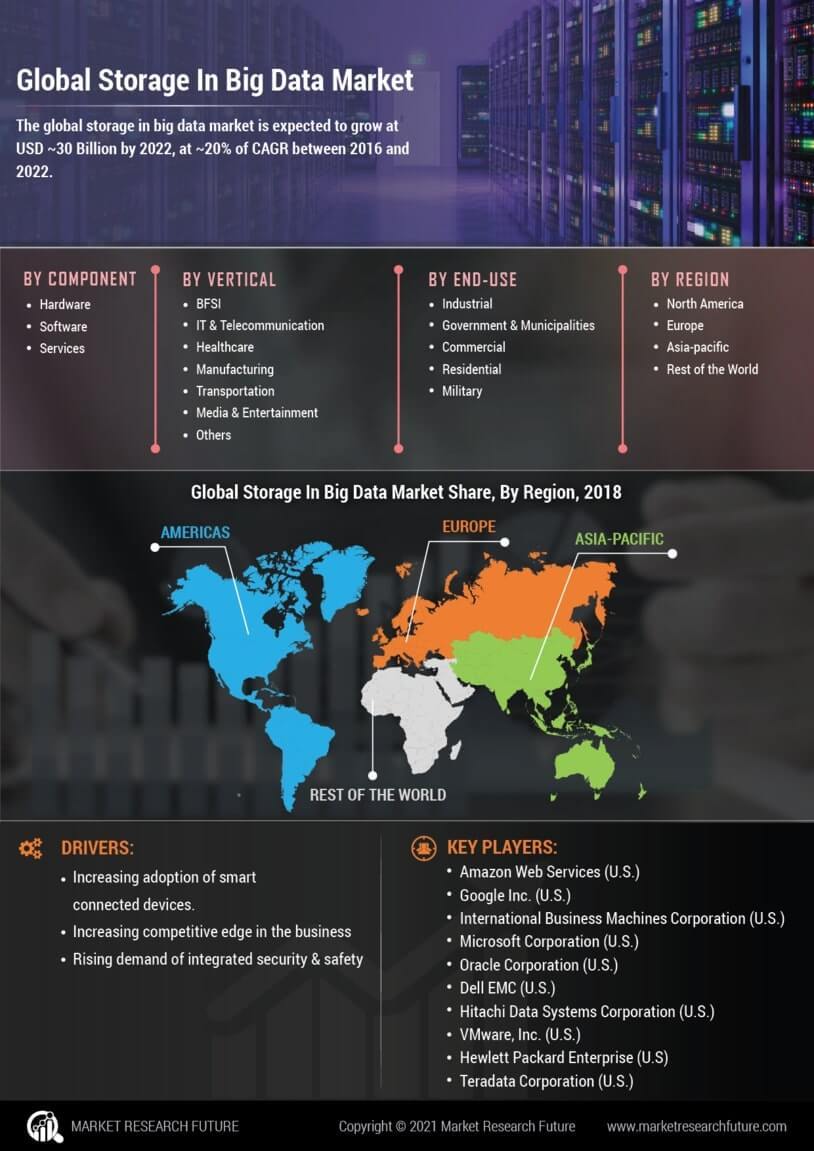

Storage in Big Data Market Overview

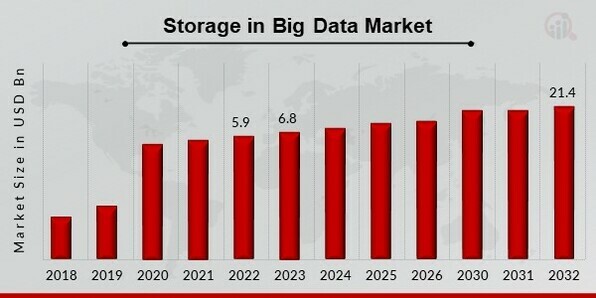

Storage in Big Data Market Size was valued at USD 5.9 billion in 2022. The storage in the big data market industry is predicted to grow from USD 6.8 Billion in 2023 to USD 21.4 billion by 2032, presenting a compound annual growth rate (CAGR) of 16.26% during the forecast period (2023 - 2032). The increasing demand of businesses worldwide for the digitalization of data records is the key market driver enhancing market growth. The global market for storage in big data is anticipated to rise over the forecast period due to rising software-based storage adoption and an increase in connected devices.

