Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

The integration of superior diagnostic technologies is an excellent trend in the Veterinary Laboratory Testing market. Innovations such as molecular diagnostics, PCR checking out, and superior imaging strategies are improving the accuracy and speed of disorder analysis in animals, permitting veterinarians to provide more focused and effective remedies. There is a shift closer to complete health testing for animals, together with ordinary bloodwork, urinalysis, and other diagnostic panels. Veterinarians are more and more recommending those checks as part of preventive care to assess the general health of animals and discover capability fitness problems before they become severe.

The demand for factor-of-care checking out is on the upward thrust, driven by the want for quick and on-website diagnostic effects. Point-of-care checking out allows veterinarians to make fast selections about treatment plans, allowing well-timed interventions and improving the performance of veterinary care, especially in emergencies. The adoption of digitalization and telemedicine in veterinary care is influencing the Veterinary Laboratory Testing market. Digital structures allow seamless communication among veterinarians and puppy owners, facilitating the sharing of test effects, far-off consultations, and the mixing of laboratory statistics into electronic health information for animals.

The increasing focus on zoonotic sicknesses and their capacity effect on human fitness is driving the need for surveillance via Veterinary Laboratory Testing. Monitoring diseases that can be transmitted among animals and people is vital for public fitness, and veterinary laboratories play an essential position in early detection and prevention. Regulatory compliance and adherence to standardized testing protocols are becoming more prominent in the Veterinary Laboratory Testing market. Veterinary laboratories that specialize in assembly regulatory requirements to ensure the accuracy and reliability of looking results, fostering consideration amongst veterinarians, puppy owners, and regulatory authorities.

The One Health approach, emphasizing the interconnectedness of human, animal, and environmental fitness, is influencing the Veterinary Laboratory Testing marketplace. Collaborative efforts between veterinary and human healthcare professionals, in addition to environmental scientists, are shaping the development of comprehensive strategies to deal with health challenges at the intersection of these domain names. Education and cognizance initiatives are playing a crucial function in riding the Veterinary Laboratory Testing marketplace. Outreach programs aimed toward veterinarians, farmers, and pet proprietors are promoting the significance of regular testing, disease prevention, and the role of veterinary laboratories in safeguarding animal fitness.

Veterinary Laboratory Testing Market Highlights:

Veterinary Laboratory Testing Market Overview

The veterinary laboratory testing market is expected to rach USD 15.8 billion by 2030 at CAGR of 10.4% during the forecast period 2022-2030.

Veterinary healthcare refers to a subset of science that deals with diagnosing, treating, and preventing various diseases in animals to expand their lifespan. It involves several services, including regular monitoring of animal health and deployment of medicated animal feeds, diagnostic products, drugs, and vaccines for limiting the spread of zoonotic diseases among animals and people. These amenities are extensively provided by the sole traders, pharmacies, veterinary hospitals, clinics, and laboratory testing services. Veterinary healthcare facilities are available for both companions and livestock animals.

The global veterinary healthcare market is driven by the increasing prevalence of various zoonotic, food-borne, and chronic diseases, such as cancer, especially among cats and dogs. This is further supported by the emerging trend of pet humanization and the increasing concerns of pet owners toward animal health, which, in turn, is facilitating the demand for preventive and more sophisticated veterinary services and therapeutic and diagnostics treatments. In line with this, significant technological advancements, such as introducing veterinary health information systems for efficient data management, are another growth-inducing factor. These devices assist in diagnosing animal health, facilitating real-time analysis of disease fluctuations, recording information on cloud-based platforms, and sharing essential veterinary clinic-generated data with clinicians and researchers directly through the internet.

Segmentation

The veterinary laboratory testing market has been segmented into animal type, technology, product, and end user.

The market, on the basis of animal type, has been segmented into companion animal and livestock animal. The companion animal segment is further classified as dogs, cats, horses and others. The livestock animal segment is further classified as cattle, pigs, poultry and others.

The market, by technology, has been segmented into clinical biochemistry, immunodiagnostics, hematology, molecular diagnostics, urinalysis, and others.

The clinical biochemistry segment is further classified as clinical chemistry analysis, glucose monitoring, and blood gas & electrolyte analysis. The clinical chemistry analysis segment includes clinical chemistry reagent clips and cartridges and clinical chemistry analyzers. The glucose monitoring segment includes blood glucose strips, glucose monitors and urine glucose strips. The blood gas & electrolyte analysis segment includes blood gas and electrolyte reagent clips and cartridges and blood gas & electrolyte analyzers.

The immunodiagnostics segment is further classified as ELISA tests, lateral flow assays, allergen-specific immunodiagnostic tests, immunoassay analyzers, and others. The lateral flow assays segment includes lateral flow rapid tests, and lateral flow strip readers.

The hematology segment is further classified as hematology cartridges, and hematology analyzers.

The molecular diagnostics segment is further classified as polymerase chain reaction (PCR) tests, microarrays, and others.

The urinalysis segment is further classified as urinalysis clips & cartridges/panels, urine analyzers, and urine test strips.

The market, by product, has been segmented into consumables and instruments.

The market, by end user, has been segmented into veterinary hospitals & clinics, in-house testing, research institutes, diagnostic laboratories, and others. The veterinary hospitals & clinics segment held the largest segment of the market in 2017. This can be attributed to the increasing incidence of zoonotic diseases. On the other hand, the academic institutes segment is estimated to be the fastest growing segment.

The market has been segmented, by region, into the Americas, Europe, Asia-Pacific, and the Middle East & Africa. The market of veterinary laboratory testing in the Americas has further been segmented into North America and South America, with the North American market divided into the US and Canada.

