용 효율적인 고품질 제품을 제공해야 합니다.

시장의 주요 업체로는 ALLERGAN PLC, MERZ PHARMA GMBH & CO. KGAA, LUMENIS, HOLOGIC INC, GALDERMA SA, BAUSCH HEALTH(VALEANT PHARMACEUTICALS), ANIKA THERAPEUTICS INC., CUTERA, ALMA LASERS, SYNERON MEDICAL LTD 등이 있습니다. 의료 미학 시장은 경쟁 증가, 인수, 합병, 기타 전략적 시장 개발 및 운영 효율성 개선을 위한 결정으로 인해 통합된 시장입니다.

의료 미학 시장의 주요 회사는 다음과 같습니다

- 앨러간 PLC

- 메르츠 파마 GMBH & CO. KGAA

- 루메니스

- 홀로직(주)

- 갈더마 SA

- BAUSCH HEALTH(밸리언트 파마슈티컬즈)

- 아니카 테라퓨틱스(주)

- 큐테라

- 알마 레이저

- SYNERON MEDICAL LTD

의료 미학 시장 세분화

제품별 의료 미학 시장(10억 달러, 2019-2035)

- 얼굴 미학

- 신체 윤곽 장치

- 비수술적 지방 감소 장치

- 셀룰라이트 감소 장치

- 지방흡입 기기

- 미용 임플란트

- 제모 장치

- 피부미용기기

- 레이저 피부 재포장 장치

- 비수술적 피부 강화 장치

- 마이크로니들링 제품

- 가벼운 치료 장치

- 화학적 껍질

- 피부 미백제

- 미적 스레드

- 문신 제거 장치

- 기타

기술 전망별 의료 미학 시장(10억 달러, 2019-2035)

최종 용도 전망별 의료 미학 시장(10억 달러, 2019-2035)

글로벌의료미학지역 전망

- 미주 의료

- 북아메리카

- 라틴 아메리카

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아 제국

- 스페인

- 유럽의 나머지 지역

- 아시아 태평양

- 중국

- 일본

- 대한민국

- 인도

- 호주

- 대만

- 아시아 태평양 지역

- 중동 및 아프리카