Figure 1: Storage in Big Data Market Size, 2023-2032 (USD Billion)

Source: Primary Research, Secondary Research, MRFR Database and Analyst Review

Industry News of Storage in Big Data Market

On Mar.02, 2023, Huawei launched a series of innovative storage products and solutions at the Mobile World Congress (MWC) 2023 for building data infrastructure in the multi-cloud era. Huawei's storage solution will help global carriers develop a trustworthy storage block building in the multi-cloud era. As carriers move from traditional IT/CT services, they face major storage challenges in new services such as video, big data, and cloud.

On Feb.27, 2023, Huawei announced partnerships with five Turkish energy firms for storage systems. The cooperation announced at the Mobile World Congress (MWC) 2023 was formalized through a protocol between Huawei Türkiye and Masfen Energy, Liva Energy, Mensis Energy, Zes Solar, and Yenelis. These Turkish companies will obtain 2 gigawatt-hours (GWh) of energy storage systems from Huawei.

Huawei is committed to providing futuristic technologies, including big data, cloud computing, the IoT, and AI, to help create a digital energy foundation that supports comprehensive digital transformation in the energy sector. Huawei Türkiye's Digital Power Business Group highlighted the importance of transitioning toward clean, low-carbon, and safe & efficient energy systems to meet the world's increasing energy demands.

Storage in Big Data Market Trends

-

Growing amount of data is driving the market growth

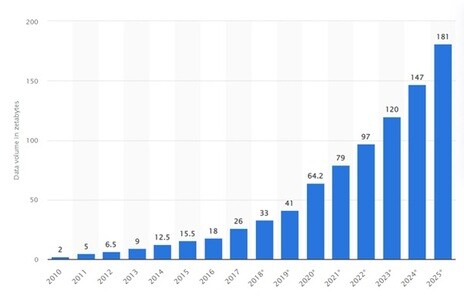

Market CAGR for storage in big data is being driven by the increasing amount of big data for data storage. A significant amount of data has been produced due to increasing digitalization and the Internet of Things (IoT). Due to the exponential expansion in data produced by large-scale industries, including medical records, banking, financial services, e-commerce, videos, and other media, businesses had to adjust their storage capacities to preserve memory storage. As a result, there is a greater requirement for investment in storing and administrating such data. For instance, global spending on big data and analytics solutions will rise by 10.1% by 2020. According to the prediction, a CAGR of 12.8% was predicted for Big Data by 2025. Network-attached storage, directly attached storage, software-defined storage, cloud storage, and server area networks are just a few storage systems and services used to store and manage data. As a result, the growth of Big Data is promoting market expansion.

Figure 2: Total volume of data produced in zettabytes from 2010 to 2020 and forecast from 2021 to 2025

Source: Primary Research, Secondary Research, MRFR Database and Analyst Review

Cloud computing is no longer a novel tool; many businesses have already signed up for cloud services. According to the Global Cloud Computing Scorecard published by BSA, The Software Alliance, cloud computing has been adopted in 24 nations and accounts for 80% of the global IT market. The primary factor driving the expansion of storage in the big data industry is the demand for external and internal hard drives, which are now required for these cloud services' systems. The rising popularity of highly virtualized infrastructure-based hybrid cloud storage systems, where digital data is kept in logical pools. The recording of information on a storage medium is known as data storage. The market for storage in big data is expanding due to businesses adopting centralized and mini mobile data centers more frequently, as well as the rising popularity of cloud computing. Thus, driving the storage in big data market revenue.