The European veterinary laboratory testing market has been segmented into Western Europe and Eastern Europe. Western Europe has been classified as Germany, France, the UK, Italy, Spain, and the rest of Western Europe.

The market of veterinary laboratory testing in Asia-Pacific has been segmented into Japan, China, India, South Korea, Australia, and the rest of Asia-Pacific. The market of veterinary laboratory testing in the Middle East & Africa has been segmented into the Middle East and Africa.

Regional Market Summary

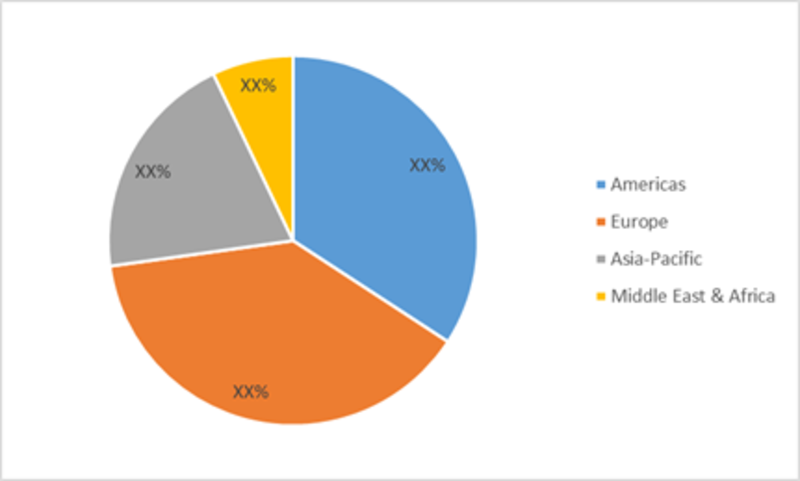

Veterinary Laboratory Testing Market Share (%), by Region

Source: Centers for Disease Control and Prevention (CDC), Eurostat, White Papers, Company Presentations, Annual Reports

Geographically, the Americas is anticipated to dominate the veterinary laboratory testing market owing to increasing cases of animal disease and technological advancements in veterinary diagnostics.

For instance, in 2016, IDEXX Laboratories, Inc. launched the Rapid Visual Pregnancy Test for cattle. With the new test, veterinarians can more quickly identify open cows using whole blood samples collected before the farm visit.

Europe is expected to hold the second largest position in the market of veterinary laboratory testing . The market growth in this region is attributed to the rising expenditure on pet insurance.

The Veterinary Laboratory Testing Market in Asia-Pacific region consists of countries namely China, Japan, Republic of Korea, India, Australia and Rest of Asia-Pacific. The Asia-Pacific region is expected to be fastest growing region owing to the awareness regarding use of sterile consumables for lab testing and rising healthcare spending.

The Middle East & Africa contributes least in the global market for veterinary laboratory testing.

Veterinary Laboratory Testing Animal Type Outlook

- Companion Animals

- Dogs

- Cats

- Horses

- Others

- Livestock Animals

- Cattle

- Pigs

- Poultry

- Others

Veterinary Laboratory Testing Technology Outlook

- Clinical Biochemistry

- Clinical Chemistry Analysis

- Clinical Chemistry Reagent Clips and Cartridges

- Clinical Chemistry Analyzers

- Glucose Monitoring

- Blood Glucose Strips

- Glucose Monitors

- Urine Glucose Strips

- Blood Gas & Electrolyte Analysis

- Blood Gas and Electrolyte Reagent Clips and Cartridges

- Blood Gas & Electrolyte Analyzers

- Clinical Chemistry Analysis

- Immunodiagnostics

- ELISA Tests

- Lateral Flow Assays

- Lateral Flow Rapid Tests

- Lateral Flow Strip Readers

- Allergen-Specific Immunodiagnostic Tests

- Immunoassay Analyzers

- Others

- Hematology

- Hematology Cartridges

- Hematology Analyzers

- Molecular Diagnostics

- Polymerase Chain Reaction (PCR) Tests

- Microarrays

- Others

- Urinalysis

- Urinalysis Clips & Cartridges/Panels

- Urine Analyzers

- Urine Test Strips

- Others

Veterinary Laboratory Testing Product Outlook

- Consumables

- Instruments

Veterinary Laboratory Testing End User Outlook

- Veterinary Hospitals & Clinics

- In-House Testing

- Research Institutes

- Diagnostic Laboratories

- Others

Veterinary Laboratory Testing Region Outlook

- Americas

- North America

- US

- Canada

- South America

- North America

- Europe

- Western Europe

- Germany

- France

- Italy

- Spain

- UK

- Rest of Western Europe

- Eastern Europe

- Western Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- The Middle East & Africa

- Middle East

- Africa

Veterinary Laboratory Testing Market, by Key Players

- Abaxis, Inc.

- BIOCHECK Inc.

- Biomérieux SA

- Henry Schein, Inc.

- Heska Corporation

- Idexx Laboratories

- Idvet

- Neogen Corporation

- Pfizer

- Qiagen N.V.

- Randox Laboratories, Ltd.

- Thermo Fisher Scientific

- VCA Inc.

- Virbac

- Zoetis, Inc.

Recent Development

May 2020

In May 2020, the United States Department of Agriculture’s (USDA) National Veterinary Services Laboratories confirmed SARS-CoV-2 in one tiger at a zoo in New York. As per the World Organization for Animal Health, as of 2020, there are approximately 117 animal diseases, infections, and infestations. In addition, with the rising pet ownership and increasing awareness, the veterinary diagnostics market is expected to grow over the forecast period.Intended Audience

- Research and Development Organization

- Diagnostic Laboratories

- Healthcare Organizations

- Research Institutes

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.