Telecom Cloud Market Summary

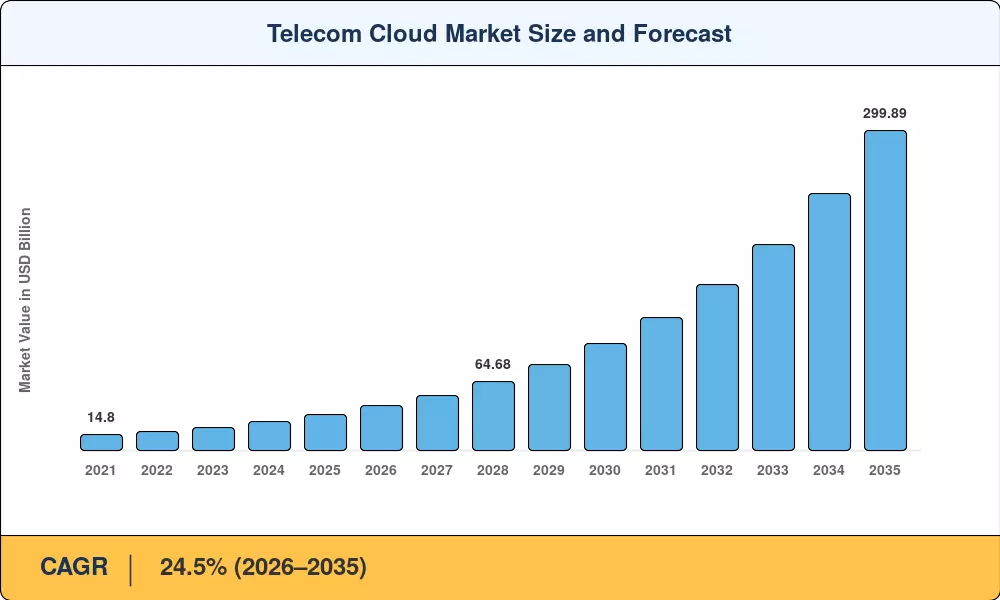

The Telecom Cloud Market was valued at USD 33.52 Billion in 2025 and is projected to grow from USD 41.73 Billion in 2026 to USD 299.89 Billion by 2035, registering a 24.5% CAGR during the forecast period (2026–2035). Operators worldwide are channeling capital toward cloud-native network cores as 5G standalone deployments accelerate and edge computing use cases proliferate. AT&T's USD 14 billion Open RAN agreement with Ericsson signals the capital intensity reshaping the Telecom Cloud Market at an infrastructure level [1].

Legacy monolithic network architectures — built around proprietary hardware stacks — are giving way to software-defined, containerized platforms that run on commercial off-the-shelf servers. Vodafone's USD 1.5 billion multi-cloud partnership with Microsoft illustrates how carriers are re-platforming core and edge workloads to meet performance, sovereignty, and compliance mandates simultaneously [2]. This shift compresses operational expenditure cycles from years to months, letting carriers launch new revenue-generating services at software speed.

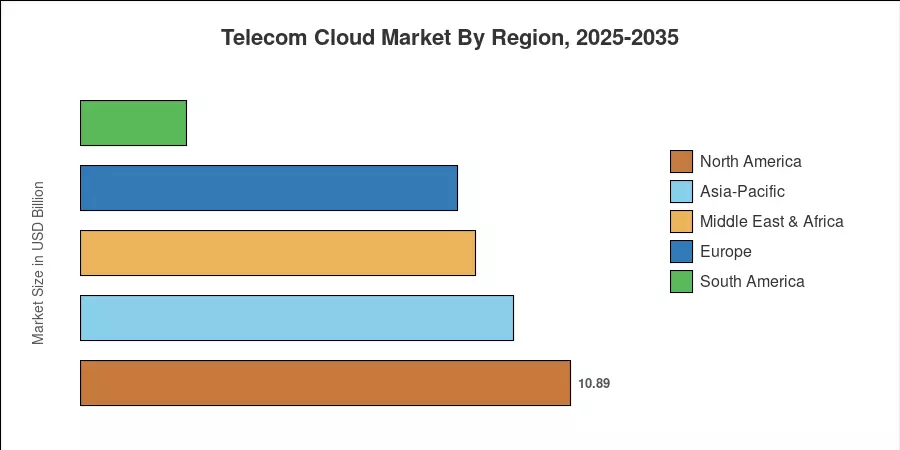

North America commands approximately 32.5% of the Telecom Cloud Market revenue, supported by hyperscaler proximity and early 5G core migrations. Asia-Pacific is the fastest-growing region at a 28.7% CAGR, propelled by India's Jio-scale investments and China's state-backed cloud-native rollouts. Europe holds the second-largest share, near 25.0%, driven by the EU's Digital Decade targets and Open RAN pilots across multiple national carriers [3]. The Telecom Cloud Market is poised to reshape connectivity economics through 2035 as carriers convert network functions into cloud-native microservices.

Key Report Takeaways

• By Solution Type

- Solution offerings captured 48.9% of Telecom Cloud Market revenue in 2025, reflecting demand for turnkey cloud-native network platforms among Tier 1 operators.

- Services are projected to expand at a 29.2% CAGR through 2035 as managed migration, integration, and optimization engagements grow.

• By Platform

- Infrastructure-as-a-Service held 45.4% of the Telecom Cloud Market share in 2025, anchored by compute and storage outsourcing for virtualized network functions.

- Platform-as-a-Service is forecast to climb at a 30.4% CAGR to 2035, fueled by DevOps toolchains for telecom application development.

• By Application

- Billing and Provisioning represented 41.5% of the Telecom Cloud Market in 2025, the first workload most operators migrate to the cloud.

- Traffic Management is on track for a 29.8% CAGR through 2035 as real-time analytics demand intensifies.

• By End User

- BFSI accounted for 34.4% of the Telecom Cloud Market share in 2025, driven by low-latency trading and secure connectivity needs.

- Healthcare exhibits the fastest end-user expansion at a 26.1% CAGR through 2035.

• By Region

- North America represented 32.5% of the Telecom Cloud Market revenue in 2025.

- Asia-Pacific is projected to grow at a 28.7% CAGR between 2026 and 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates are derived from a combination of primary interviews with telecom CIOs and CTOs, carrier capex disclosures, hyperscaler revenue breakdowns, and validated against third-party benchmarks. Historical figures reflect actual reported spending; forecast values apply the calibrated 24.5% CAGR with adjustments for macroeconomic cycles.