Storage in Big Data Market Segment Insights

Storage in Big Data Component Insights

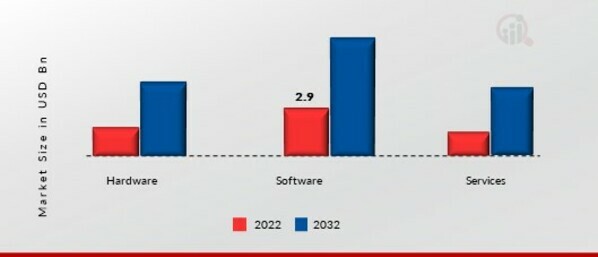

The Storage in Big Data Market segmentation, based on components, includes hardware, software and services. In 2022, the software sector dominated the market. With a software-based storage solution, the storage controller software is decoupled from the hardware and uses industry-recognized hardware platforms to provide a full spectrum of storage services. This enables multiple data storage, data access interface, and service options that can be provided in various ways, including the cloud. However, in 2022, the hardware sector witnessed the fastest growth rate. Tapes, cartridges, hard drives, optical discs, and flash memory are examples of the hardware that is used for data storage. Due to rising global internet usage and computer system demand, the hardware sector has expanded steadily over the past few years.

Figure 3: Storage in Big Data Market, by Component, 2022 & 2032 (USD billion)

Source: Secondary Research, Primary Research, MRFR Database and Analyst Review

Storage in Big Data Vertical Insights

The Storage in Big Data Market segmentation, based on vertical, includes BFSI, IT & telecommunication, healthcare, manufacturing, transportation, media & entertainment and others. The market for storage in big data market was dominated by the healthcare sector in 2022, and it is predicted that it will continue to hold the top spot during the forecast period. In the past several years, the way that data is stored in the healthcare sector has undergone a paradigm shift, moving from traditional digital data storage to the use of cloud storage for the vital patient and organizational data related to a range of procedures, operations, and services.

November 2022: Google Cloud has introduced three powerful Healthcare Data Engines with Lifepoint Health, Hackensack Meridian Health, and others (HDEs). The advanced HDE assists healthcare organizations in improving health equity, value-based treatment, and patient flow.

Big data technologies and services are expected to become more widely used in the BFSI (banking, financial services, and insurance) sector during the forecast period due to their accessibility and affordability. Several financial firms are embracing big data technology and services more broadly for risk management, operations and supply chain efficiency, and preventative and predictive maintenance.

Storage in Big Data Regional Insights

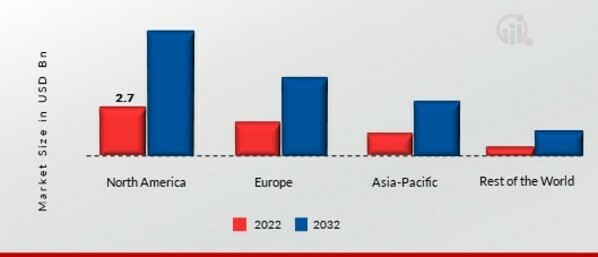

By Region, the study provides market insights into North America, Europe, Asia-Pacific and Rest of the World. The North American storage in the big data area will dominate this market due to the country's regional concentration of international suppliers and consumers. Google also declared intentions to invest USD 9.5 billion in data centers and offices nationwide in April 2022. 14 data centers will be constructed or expanded by the internet giant in US states, including Georgia, Texas, New York, and California, among others.

Further, the major countries studied in the market report are U.S., Canada, German, France, UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil.

