The global demand for copper semis is expected to grow at approx. 2-4 percent CAGR through 2022–2024.The electronics, transportation (especially EV), and construction sectors are the major growth drivers.

Copper and Copper Semis Market Outlook

World’s (excl-China) refined usage is estimated to have increased by about 8.5 percent in 2021, Chinese apparent usage declined by 3.8 percent, partially offsetting the usage growth in other regions of the world. Also, Global copper smelting activity decreased by 3% M-o-M in Oct-22 to 47.5

Globally, the end-use demand for copper cathodes is primarily from the wire rods market. This constituted to approximately 68 percent, followed by copper tube products that contributed to 12 percent

The global copper wire demand rebounded in second half of 2020, led by China, where economic activity resumed. The nature of the market is highly fragmented, and the ability of suppliers varies, based on the size of the wire, quality of copper, and the facilities available for production

Both global supply and demand of copper plates, sheets, and strips increased in 2021, as the market resumed activity by the end of 2020, especially in China. Demand from electronics, telecommunication, and power witnessed a robust growth. The copper strips market witnessed an increase in demand in 2021, majorly led by industrial equipment and construction sector.

The global supply–demand for copper rods, bars, and sections reduced in 2020, due to COVID-19 outbreak. The primary end uses are telecommunication and power industries, where the billets procured are further processed to produce PCB copper wires or electric cables of higher diameters. Increase in electrification and expanding communication networks, especially across developing countries, will lead the growth

COVID-19, Russia-Ukraine, and Economic Headwinds Impact on Copper and Copper Semis

Volatile conditions due to Russia-Ukraine conflict, logistical constraints, IMF slashing forecast for global economic growth, re-emergence of Covid-19 in China, regulatory constraints in Chile and Peru have high chances of affecting global copper market.

Copper Pricing Insights

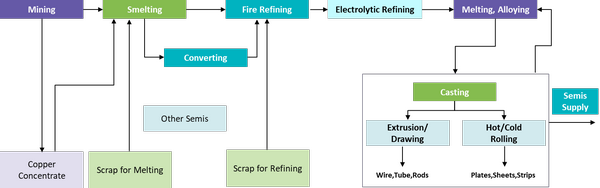

Production of copper semis depends primarily on the raw material from smelters and refiners. Most of the mining companies also have smelting and refinery facilities to supply end products as cathodes.

Comex prices decreased only slightly by 0.2 percent M-o-M in Oct-22 as tight supply counterbalanced weak demand. Scrap supplies to market tightened. USA manufacturing PMI fell to 49.9 in Oct-22 from 52 in Sept-22. LME prices decreased by 1.5 percent M-o-M in Oct-22, due to weakening downstream demand even as production costs remain high. Eurozone’s manufacturing PMI declined to 46.4 in Oct-22 from 48.4 in Sept-22. SHFE prices declined slightly by 0.1 percent in Oct-2022 as low demand was offset by reduction in smelting activities leading to tight supply. Caixin China General Manufacturing PMI increased slightly to 49.2 in Oct-22 from 48.1 in Sept-22.

Copper and Copper Semis Supply Outlook

Supply is expected to reduce, as energy costs are expected to impact production in Europe and North America. While in China, smelting rates shall remain low.

The countries are trying to bring supply chains closer to home, especially after pandemic, coupled with tariff regime and Chinese policies.

China is the leading producer, accounting for around 47 percent of global production, followed by Asia, excl. China (21 percent) and Europe (17 percent). Some of the major suppliers of wires include Aurubis, Jiangxi Copper, Jiangsu, Nexans, LS Group, etc.

Supply–demand witnessed a downtrend in 2020, on the account of COVID-19 outbreak as demand from building sector declined. Primary uses of copper tubes are in heating, ventilation, air conditioning and refrigeration systems, water distribution systems, etc.

Copper and Copper Semis Value Chain

Regional Market Insights

China is expected to have accounted for the largest share of the world’s copper semis production, holding nearly 48 percent of the global market share

Production declined in Europe in 2021, mainly due to decrease in production in Germany, Russia, Spain, owing to factors like maintenance work, operational issues etc. Recessionary risk, energy crisis, Ukraine war etc. are likely to affect copper production more than demand.

Supplier Intelligence

The category intelligence covers some of the key global and regional players such as Codelco, Jaingxi Copper, Freeport-McMoran, Mitsui, Aurubis, Groupo Mexico among others.

Key global players have announced to expand its manufacturing facilities in developing countries where there is high demand and scrap recycling rates are less. For instance, Aurubis building $320 million multimetal recycling plant in Georgia, USA will aid in sustainable growth and circular economy

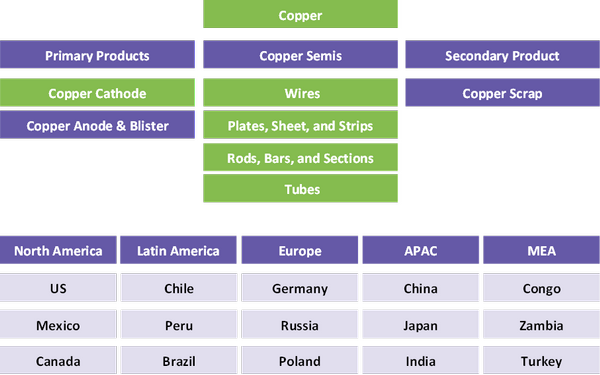

Segmentation Overview: