Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

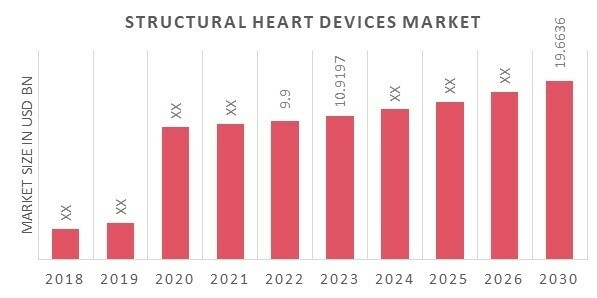

Global Structural Heart Devices Market Overview

The Structural Heart Devices Market Size was valued at USD 9.9 billion in 2022 and is projected to grow from USD 10.91 Billion in 2023 to USD 19.66 billion by 2030, exhibiting compound annual growth rate (CAGR) of 10.30% during the forecast period (2023 - 2030). Structural heart disorders and the demand for minimally invasive techniques are the key drivers enhancing market growth.

Source Secondary Research, Primary Research, MRFR Database, and Analyst Review

Structural Heart Devices Market Trends

- Rise in the frequency of structural heart diseases boost the market growth.

Heart devices include heart valve balloon occludes and annuloplasty rings. If the heart is oversized or has a leaky valve, these devices restructure and tighten the buzz around the heart. Owing to the increasing number of cardiovascular diseases ly, the demand for heart valve devices is growing, further expected to fuel market growth. The article published in June 2022 stated that heart valve surgery is a procedure to treat heart valve disease involving at least one of the four faulty heart valves. Heart valves keep blood flowing in the correct direction through the heart. Thus, the advantages of the devices are anticipated to fuel the Segment's growth.

Additionally, product approvals and new drug launches are the primary factors affecting the availability of a vast concentration of drugs in the market. This is expected to drive segment growth. For instance, in September 2021, Abbott received the Food and Drug Administration (FDA) approval for the company's Epic Plus and Epic Plus Supra Stented Tissue Valves to improve therapy options for people with aortic or mitral valve disease. With this new device, Abbott expanded its Epic surgical valve platform.

In addition, in August 2021, the First 'Made in India' 3-D printed heart valve was developed in Chennai. The new heart valves are designed using 3D printers, which can overcome the problems related to artificial heart valves. Thus, increasing developments are anticipated to drive segment growth over the forecast period. Therefore, a medical condition associated with cardiovascular diseases has recently enhanced the market CAGR of Structural Heart Devices across the globe.

However, there have been significant advances in treatment innovations to cater to the demand. The rising prevalence of cardiovascular diseases (CVDs) ly is another factor driving the growth of the Structural Heart Devices market revenue.

Structural Heart Devices Market Segment Insights

Structural Heart Devices Type Insights

The market segments of Structural Heart Devices, based on type, the segment is divided into Heart Valve Devices, Annuloplasty Rings, Occluders, Delivery Systems. Heart Valve Devices Sweeteners segment held the majority share in 2022concerning the Low-Intensity sweeteners market revenue. Due to its established reimbursement codes and therapeutic efficacy.

LAAC is predicted to be among the segments with the quickest growth in the upcoming years.The procedure's minimally invasive nature is crucial for developing the Structural Heart Devices market revenue.

May 2022Abbott and laboratories announced a distinctive minimally invasive vascular heart valve repair device. The company also revealed new data on two critical components of its market-leading structural heart portfolio, MitraClip, and Amplatzer Amulet.

In May 2022 Biometrics announced its expansion in Ireland with potential in Galway under the Balloons & Balloon Catheters Centre of Excellence.

Structural Heart Devicesby Indication Insights

The market segmentation of Structural Heart Devices has been segmented according to indication into valvular heart disease, cardiomyopathy, congenital heart abnormalities, and others. The two subtypes of valvular heart disease are regurgitation and stenosis. Hence, rising applications of the Segment for biological and tissue valves held a significant market share for structural cardiac devices worldwide. Over the anticipated period, the Segment is likely to dominate the market growth.