Figure 4: STORAGE IN BIG DATA MARKET SHARE BY REGION 2022 (%)

Source: Secondary Research, Primary Research, MRFR Database and Analyst Review

Europe’s storage in the big data market accounts for the second-largest market share. The European Union is making investments, moving quickly, and digitizing local firms. According to a study by The Digital Economy and Society Index, the EU plans to increase the number of ICT workers from 8.9 million in 2021 to at least 20 million by 2030. (DESI). There will be a need for high-storage platforms due to the expanding need for digitalization in the IT sector. Further, German storage in the big data market held the largest market share, and UK storage in the big data market was the fastest-growing market in the European region.

The Asia-Pacific Storage in Big Data Market is estimated to expand at a rapid rate from 2023 to 2032. Data centers changed due to the pandemic as they developed solutions supported by Big Data, IoT, 5G, and cloud computing. For instance, Pure Storage opened a research and development facility in Bengaluru, India. Pure Storage is a data management and software service company based in California. As a result, this is giving the local market several opportunities. Moreover, China’s storage in the big data market held the largest market share, and Indian storage in the big data market was the fastest-growing market in the Asia-Pacific region.

Storage in Big Data Key Market Players & Competitive Insights

Leading market players are investing heavily in research and development to expand their product lines, which will help the storage in the big data market grow even more. Market participants are also undertaking different strategic activities to expand their global footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, storage in the big data industry must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics manufacturers use in the global storage in the big data industry to benefit clients and increase the market sector. In recent years, storage in the big data industry has offered some of the most significant advantages to medicine. Major players in the storage in the big data market, including Hitachi Data Systems Corporation (U.S.), Microsoft Corporation (U.S.), Teradata Corporation (U.S.), Google Inc. (U.S.)., and others, are attempting to increase market demand by investing in research and development operations.

Hewlett Packard (HP) is a global American information technology corporation headquartered in Palo Alto, California. HP created and sold various hardware components, related services, and software to consumers, medium-sized and small businesses (SMBs), big organizations, and customers in the health, government, and education sectors. In May 2021, HP Enterprise unveiled advancements that will alter HP storage in the software-defined data and cloud-native services market. The new solutions can take advantage of the edge-to-cloud data explosion, the silos and complexity that epidemic data creates, boost agility and creativity, and reduce corporate risk.

StarWind is a storage virtualization service provider that aims to supply all the building pieces needed to develop a full-stack data center infrastructure. Storage management and storage area network software provision, a hyper-converged platform that unifies commodity servers, discs, and flash, with multiple options for hypervisors and software-defined storage, cloud gateways, and more are among the services provided by the company, allowing businesses to build a flexible, easily scalable, and cost-effective information technology infrastructure. In July 2021, StarWind introduced SAN and NAS, a pre-configured Linux-based solution that allowed users to convert existing hypervisor servers into high-performance storage applications. Users may reinvent their hardware as software-defined storage without paying extra or purchasing a real NAS/SAN.

Key Companies in the storage in big data market include

- Google Inc. (U.S.)

- Oracle Corporation (U.S.)

- Amazon Web Services (U.S.)

- Google Inc. (U.S.)

- VMware, Inc. (U.S.)

- International Business Machines Corporation (U.S.)

- Teradata Corporation (U.S.)

- Dell EMC (U.S.)

- Hewlett Packard Enterprise (U.S)

- Microsoft Corporation (U.S.)

- Hitachi Data Systems Corporation (U.S.)

Storage in Big Data Industry Developments

In collaboration with Nvidia, AI data platform Vast Data unveiled an AI architecture for data centers in March 2024. The vendor asserts that the new system will provide enhanced zero-trust security in addition to improved performance and service quality. The architecture, which is constructed using Nvidia BlueField-3 data processing unit (DPU) technology, "enables the native disaggregation of the entire Vast operating system into AI computing machinery, thereby converting supercomputers into AI data engines." Vast's system facilitates the training of AI models through the storage and synthesis of vast quantities of data. It introduced its data platform a year ago, providing storage, database, and compute engine services to facilitate AI-enabled research. Vast believes that the new architecture design will significantly reduce the cost, footprint, and power consumption of AI data services by integrating storage and database processing services directly into AI servers and providing "true linear data services designed to scale to hundreds of thousands of GPUs." Additionally, the design eliminates multiple layers of x86 hardware and networking from the data platform infrastructure.