Figure 1 Structural Heart Devices Market, by Indication, 2022& 2030 (USD Billion)

Source Secondary Research, Primary Research, MRFR Database, and Analyst Review

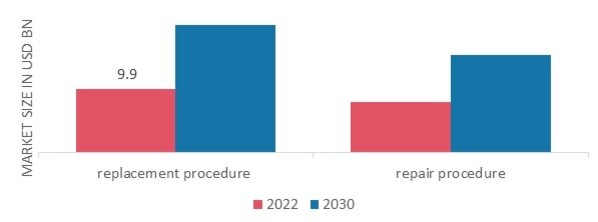

Structural Heart Devices By Procedure Insights

The Structural Heart Devices market data has been divided into six categories based on procedure is divided into two categories based on technique replacement process and repair procedure. Throughout the projected period, the replacement procedure segment is expected to account for a sizeable portion of the market due to the availability of cutting-edge technology, & cost-effective treatments.

In May 2022Philips launched EchoNavigator 4.0, the new release of its image-guided therapy solution for treating structural heart disease. EchoNavigator 4.0 gives users of Philips’ EPIQ CVXi interventional cardiology ultrasound system a control of live fusion-imaging on the company’s Image Guided Therapy System called “Azurion – platform.”

In February 2022Genesis MedTech Group (Genesis or Group) completed the acquisition of JC Medical (JCM). This structural heart company primarily designs and develops transcatheter valve replacement products for the minimally invasive treatment of structural heart diseases. J-Valve, developed by JCM, is the first and only in China to successfully develop and commercialize a minimally invasive TAVR device approved for both aortic regurgitation and stenosis patients.

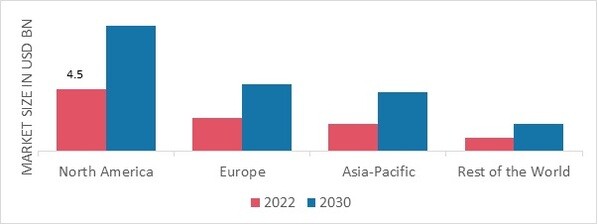

Structural Heart Devices Regional Insights

By Region, the study provides market insights into North America, Europe, Asia-Pacific, and the Rest of the World. The North America Structural Heart device market accounted for USD 4.5 billion in 2022 and is expected to exhibit a significant CAGR growth during the study period. This is attributed to the rate of endovascular procedures has increased as well as invasive procedures across the Region.

Further, the significant countries studied in the market report are The U.S., Canada, Germany, France, the UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil.

Figure 3 STRUCTURAL HEART DEVICES MARKET SHARE BY REGION 2022 (%)

Source Secondary Research, Primary Research, MRFR Database, and Analyst Review

Europe's Structural Heart Devices market accounts for the second-largest market share due to indications into valvular heart disease, cardiomyopathy, congenital heart abnormalities, and others. The two subtypes of valvular heart disease are regurgitation and stenosis. Hence, rising applications of the Segment for biological and tissue valves held a significant market share for structural cardiac devices worldwide. Further, the Germany market of Structural Heart Devices had the largest market share, and the UK market of Structural Heart Devices was the fastest-growing market in the European Region.

The Asia-Pacific Structural Heart Devices Market is expected to grow at the fastest CAGR from 2022 to 2030. This is due to increased rates of cardiovascular disease in the rapidly evolving healthcare industry. Moreover, Japan's market of Structural Heart Devices held the largest market share, and the India market of Structural Heart Devices was the fastest-growing market in the Asia-Pacific region.