Global market leader Huawei introduced in February 2024 three cutting-edge solutions designed to assist carriers in developing industry-leading data infrastructures for the AI era: an AI data lake solution, an all-scenario data protection solution, and a DCS full-stack data center solution. Data assets are becoming more valuable and an era of data awakening is imminent due to the exponential growth of large AI models. In the era of artificial intelligence, data infrastructure development faces two crucial obstacles. Before knowledge can be extracted from data, dispersed and independent data sources must be compiled in AI data factories in order to derive value from the data. This creates stringent criteria for the transfer of data. Second, the rate of expansion of data assetization is brisk. At present, annotated AI data and model data are retained for an average of over three years. Furthermore, certain valuable corpus data necessitates permanent storage. Huawei has introduced a range of cutting-edge storage products and solutions to assist carriers in constructing industry-leading data infrastructures in the era of artificial intelligence.

October 2022: Seagate has introduced the Lyve cloud analytics system, a comprehensive cloud-based solution that includes storage, analytics, and computing. Seagate enables enterprises to begin storing their data in an open data architecture for analytics at a petabyte scale, advancing innovation and implementation.

December 2021: Microsoft has introduced the soft delete for blobs capability in Azure Data Lake Storage. This function safeguarded files and folders against accidental deletion by retaining destroyed data in the system for a certain time period. Within the retention period, users might return a softly erased object, like a file or directory, to its prior state. The object will be permanently deleted after the designated retention time has passed.

Storage in Big Data Market Segmentation

Storage in Big Data Component Outlook

- Hardware

- Software

- Services

Storage in Big Data Vertical Outlook

- BFSI

- IT & Telecommunication

- Healthcare

- Manufacturing

- Transportation

- Media & Entertainment

- Others

Storage in Big Data Regional Outlook

- North America

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Australia

- Rest of Asia-Pacific

- Rest of the World

- Middle East

- Africa

- Latin America

| Report Attribute/Metric |

Details |

| Market Size 2022 |

USD 5.9 billion |

| Market Size 2023 |

USD 6.8 billion |

| Market Size 2032 |

USD 21.4 billion |

| Compound Annual Growth Rate (CAGR) |

16.26% (2023-2032) |

| Base Year |

2022 |

| Market Forecast Period |

2023-2032 |

| Historical Data |

2019- 2021 |

| Market Forecast Units |

Value (USD Billion) |

| Report Coverage |

Market Competitive Landscape, Revenue Forecast, Growth Factors, and Trends |

| Segments Covered |

Component and Vertical |

| Geographies Covered |

Asia Pacific, North America, Europe, and the Rest of the World |

| Countries Covered |

The U.S., Canada, German, UK, France, Spain, Italy, China, Japan, India, Australia, South Korea, and Brazil |

| Key Companies Profiled |

Hitachi Data Systems Corporation (U.S.), Microsoft Corporation (U.S.). Teradata Corporation (U.S.), and Google Inc. (U.S.). |

| Key Market Opportunities |

Rise in investment in IT sectors by various businesses |

| Key Market Dynamics |

Incorporation of digital transformation in top-level strategies |

Storage in Big Data Market Highlights:

Frequently Asked Questions (FAQ) :

The size of the global storage in the big data market was valued at USD 5.9 Billion in 2022.

The global market is predicted to grow at a CAGR of 16.26% during the forecast period, 2023-2032.

North America had the major share of the global market.

The key players in the market are Hitachi Data Systems Corporation (U.S.), Microsoft Corporation (U.S.). Teradata Corporation (U.S.), and Google Inc. (U.S.).

The software category dominated the market in 2022.

The healthcare sector had the largest share of the global market.