Structural Heart Devices Key Market Players& Competitive Insights

Major market players are spending a lot on R&D to increase their product lines, which will help the market of Structural Heart Devices grow even more. Market participants are also taking various strategic initiatives to develop their worldwide footprint, with key market developments such as new product launches, contractual agreements, mergers and acquisitions, increased investments, and collaboration with other organizations. Competitors in the Structural Heart Devices industry must offer cost-effective items to expand and survive in an increasingly competitive and rising market environment.

One of the primary business strategies manufacturers adopt in the Structural Heart Devices industry to benefit clients and expand the market sector is manufacturing locally to reduce operating costs. The structural Heart devices industry has provided medicine with some of the most significant benefits in recent years. The Structural Heart Devices market major player such as Edwards Lifesciences Corporation (US), Medtronic plc (Ireland), Abbott (US), Boston Scientific Corporation (US), LivaNova plc (UK), ST. Jude Medical, Biomerics, ComedBV,JenaValve Technology Inc.,CardioKinetix,Cook Group Incorporated (US), and others are working on expanding the market demand by investing in research and development activities.

Philips, is a Dutch multinational conglomerate corporation that was founded in Eindhoven in 1891. Since 1997, it has been mostly headquartered in Amsterdam, though the Benelux headquarters is still in Eindhoven. Philips launched EchoNavigator 4.0, the new release of its image-guided therapy solution for treating structural heart disease. EchoNavigator 4.0 gives users of Philips’ EPIQ CVXi interventional cardiology ultrasound system a control of live fusion-imaging on the company’s Image Guided Therapy System called “Azurion – platform.”

Genesis MedTech Group is a medical device company headquartered in Singapore. Founded by professionals and entrepreneurs with MedTech experience ly and in Asia, its product portfolio focuses on value segment multi-therapy medical device products for emerging markets with sales and distribution through its established commercial network. Genesis MedTech Group covers the entire industry value chain of research and development, manufacturing, quality management, supply chain, marketing, and sales. Genesis MedTech Group (Genesis or Group) completed the acquisition of JC Medical (JCM). This structural heart company primarily designs and develops transcatheter valve replacement products for the minimally invasive treatment of structural heart diseases. J-Valve, developed by JCM, is the first and only in China to successfully develop and commercialize a minimally invasive TAVR device approved for both aortic regurgitation and stenosis patients.

Key Companies in the market of Structural Heart Devices include

- Edwards Lifesciences Corporation (US)

- Medtronic plc (Ireland)

- Abbott (US)

- Boston Scientific Corporation (US)

- LivaNova plc (UK)

- Jude Medical

- Biometrics

- Come BV

- JenaValve Technology Inc.

- CardioKinetix

- Cook Group Incorporated (US)

Structural Heart Devices Industry Developments

In May 2022 Philips launched EchoNavigator 4.0, the new release of its image-guided therapy solution for treating structural heart disease. EchoNavigator 4.0 gives users of Philips’ EPIQ CVXi interventional cardiology ultrasound system a control of live fusion-imaging on the company’s Image Guided Therapy System called “Azurion – platform.”

In February 2022 GenesisMedTech Group (Genesis or Group) completed the acquisition of JC Medical (JCM). This structural heart company primarily designs and develops transcatheter valve replacement products for the minimally invasive treatment of structural heart diseases. J-Valve, developed by JCM, is the first and only in China to successfully develop and commercialize a minimally invasive TAVR device approved for both aortic regurgitation and stenosis patients.

Structural Heart Devices Market Segmentation

Structural Heart Devices Type Outlook

- Heart Valve Devices

- Annuloplasty Rings

- Occluders

- Delivery Systems

Structural Heart Devices Indication Outlook

- Valvular Heart Disease

- Cardiomyopathy

Structural Heart Devices Procedure Outlook

- Replacement Procedures

- Repair Procedures

Structural Heart Devices Regional Outlook

-

North America- US

- Canada

- Europe

-

Germany- France

- UK

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific- China

- Japan

- India

- Australia

- South Korea

- Australia

- Rest of Asia-Pacific

-

Rest of the World- Middle East

- Africa

- Latin America

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.